It’s always great to come across supporters when Members of Parliament go on their house visits, but a recent visit for Workers’ Party chair Sylvia Lim (Aljunied GCR) was particularly “heartwarming”.

Ms Lim posted a photo on her Instagram account of a man wearing a dark blue mask with the WP logo, a gold hammer in a red circle background, also outlined in gold.

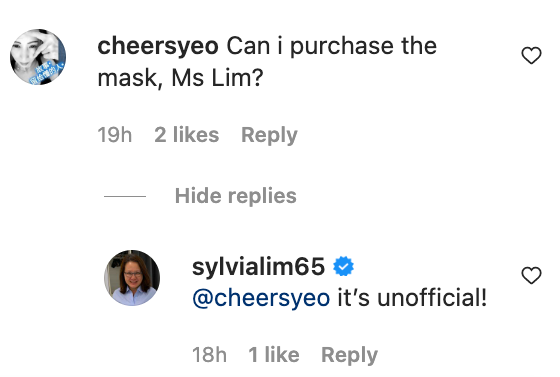

“Heartwarming, but that’s unofficial merchandise!” wrote Ms Lim.

She also took the opportunity to add that the party does make available official items for those who want to carry the WP colour and symbols.

The link the MP provided shows that supporters may buy a bag, a flag, two types of umbrellas, a cap, and the WP60 book, “Walking with Singapore.”

But Ms Lim was not the only one who appeared to be charmed by the mask, unofficial though it may be.

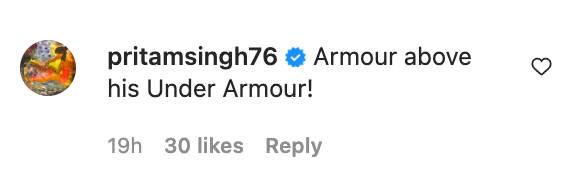

Mr Pritam Singh, Ms Lim’s fellow MP at Aljunied who is the Leader of the Opposition and the party’s Secretary-General, did not only like the photo but dropped a comment about it.

Since the supporter was wearing a shirt from popular sportswear brand Under Armour, Mr Singh wrote, “Armour above his Under Armour!”

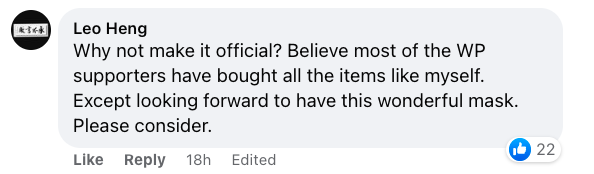

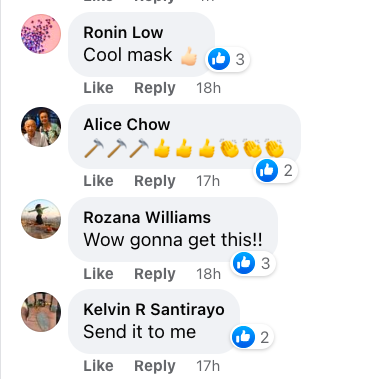

And since the WP is not selling masks at this point, several netizens urged that it does so, with some appearing to like the way it looks.

Several netizens expressed the desire to buy the mask.

Something similar happened after the July 2020 General Election, when WP MP Jamus Lim (Sengkang GRC) made the word “cockles” famous again.

In his first exposure in the national spotlight at the GE2020 Political Debate on July 1, just as the campaign period was beginning, Assoc Prof Lim gave new life to an almost forgotten phrase.

During the debate, Singapore Democratic Party’s Dr Chee Soon Juan highlighted inequalities in the education system.

Assoc Prof Lim, an Associate Professor in Economics, said that, as an educator, what Dr Chee had said: “warms the cockles of my heart”.

And then, as the WP MP thanked residents after they were elected, he said it “warms the cockles of our hearts to be able to work for the people of Singapore, and for all Singaporeans,” holding up a finger heart as he spoke.

Life insurance is a complicated but important kind of insurance coverage. It mainly consists of two types – Whole Life and Term Life. Unlike other insurance plans, life insurance pays out only after the covered policyholder passes away. Hence, it is vital to get the right life insurance coverage and avoid costly errors since rectifying them could prove to be near impossible by the time a problem is discovered after death.

With the Singapore life insurance industry seeing booming sales for 2021, Singaporeans are placing more emphasis and attention on the purchase of life insurance. Are they guilty of making these common life insurance mistakes? And are you one of them?

If you are currently in the market for life insurance or have recently bought a policy, read on to make sure you do not put your family’s finances in jeopardy by making these mistakes.

Mistake #1: Waiting to Buy Insurance

It is not uncommon for people to delay their purchases of insurance policies. After all, the purchase of life insurance is a complicated matter. It is important to consider the amount of coverage you need as well as the cost. It is certainly not easy to make a decision with the plethora of life insurance options out there in the market.

However, buying a life insurance policy sooner, rather than later, can work in your favour if you are seeking to secure a policy at the lowest possible cost.

Life insurance rates generally increase as people age or as their health deteriorates. In some cases, illnesses or health problems may make you ineligible for coverage. The longer you put off the buying decision, the more the insurance will likely cost. Postponing the purchase of a life insurance policy could cost thousands of dollars over a lifetime.

