A road accident unfolded before a cyclist’s eyes as they rode down the street, “Tour de Singapore” style.

One cyclist was caught on camera sticking too close to another before losing control for a split second. The cyclist then either kicks or gets his foot stuck to a fellow cyclist’s cycle to his left, causing the latter to tumble to the floor.

Here’s how the accident happened based on the footage.

The cyclists travelling down the road/FB Complaint SingaporeThe cyclists stick too close to one another/FB Complaint SingaporeThe same cyclist kicks out his left leg, pushing a fellow cyclist off his bike/FB Complaint SingaporeThe affected cyclist is sent tumbling to the ground/FB Complaint SingaporeThe cyclists continue riding while a fellow cyclist lands on the floor/FB Complaint Singapore

A video of the incident was shared on Facebook page Complaint Singapore by member Clark Tan, sparking multiple criticisms from netizens.

“What’s that? Tour de Singapore?” asked Facebook user Michael Teo.

“What happened to sticking to the left of the road? Why stick to each other? Looks like they were more into racing each other,” added Facebook user Drillrig Singapore.

According to a couple of netizens, the video looked like it was indeed a race, as the road looked like it was closed off.

“Which race is it? Got submit this video to the organiser?” asked Facebook user Darlene Tan.

According to the Singapore Sports Hub website, a Festival of Cycling was held on May 29, from 7:30 am to 1 pm, along Stadium Drive.

The Independent Singapore has reached out to the Singapore Sports Hub to confirm the incident and check on the affected cyclists.

UPDATE: June 6, 2022

Singapore Sports Hub Statement

The SSH has responded and clarified the incident today with the below statement:

The organiser of the Festival of Cycling is the Singapore Cycling Federation (SCF). Their response is as appended.

Comment to be attributed to: Singapore Cycling Federation Commissaires and Technical Commission

This was a race incident that did not impinge the conduct of the race. It was also not necessary to neutralise this category or to stop or even cancel the race. This incident was just one of the categories.

The race venue and field of play is closed to the public and vehicles. There were ambulances and medical on standby at all times during the race.

It is important to note that this is a controlled race environment where participants are well aware of the risks they are taking in this controlled race environment.

Got a juicy story to share? Came across a gross injustice that needs to be heard? Want to have your opinion on current events made known? Email us your story with details and proof! Make your voice known! [email protected]

Got a juicy story to share? Came across a gross injustice that needs to be heard? Want to have your opinion on current events made known? Email us your story with details and proof! Make your voice known! [email protected]

Dear Editor,

I am glad to learn that “Fish farms may be set up near 3 southern islands with high coral diversity, endangered marine life” and Singapore Food Agency is seeking public feedback (TODAY, May 23).

Malaysia’s chicken ban on Singapore on June 1 has more or less disrupted the meat supply market, and the food retailers who rely on selling chicken as the main dish will bear the blunt impact.

No matter what, any disruption of food supply will swiftly prompt Singapore to find ways and means to tackle the issue upfront. Thus, increasing the multiple channels of food supply will undoubtedly ensure the importance of food diversity and enhance the stability of food prices and the sustainability of food supply for Singapore.

Singapore aims to establish large scale marine fish farms and high-tech vertical farming are some of the effective means or channels for ensuring the continuous supply of alternative food to sustain and alleviate the impact of food supply.

However, whoever runs the marine type fish farms have the obligation to protect and preserve the marine environment. And, they shall take all the necessary measures to ensure that activities under their jurisdiction or control are so conducted as not to cause damage by pollution to the surrounding sea areas. In due course, protecting deep-sea coral habitats from physical damage caused by fish farming infrastructure and polluted water discharge from fish farms is critical.

The selection of the right type and method for marine aquaculture should also be an important consideration for the relevant authorities or commercial parties. This will ensure the projects are commercially viable and environmentally non-polluted. For example, whether going for Open Net Pens, Submersible Net Pens or Recirculating Systems should be duly considered, planned, organised and executed.

Another vital consideration is to ensure the navigation waterways around these specific islands are free of pollution and traffic congestion.

Last but not least, would the present Jurong Fishery and Senoko Fishery Port be sufficient and capable enough to support the logistics requirements to and from the market and the specific fish farms?

Most importantly, would the benefit of financial gain from fish farming be eventually channelled to the hands of the vast consumers?

Teo Kueh Liang (Mr)

The views expressed here are those of the author/contributor and do not necessarily represent the views of The Independent Singapore.

It may sound impossible for some who may also believe that it is a hoax but no, it happened and reports say it is a rare condition for some women. The mom, who gave birth to twins, now says it is a miracle.

‘I 100% believe it was a miracle just because of everything that happened in my pregnancy journey.’ The 30-year-old had three miscarriages before becoming pregnant again… while already expecting.

Her condition called superfetation is an extremely unusual occurrence in which a second pregnancy occurs days or even weeks following the first.

Cara, from Texas, asked the doctor, “What happened?” when she found out she was pregnant again. The first time he wasn’t there, he wasn’t there. ‘What the hell is going on?’

‘She said I ovulated twice, discharged two eggs, and they were fertilised at various times, about a week apart,’ she continues.

