{kind=link}

The Government announced today new property cooling measures. The measures saw adjustments to the Additional Buyer’s Stamp Duty (ABSD) rates and Loan-to-Value (LTV) limits on residential property purchases, to cool the property market and keep price increases in line with economic fundamentals.

<TO FIND THE BEST HOME LOANS IN SINGAPORE CLICK HERE>

Status of the Private Housing Market

After declining gradually for close to 4 years, private residential prices began rising in 3Q2017. Prices have increased sharply by 9.1% over the past year. Demand for private residential property has also seen a strong recovery, as transaction volumes continue to rise.

The Government said the new property cooling measures were necessary to check sharp increase in prices, which could run ahead of economic fundamentals and raise the risk of a destabilising correction later, especially with rising interest rates and the strong pipeline of housing supply.

The new property cooling measures introduced by the Government includes raising the ABSD rates and tighten LTV limits for residential property purchases.

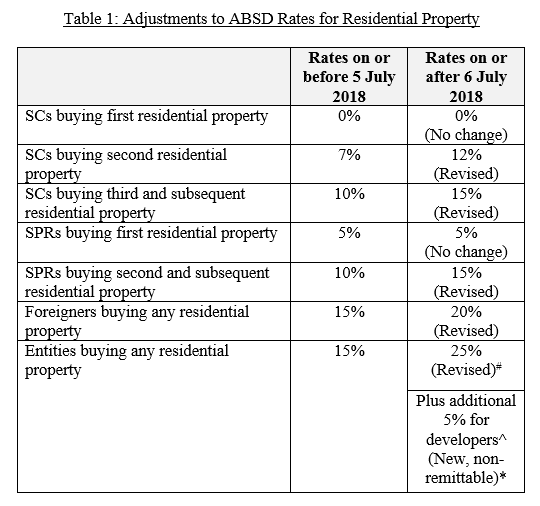

Raising ABSD Rates

The current ABSD rates for Singapore Citizens (SC) and Singapore Permanent Residents (SPR) purchasing their first residential property will be retained at 0% and 5% respectively.

The Government will make the following changes to ABSD rates:

a. Raise ABSD by 5%-points for all other individuals; and

b. Raise ABSD by 10%-points for entities; and

c. Introduce an additional ABSD of 5% that is non-remittable under the Remission Rules (payable on the purchase price or market value, as applicable) for developers purchasing residential properties for housing development.

The Government said that being entities, developers will also be subject to the ABSD rate of 25% for entities. Developers may apply for remission of this 25% ABSD, subject to conditions (including completing and selling all units within the prescribed periods of 3 years or 5 years for non-licensed and licensed developers respectively). Details are provided under the Stamp Duties (Non-licensed Housing Developers) (Remission of ABSD) Rules and the Stamp Duties (Housing Developers) (Remission of ABSD) Rules.

This new 5% ABSD for developers is in addition to the 25% ABSD for all entities. This 5% ABSD will not be remitted, and is to be paid upfront upon purchase of residential property.

For purchases made jointly by two or more parties of different profiles, the highest applicable ABSD rate will apply. However, full ABSD remission will continue to be provided for joint purchases of the first residential property by married couples with at least one SC spouse.

Married couples with at least one Singapore Citizen spouse, who jointly purchase a second residential property, can continue to apply for a refund of ABSD, as long as they sell their first residential property within 6 months after (a) the date of purchase of the second residential property, or (b) the issue date of the Temporary Occupation Permit (TOP) or Certificate of Statutory Completion (CSC) of the second residential property, whichever is earlier (if the property was uncompleted at the time of purchase).

There will be a transitional provision for cases where an Option to Purchase (OTP) has been granted by sellers to potential buyers on or before 5 July 2018, and this OTP has not been varied on or after 6 July 2018. For such cases, the current ABSD rates, instead of the revised ABSD rates, will apply if the OTP is exercised within 3 weeks of this announcement (i.e. exercised on or before 26 July 2018) or the OTP validity period, whichever is earlier.

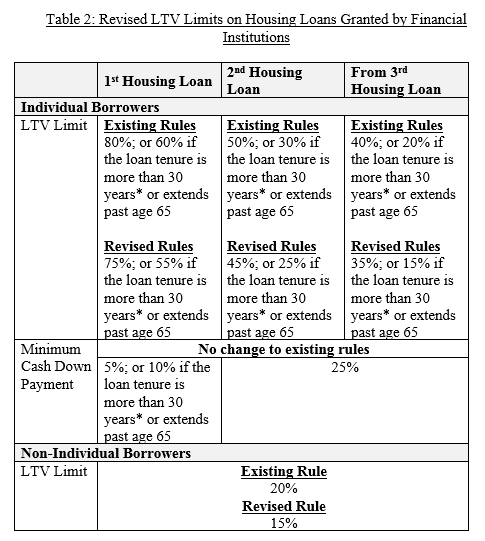

Tightening of LTV Limits

LTV limits will be tightened by 5%-points for all housing loans granted by financial institutions. These revised LTV limits do not apply to loans granted by HDB.

Table 2 summarises the adjustments to the LTV limits:

The LTV Limit will be 25 years, where the property purchased is a HDB flat.

The tightened LTV limits will apply to loans for the purchase of residential properties where the OTP is granted on or after 6 July 2018.

In line with the tightening of LTV limits for housing loans, LTV limits for mortgage equity withdrawal loans (MWLs) will be tightened as follows:

a. 75% for a borrower with no outstanding housing loan for the purchase of another residential property; and

b. 45% for a borrower with an outstanding housing loan for the purchase of another residential property.

The tightened LTV limits will apply to MWL applications made on or after 6 July 2018.

The Government said that it will continue to monitor the property market and adjust its policies as necessary, to maintain a stable and sustainable property market.

Commenting on the new property cooling measures, Minister for National Development Lawrence Wong said that the “government has been monitoring the property market closely.”

He added: “We are very concerned that prices are running ahead of economic fundamentals. There is a large supply of units coming on stream and interest rates are going up. We want to avoid a severe correction later, which can have more destabilising consequences. Hence we are acting now to maintain a stable and sustainable property market”.

The new property cooling measures were introduced after Mr Ravi Menon, the Managing Director of Monetary Authority of Singapore, said developers, banks and home buyers should be cautious about the property market euphoria.

Property market euphoria calls for caution, Singapore central bank chief

Speaking at the MAS annual report media briefing yesterday, he reminded developers who bid for land to be mindful of the huge supply which is coming onstream.

“We need to be mindful of the supply and demand dynamics and we have to ask ourselves whether demand will be able to match the big supply that’s coming onstream in the next few years,” said Mr Menon.

Noting the aggressive bidding by developers (both in en bloc sales and Government Land Sales tenders) against the expectancy of units available in the near term to more than double, the central bank chief warned that this could result in a supply imbalance and weight on the market.

<TO FIND THE BEST HOME LOANS IN SINGAPORE CLICK HERE>

If you are concerned about how the new cooling measures will affect you, our Panel of Property agents and the mortgage consultants at icompareloan.com can advise you. The services of our mortgage loan experts are free. Our analysis will give industrial property loan seekers better ease of mind on interest rate volatility and repayments.

Just email our chief mortgage consultant, Paul Ho, with your name, email and phone number at [email protected] for a free assessment.