Mistake #2: Buying the Cheapest Policy

While it is important to shop for a life insurance policy that is affordably priced, the coverage that you are getting in return is also crucial. Life insurance policies can be a tad complicated, and it is a good idea to learn about their features and benefits.

Premiums of term life insurance are way less than whole life insurance and for a good reason. Term life insurance only covers you for a set period of time, while whole life insurance covers you until death.

If you believe that you would need life insurance for a set period of time, purchasing a term life policy would be best. On the contrary, if you are seeking lifetime coverage, or you want to own a life insurance policy that builds cash value similar to investments, whole life insurance would be a better choice.

The cheapest policy may not represent the best value. There could be other insurers in the market offering much better coverage at a slightly higher price. Hence, it is essential to evaluate the value of the life insurance plan that you are considering or currently hold.

Mistake #3: Not Paying Premium on Time

You are expected to pay a premium in return for coverage from your life insurance plans. These premiums are based on your insurance risk class, which takes into factor your age, health, and many others.

Missing a premium payment may have serious consequences. Rather than a late fee penalty, a missed premium payment could cause your life insurance policy to lapse, and you will no longer have life insurance coverage. Depending on your insurer, you could get the policy reinstated by paying an additional sum of money.

However, in the event that you are unable to do so, you will have to seek a new life insurance policy. This could come with its own set of problems. Life insurance gets more expensive as you age, and even the difference of several years could lead to a substantial increase in cost. Any changes in health could lead to higher premiums or even ineligibility for life insurance altogether. The search for a new life insurance policy would also cause a coverage gap, and your dependents would not be insured if misfortune strikes during this period.

Life can also throw some unexpected curveballs at you; just as the recent Covid-19 events. Job loss, business failures, or even serious illnesses could impede your ability to pay for your insurance premiums. Hence, it is advisable to balance the coverage you need with a premium you can reasonably afford, even when all things have gone south.

How to avoid it? Pay your premiums on time! Ensure that you have sufficient funds in your bank account should you pay by GIRO, or set a monthly/yearly reminder for you to make payment. You should also consider using various platforms such as PolicyPal to track your various insurances.

Mistake #4: Too Little or Too Much Coverage

It is easy to under/overestimate how much your beneficiaries will need to maintain their current standard of living should anything unfortunate happen to you. Having too little coverage can have serious consequences for the people you leave behind, and they could face financial hardship as a result. Having too much coverage is also a problem due to the higher premiums charged to your card.

To calculate how much life insurance you need, consider what financial obligations need to be covered: replacing your income, paying off a mortgage or other large debts, and paying for your children’s education. Thereafter, consider what assets you have, such as savings, and if they are able to cover these costs. The difference between your assets and obligations is the gap that life insurance needs to fill.

As a rule of thumb, it is advisable for your life insurance coverage to be at least 10 to 15 times your current income. Nonetheless, this is just a rough estimate. Depending on your financial status, this number could be higher or lower.

Mistake #5: Failure to Reassess Your Needs

Most people would have their life insurance policy for quite some time, and there would be a lot of changes during that time. Your life insurance needs will differ greatly when you’re aged 20, 40 and even 60. These shifts in circumstances would signify a need to change your life insurance policies or life insurance beneficiaries.

Determine whether you need more to meet the growing needs of your beneficiaries or less coverage due to the amount of money you have amassed through the years. Carefully consider your budget and needs before purchasing another policy of any kind, to make sure you have the insurance you need at the right price.

If there are any changes to your dependents, do update your life insurance policy accordingly when these changes occur. This ensures those relying on you do not miss out on vital protection, should anything happen to you.

Mistake #6: Borrowing From Your Policy

Life insurance policies that accumulate cash value could be a source of funds when you are in need of money. The cash value of a permanent or whole life insurance policy can generally be used for any reason you see fit, including tax-free withdrawals and loans, if done properly. Policy loans are borrowed against the death benefit, and the insurer uses the policy as collateral for the loan.

This is a great benefit, but it must be carefully managed. If you take too much money out of your policy and your policy lapses or runs out of money, all the gains you have taken out will become taxable. Not to mention, you would significantly reduce the death benefit available to your beneficiaries.

If you have taken too much money out and your policy is about to lapse, you may be able to maintain the policy by making additional premium payments, assuming you can afford them. When accessing your life insurance policy’s cash value, be sure to monitor it closely and consult your financial advisor to avoid any unwanted tax liability.

Conclusion

The purchase of life insurance policies is a complicated affair, but we are here to make it simple for you. Keep in mind these 6 common mistakes before, during, and even after making your purchase.

Consider making your insurance purchase at an earlier age when it is more affordable. Select sufficient coverage at the right price and pay your premiums on time. Reassess your needs every now and then to ensure you have enough coverage. There are no rules that disallow you from having multiple life insurance coverages, so go for it if the need arises. Avoid borrowing from your life insurance policies, and ensure you are able to manage them wisely when you do.

If you are still unsure of how much coverage you need, check out here for a more personalised quote from our experts.

For more tips on your personal finances, check out over here!

It appears that scammers are now targeting motorists in the form of phishing emails disguised as a traffic offence notification. Members of the public have been receiving an email from scammers posing as the Division of Transportation regarding traffic violations.

The notification includes details like, “You’ve been detected with a traffic infringement. Reason: negligent driving”, with the corresponding penalty such as S$95.95. The email continues to say, “All of relevant documentations will be forwarded to you by mail to your address. However you can check it now, please press on button below or click here (sic).”