Cara had three miscarriages – one of which nearly killed her. She told the story of this miscarriage that could have ended her life.

She told the news outlet Metro which carried her story in the U.S., that her baby was stuck in her cervix and there was a lot of blood.

‘I blacked out and they said that the tissue, which I guess is what they call the baby, had gotten stuck in my cervix and I was bleeding out and they said if I had stayed home for maybe thirty more minutes I would have died.’

In March 2021, the math interventionist tutor learned she was expecting a child. After several ultrasounds, she heard the good news.

The doctor informed her that she was expecting a baby.

Cara went in for a seven-week ultrasound two weeks later to make sure there was still a heartbeat, but there were two foetuses.

The scan revealed that she was expecting two twins, one conceived a week apart.

A man took to social media to complain that he was charged 20 cents more for his breakfast order without being given a reason why.

In a Facebook post to popular page Complaint Singapore on Sunday (May 29), the man wrote: “I want to complain…why kopi C siew dai need to add 20cts”.

The man, who went by the name of Ahmad Syah, added that his was a dine-in order. He also noted that he was told that the additional 20 cents were imposed regardless of whether it was a take-away or dine-in order when he asked the cashier.

In his post, the man shared a photo of his receipt, without confirming where he ate at. Mr Ahmad however stated in the comments that he dined at a coffee shop. As per his receipt, he had a Signature Breakfast Set which was $2.60. It came with toasted bread, an egg and a cup of coffee (Kopi). Mr Ahmad was also charged twice for a ‘TA Cup’, presumably a takeaway cup, 10 cents each time.

Netizens in the comments speculated that Mr Ahmad was made to pay the extra money for the evaporated milk added to his Kopi C order. However, there were others who also explained that usually they were only charged 10 cents for the evaporated milk, but he was charged 20 cents.

Netizens added that the drinks usually included in the breakfast set were Kopi, Kopi O, Teh or Teh O (coffee, black coffee with sugar, tea, or plain tea with sugar) only. They wrote that because he wanted to change his drink to one outside the standard orders, he had to pay more. Some netizens who worked in coffee shops also weighed in on the matter.

Here’s what they said:

In April, tracking the prices of “Economical” Bee Hoon (fried noodles), one netizen pointed out the price jump, adding that he would starve to death soon if prices kept increasing.

In a post to Facebook group Voice Your Grievances, a netizen who goes by the name of Bob Sim writes: “Economical beehoon no longer econ”.

He shared a photo of a plate of bee hoon and noted the following price increases:

Beehoon 80 cents before, now $1.20

Vegetables were 30 cents before, now 70 cents

Egg 50 cents before, now 60 cents

Spring roll 80 cents before, now $1

“This plate used to be $2.40, now $3.50”, he added.

“I gonna starve to death soon if this goes on”, Mr Sim wrote.

The announcement from Finance Minister Lawrence Wong regarding the planned Goods and Services Tax (GST) hike in 2023 has sent many Food & Beverage (F&B) operators into a worried frenzy, with many increasing prices ahead of time to brace themselves.

A post on Facebook page SG Opposition by netizen Kelvin Pek showed a photo of a stall’s ‘Price Adjustment for Noodles’. Though the sign itself did not say if the prices were increased or decreased, the netizen who posted it – one by the name of Kelvin Pek – wrote that the noodles were increased from S$3.50 to S$3.80.

In his post, Mr Pek tagged Mr Wong and wrote: “Lawrence Wong, please tell Singaporean[s] what your anti profiting committee has done to ensure this hike, from $3.50 to $3.80 way before your GST hike, a mere 1% coming in 2023 has cause Singaporean to pay at least another 8% more as consumers”.

“So can you imagine what will the cost be in 2024 when another percent is raised? $4, $4.2? Is there even an anti profiting committee to begin with…”, he added.

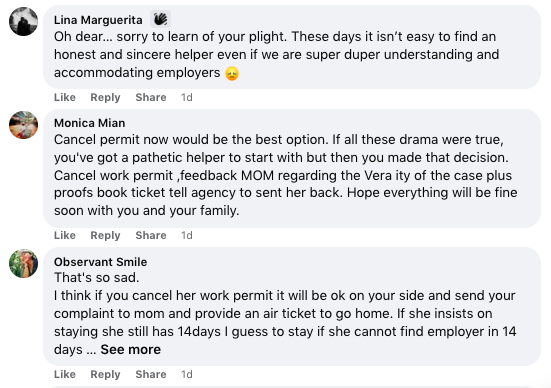

After a number of posts from foreign domestic workers asking for help with problems they faced with their employers, the tables have now been turned, and an employer took to social media asking for advice on her problematic full-time maid.