The emails look like the one below:

Photo: Taken from SPF website

“The police have detected a new phishing scam variant where victims would receive an email from the ‘Division of Transportation’ alleging that they have committed a traffic offence,” said the Singapore Police Force (SPF) in a media release on June 30.

Motorists should note that for traffic offences committed in Singapore, the owner of the vehicle will first be asked to furnish the driver’s particulars before a Notice of Traffic Offence (NTO) is issued to the offending driver. The Traffic Police will not issue a digital NTO, said SPF.

Those who receive unsolicited emails and text messages should not click the attached URL and always verify the information’s authenticity with the official website.

“Never disclose your personal details, Internet banking details or one-time passwords to anyone and report any fraudulent credit or debit card charges to your bank and cancel your card immediately,” added SPF.

Public members with information relating to such crimes can call the Police Hotline at 1800-255-0000 or submit it online at www.police.gov.sg/iwitness. Those in need of urgent police assistance can dial “999”.

More information on scams can be found at www.scamalert.sg or through the Anti-Scam Hotline at 1800-722-6688. /TISG

Fortunately, customers at a Hougang eatery won’t experience the same because stall operators are choosing to keep their prices low amid rising costs.

A caifan stallholder in Block 6 Hougang Avenue 3 continues to sell dishes at S$2, with no plans to raise prices.

According to Chinese language newspaper Shin Min Daily News, the stall operators are willing to shoulder increasing costs because their customers don’t often receive salary increases.

Their price list posted at the front of the stall reads, “We fight Covid-19 together.” It was reported that the stall stayed true to its promise and hasn’t increased prices in the last three years amid the pandemic.

Customers can enjoy one vegetable and one meat or three types of vegetables for S$2.

The 53-year-old stallholder, Mr Guo told Shin Min Daily News that they choose to keep prices the same, so their regular patrons could continue to afford their meals.

Mr Guo admitted that the price for ingredients, utility bills and rent has increased.

However, their regular customers don’t have salaries that are also increasing. Life for them isn’t easy, said Mr Guo.

Another caifan stall at Block 262 Serangoon Central’s Song Le Coffee Shop is doing the same, and it hasn’t changed prices for the last decade.

Customers can purchase three vegetables for S$2, one meat and one vegetable or two types of meat for S$2.50.

Referring to the stallholders’ decision, Facebook user Zig Steenie wrote, they are “the people who understand the men on the ground’s sentiments while those puppets sitting in parliament brainstorming how else can we squeeze from the commoners to sustain our million-dollar salaries.”

“That stall food is nice and cheap. Hope the government don’t consider to enblock that place cause if they have to move, they will not be able to afford the high rental in a multi-million coffeshop. How to maintain that price,” noted Facebook user Peggy Tan. /TISG

While the controversy generated by the recent hanging of convicted Malaysian drug trafficker Nagaenthran K. Dharmalingam (Nagen) seems to be fading, something has surfaced which may put the issue of the mandatory death penalty and its possible pitfalls back in the spotlight.

According to new reports, an innocent Australian holiday-maker was arrested at Changi Airport and charged with trafficking an amount of cocaine punishable by death. 64-year-old Sydney businessman, Philip George Sceats languished in Changi Prison for the next 353 days, under the pall of the capital charge.

Facing the spectre of the hangman’s noose, Sceats’ plight could not be more dire. Fortunately for him, his family had the means, influence, and determination to save his life. They engaged a well-known Singapore criminal lawyer to defend him against the capital charge. They also hired a team of high-credentialed private investigators and consultants to find evidence that would convince the Singapore authorities that he was innocent of the charge and that he had been set up by persons unknown. Sceats’ high-powered team included former high-ranking police officers from three different Australian states.

The team took stock of the many things in Sceats’ case that did not add up. Luckily for Sceats, he was eventually released.

This case illustrates the fallibility of any system. Not because the system is bad, but because humans make mistakes and the system must make allowances for human error, unconscious biases, and such like. No matter how good a system is, to err is human.

Should we have a mandatory death penalty when the consequences of a mistake are irreversible?

Sceats was only able to save his life because he had the means to do so. Many of our convicted drug traffickers are from poor backgrounds without the knowledge or the resources to fight. Does this mean that their lives are less valuable?

While none of us would feel comfortable saying this. The effect of the mandatory death penalty is that some lives will be, in effect, more valuable than others.

I am not criticising the system. It was designed perhaps at a time when this was thought necessary and with the best of intentions to keep Singaporeans safe. However, if it is subsequently revealed that mistakes have unwittingly been made, shouldn’t we consider releasing some of our attachments to what we thought had worked in the past?

Was our system really designed to catch someone with a low IQ like Nagen? Or someone like Sceats who was just a hapless tourist?

Related to this, anti-death penalty activist, Kirsten Han, has said that she has been harassed for her stance against the death penalty. In her Tweet, Ms Han said: “I have been smeared, harassed, investigated, and on Friday the police took the shirt off my back”.

It is of course terrible that Ms Han had to go through any of this. I do wonder though if we can create a space between the anti and pro-death penalty to find some common ground.

I think that we can all agree that we want to create a safe environment for people, and where we disagree is the how. In that regard, the Government is not the enemy. It may just be holding on to a system that is the legacy of another era.

In the same vein, the Government should also see that the activists, such as Ms Han, are not the enemy. They simply want those in power to acknowledge that the system is imperfect as it is and that mistakes have been made.

So perhaps, at this point, the discussion should not be binary and limited to whether or not the death penalty is wrong or right, but rather, what we can do to ensure that our judges have more discretion to exercise their discernment.

Those who have been in the heart of our justice system seem to have acknowledged that the system isn’t perfect.

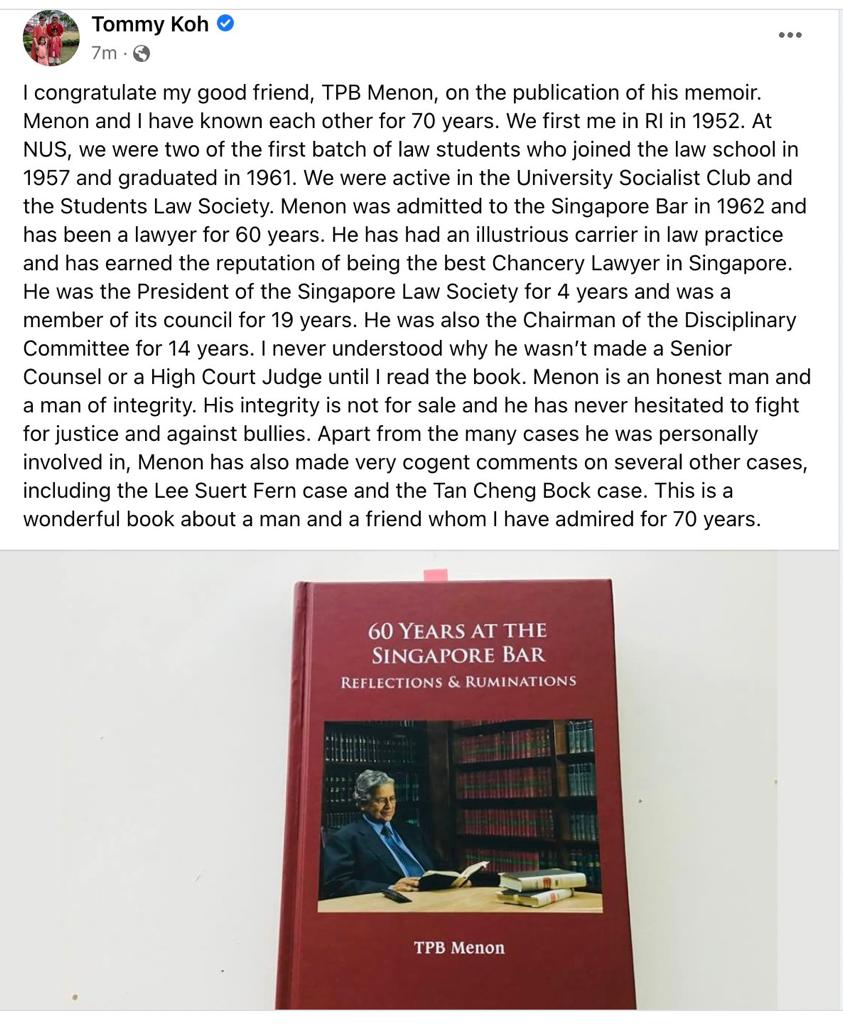

Veteran lawyer TPB Menon has recently published his memoir on his 60 years at the bar. Among other things, he talked about some of the more notable cases, such as that which was made against Lee Suet Fern over the will of late Prime Minister Lee Kuan Yew (LKY). Mr Menon observed that LKY’s legacy was never his marital home but his political acumen and statesmanship, and that fighting over his home was perhaps missing the point. In that vein, it may well be that Mrs Lee was dragged into something that she should never have been dragged into because we confused LKY’s legacy with his home.

While Mr Menon was an illustrious lawyer, it was noteworthy that he was never made a High Court Judge or a Senior Counsel. Professor Tommy Koh posted on his Facebook page that he never understood why Mr Menon was never promoted until he read his book.

Could Professor Koh be implying that politics had something to do with legal promotions?

At the end of the day, no system is perfect, and it is important to acknowledge that Singapore is a safe and stable place to live in. Is it perfect? No. But is it so terrible? No. Is the system perfect? No. Does it make mistakes? Yes. Can it improve? Yes.

But for this to happen, we have to realise that the Government is not the enemy and the Government has to acknowledge that campaigners and activists are not the enemies either.

Let’s look for the space in between.

The book is available in major bookstores and you can get a copy from the publisher – email Ms Janice Ng of APD at [email protected] to buy copies.

A woman felt “so emotional” watching an elderly worker having breakfast alone that she wondered why the pioneer generation in Singapore still had to work to make a living.

“Stumbled upon this elderly sitting down eating his breakfast before he starts work,” wrote TikTok user @clumsydaisyxxxz in the video.

She admitted feeling emotional watching the man spread peanut butter on his bread and sip his milo.

“I guess being in Singapore, regardless of how pioneer you have become, you still have to work your ass off for a living,” she noted, adding that retirement only applies to the rich or those with kids who could look after the elderly.

“If not, you need to work to live,” said the TikTok user. “I wish you well, uncle. Hope you like the little gifts from me,” she added.

Although the kind stranger’s efforts sparked criticisms from netizens who said she didn’t need to “broadcast” the good deed, many still thanked her as it raised awareness of the current situation.

“I see it with so much positivity, and by sharing, it will inspire more awareness and love amongst us,” said Facebook user Clara Chua.

“Food is definitely costly in the town area, so Uncle might be trying to save money,” highlighted Facebook user Ari Tumijo. “Kudos to the lady for this kind gesture, doesn’t matter if she uploaded it to socmed for likes or whatever, it’s the gesture that mainly counts.”

The topic of Singapore’s elderly still working instead of retiring often circulates on social media. Some, like the case of 95-year-old Mdm Zheng Xuehua, choose to continue working because they’re not used to the leisurely life of retirement.

Another senior citizen, a 79-year-old woman, collects cardboard to pass the time and get some exercise while earning a small income on the side.” /TISG

A woman who ordered takeout food from a mamak stall in Little India was surprised to pay S$15 for some curry chicken, rice, and vegetables.

Although she expected the dish to be more expensive than before due to increasing prices, she didn’t think it would be so overpriced.

The customer posted her experience on Facebook, attaching a photo of her meal, which she purchased from a 24-hour eatery in Little India. The dish consisted of some curry chicken and a small portion of vegetables on some rice.

Photo: FB screengrab/人在狮城漂

Despite the food being delicious, the customer thought paying S$15 for the meal was outrageous. She added that this would be the first and last time she would buy from the stall.

With over 280 comments to date, netizens agreed that the price was too much.

“S$15 for a meal? How much do you earn a day?” asked a Facebook user, referring to the high cost of living.

Others advised avoiding stalls with no set pricing to minimize the risks of paying a hefty bill at the cashier.

Some also included photos of their ordered meals and the corresponding price for reference.

Photo: FB screengrab/人在狮城漂

The following meal was only S$13, according to Facebook user Joyce SQ.

Photo: FB screengrab/人在狮城漂

This isn’t the first time a diner’s total bill came as a shock. A person who paid S$11 for cai png or economy rice with fish at a hawker centre also felt he was robbed.

Read the story below for some tips on how to avoid or prevent an unexpected bill amount for food. /TISG

A video of two construction workers fighting went viral last week. The 16-second-long clip garnered over 12,000 views within four days. The fight allegedly took place at a work site of the Bukit Batok-Tengah link project.

According to Zul, the netizen who took the video, the man to be blamed was the safety officer on site. In the comments section, other netizens said that the safety officer was the one wearing a blue hardhat and could be seen in the clip using his mobile phone to record the fight.

In the clip, two men could be seen scuffling while holding a pole between them. One was wearing safety gear, a hardhat and a vest. It is unclear from the clip who had used the pole to attack the other, but as the fight progressed, the man in the hardhat seemed to get the upper hand, slapping and punching his opponent.

In the comments section, many asked why those around did not come in to help, but Zul wrote that they were all more interested in filming the incident than stopping it.

Recently, videos of a fight between two men in a coffee shop have also gone viral online; one used nearby plastic chairs to defend himself, while another attacked with a knife.

“Bukit Merah!” wrote Facebook user Patrick Tan on Wednesday (June 29), referring to the location of a fight between two men.

Mr Tan’s post included a video of a man in a black shirt charging toward another man with an object presumed to be a knife in his hand.

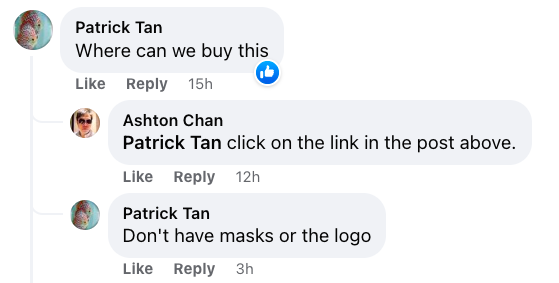

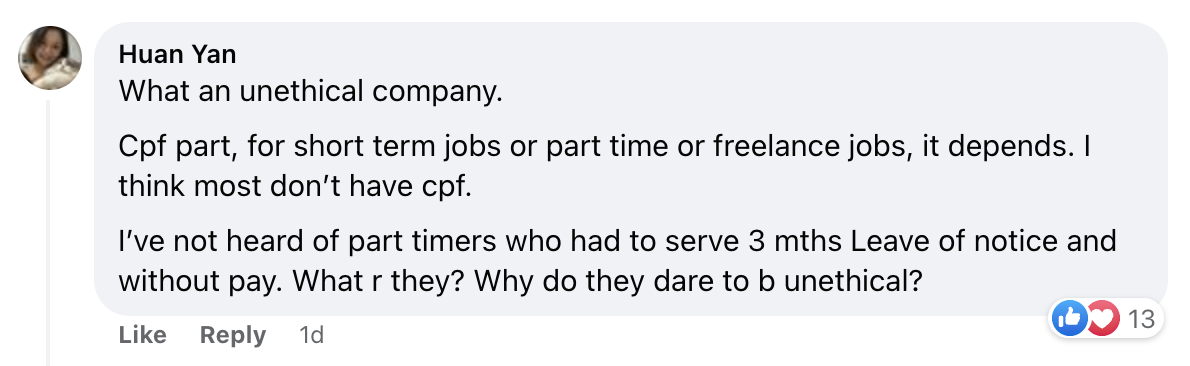

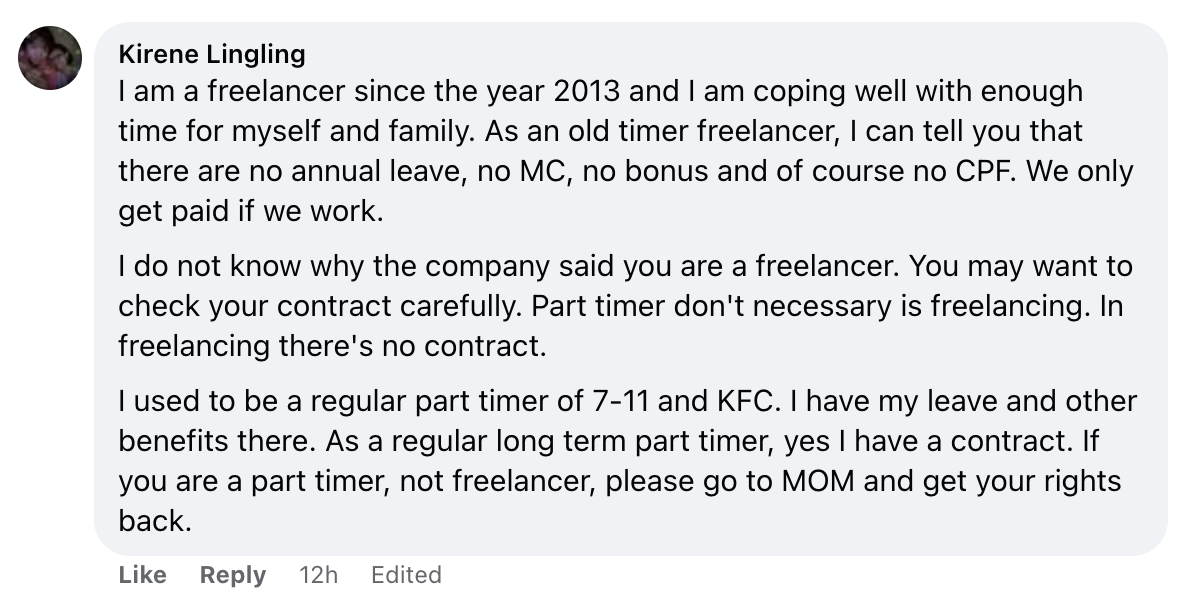

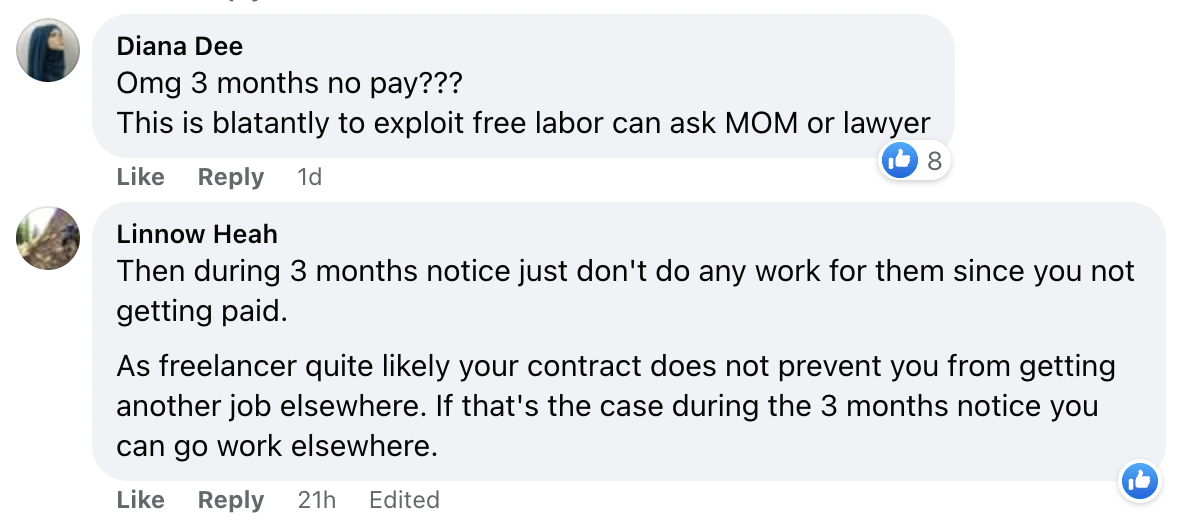

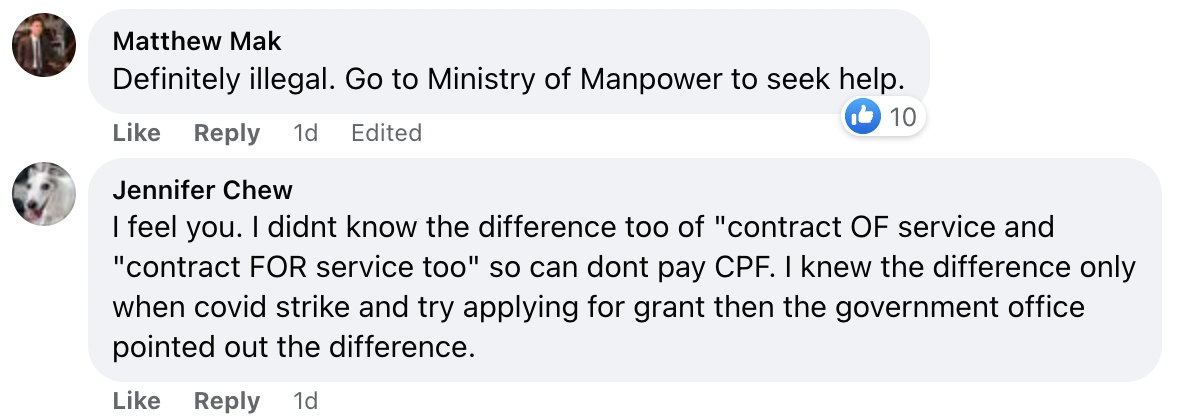

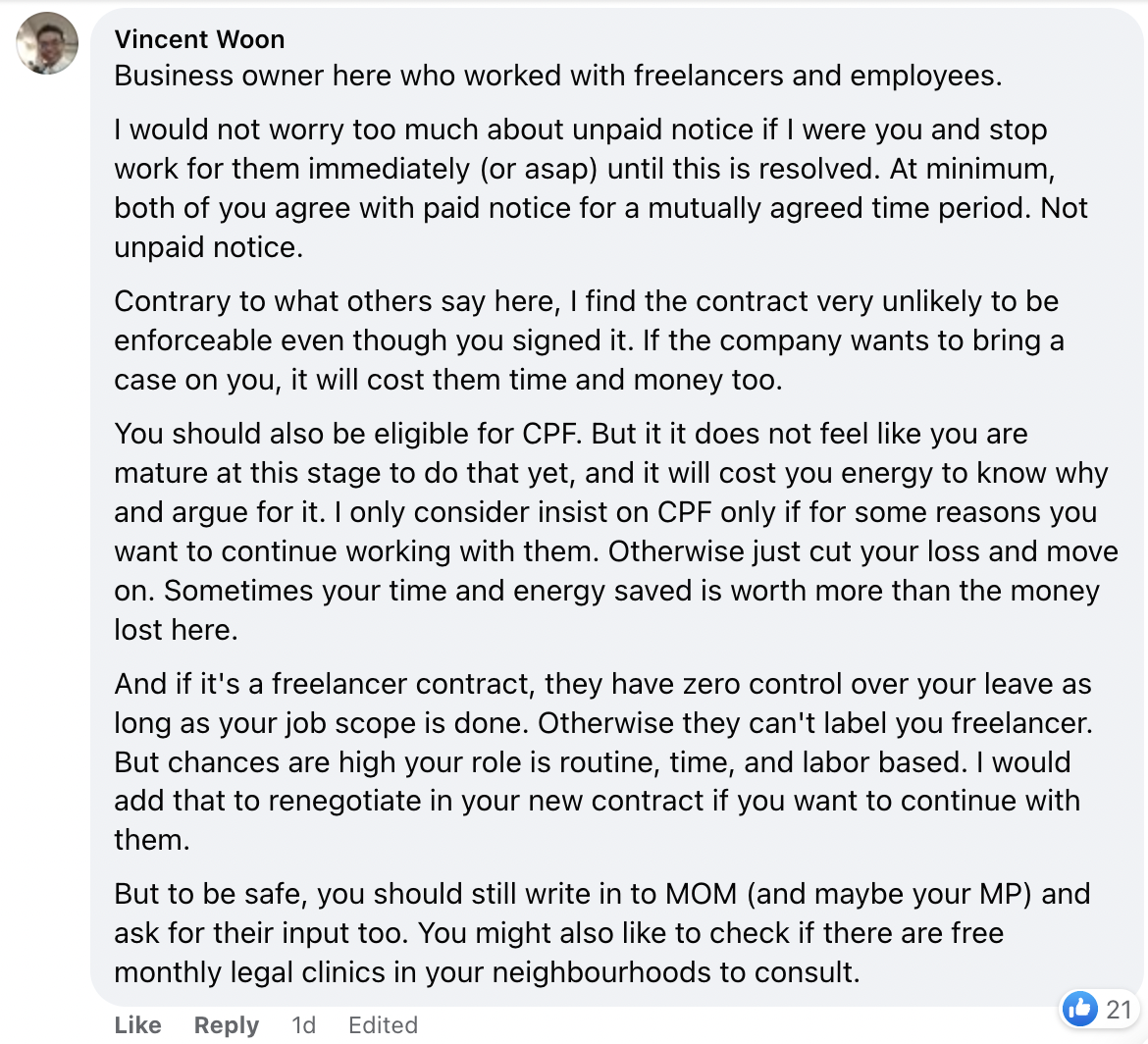

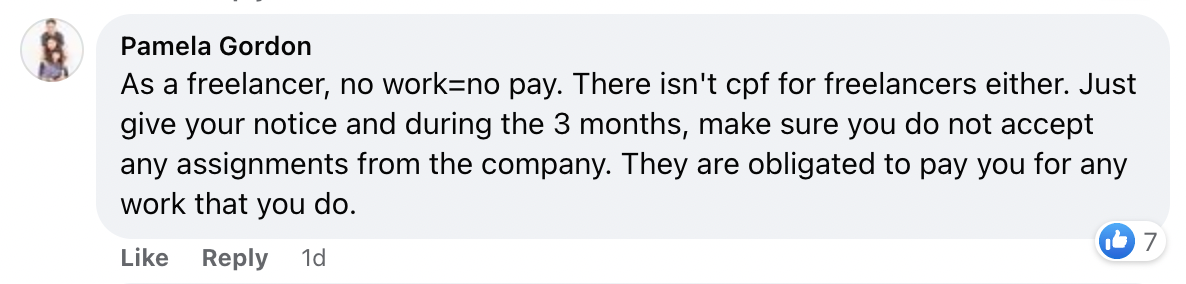

A polytechnic student who claims they got tricked into signing a contract with a company as a freelancer and not as a part-timer asked if there was anything that could be done.

The student wrote that while on their school holidays, they decided to get a part-time job. In an anonymous post to popular confessions page SGWhispers, the student wrote that they were able to find a job rather quickly and signed a contract for two years. According to the job advertisement, it was a part-time job.

However, the student wrote: “i did not know the difference between contract of service and contract for service”. Only after signing the contract did the student’s boss say that they had joined as a freelancer and not a part-timer. Because of this, the student wrote, they did not have Central Provident Fund (CPF) contributions from the company and were not entitled to any leave either.

They then added that if they wanted to leave the company before their contract period was over, they would have to “serve 3 months notice as well as receive no pay during my 3 months notice”.

“is this legal ? is there any platform where i can get help ?” the student asked.

Netizens who commented on the post advised the netizen to stop work immediately and leave. They explained that if no work was done by the student, the company would have no unpaid salary amount to withhold. Others also said that the student should approach the Manpower Ministry for help and advice.

Here’s what they said:

In May, a man not been able to find a job for almost two years took to social media asking netizens for advice, especially after a girl who wanted to date him left after she found out he was unemployed.

In a post to popular confessions page SGWhispers on May 10, the man wrote that he had been searching for a supply chain or procurement job for almost two years. He added that he applied in various industries such as construction, engineering, manufacturing, non-governmental organizations (NGO) and even education, but was of no avail.

“I have attended a few interviews where they will tell me they will get back to me but won’t get back. Some Low balled (sic) me and [due] to my current financial situation I will be agreeing to what they are offering but yet they won’t select me”, he wrote.

Similarly, in March this year, a man who wanted his wife to quit her job, so she can stay home and take care of their son got into an argument with her because she threatened to not have another child.

In an anonymous post on popular confessions Facebook page NUSWhispers, the husband wrote: “I always thought it will be best for a parent to stay at home and take care of the house, so that there will be someone to properly supervise the child and ensure proper upbringing, especially if we have another child next time”.

He said this wife said that he did not respect her goals or social life.

“Yes, she previously did say that she intends to continue to work after having kids. I didn’t disagree back then, neither did I agree too, so there wasn’t any promises made? And I didn’t think she will take it seriously cos I thought a lot of women will be open to the idea of staying at home to bond with the child after having one”, he added.

In the latest development in the saga between social media influencer Rachel Wong and the woman she has sued for defamation, a High Court judge turned down Ms. Rachel Wong’s appeal against an order to provide the correspondence between her and two men she is said to have had relations with.

Ms. Rachel Wong, 27, used to be married to Mr. Anders Aplin, 30, a professional football player.

They wed in December 2019 but by the following April, applied for an annulment, which was granted in March 2021.

However, in December 2020, a woman named Olivia Wu featured Rachel Wong in a series of Instagram Stories with the caption: “Cheater of 2020.”

The series implied that Ms Wong cheated on her then-husband.

Ms. Wu, a nurse, is allegedly a friend of Mr. Aplin’s current girlfriend.

Ms Rachel Wong then sued Ms Wu for defamation, saying that her stories had negatively affected her reputation, which had an effect on the business deals and partnerships which she depends on for her living.

In the course of the lawsuit, Ms Wu requested a copy of Ms Wong’s correspondence with her fitness trainer, Mr Han, as well as for Mr Wan, who had been the emcee at Ms Wong’s wedding.

Ms Wu has also asked for the entries in the influencer’s diary concerning Mr Wan.

Mr Clarence Lun, Ms Wong’s lawyer, alleged that this was a mere “fishing expedition” that would transgress Ms Wong’s privacy.

In March, however, the State Courts said that the documents Ms Wu asked for were “plainly relevant” to the case.

All the correspondence between Ms Wong and her trainer from June 2016 to June 2020 were included in the discovery order, as well as all correspondence between her and Wan between June 2018 and June 2020.

The entries in her diary between June 2018 and June 2020 concerning the emcee were also included.

After the State Court’s decision, Ms Wong appealed to the High Court.

But this appeal was dismissed by High Court judge Choo Han Teck on Tuesday (June 28) as the documents were determined to be relevant to the lawsuit.

“In this case, samples of relevant material had been produced and, just to extend the fishing analogy just a bit more, it is not a mere fishing expedition if fish has in fact been spotted,” the judge said.

In May, a man not been able to find a job for almost two years took to social media asking netizens for advice, especially after a girl who wanted to date him left after she found out he was unemployed.

In May, a man not been able to find a job for almost two years took to social media asking netizens for advice, especially after a girl who wanted to date him left after she found out he was unemployed.