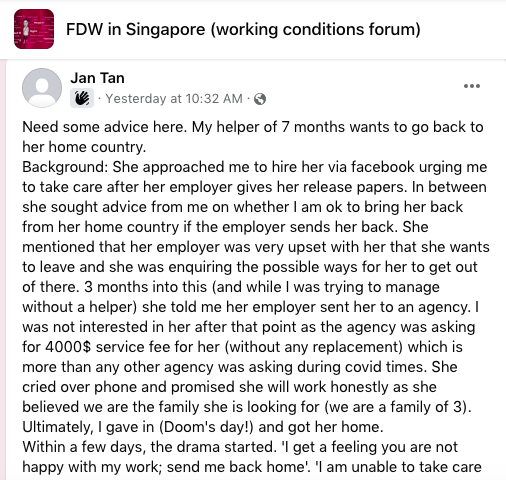

In a throwaway account, probably to maintain anonymity, one Jan Tan wrote to popular Facebook group FDW in Singapore (working conditions forum) on Tuesday (May 31).

In her post, Ms Tan shared that the helper contacted her through Facebook “urging me to take care (of her) after her employer gives her release papers. In between she sought advice from me on whether I am ok to bring her back from her home country if the employer sends her back”.

The maid told Ms Tan that her employer was upset with her, which is why she wanted to leave. Three months later, the maid’s employer sent her to an agency. Ms Tan said that her agency was asking for a $4,000 service fee, without offering to provide a replacement “which is more than any other agency was asking during covid times”.

The helper cried over the phone to Ms Tan, and they eventually gave in and brought her back.

Ms Tan wrote that within a few days of them bringing the helper back, she would come up with excuses such as ‘I get a feeling you are not happy with my work, send me back home’ or ‘I am unable to take care of your child, so [I] want to go’.

Ms Tan wrote that she tried to convince the helper to stay and adjust to the work. Evaluating her work, Ms Tan added that the helper was independent, but that she would not communicate. Instead of talking, the helper would send messages via WhatsApp Messenger and be unhappy if the family complains about anything.

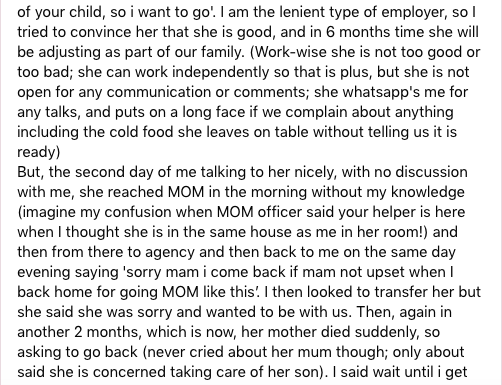

One day, Ms Tan receives a call from the Ministry of Manpower (MOM): “imagine my confusion when MOM officer said your helper is here when I thought she is in the same house as me in her room!”

Without her employers knowing, the maid had gone to the MOM and then back to her agency. Speaking to her employers, she then said she would come back to the house if they were not upset with her for going to “MOM like this”.

Though Ms Tan wanted to transfer the helper out, the helper apologised and said she still wanted to work with the family. Two months later, claiming that her mother had passed, the helper asked to go back home. She never cried about her mother, wrote Ms Tan, adding that she only seemed worried about her son. The maid was asked to wait until a replacement was found for her.

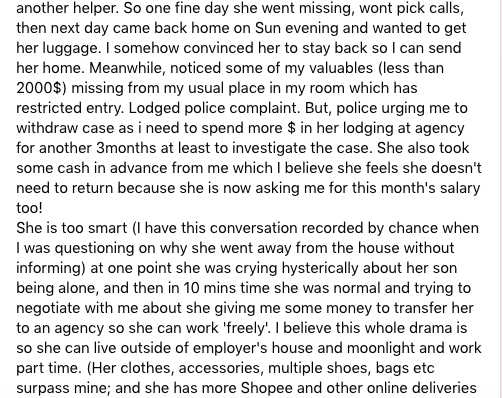

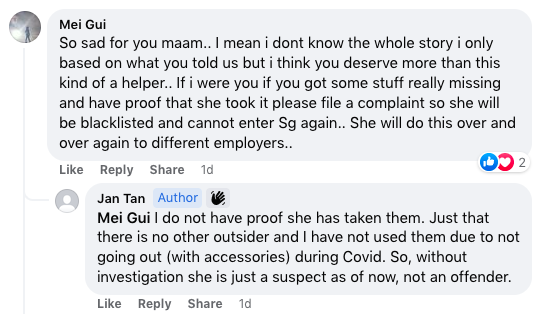

“So one fine day she went missing, won[‘]t pick calls, then next day came back home on Sun evening and wanted to get her luggage. I somehow convinced her to stay back so I can send her home. Meanwhile, noticed some of my valuables (less than 2000$) missing from my usual place in my room which has restricted entry”, Ms Tan wrote.

She added that the helper also took some cash in advance from her, which the helper assumed she would not need to return, as she asked for her full salary at month end as well.

While speaking to her maid, Ms Tan wrote that “at one point she was crying hysterically about her son being alone, and then in 10 mins time she was normal and trying to negotiate with me about she giving me some money to transfer her to an agency so she can work ‘freely'”.

Ms Tan added that she believed the maid’s plan was to be able to live outside of her employer’s house, enabling her to moonlight and work part-time. She added that the helper’s clothes, accessories, multiple shoes, and bags surpassed her own, “and she has more Shopee and other online deliveries coming in for her than I can order for my entire household-this definitely cannot be from the 500+$ salary”.

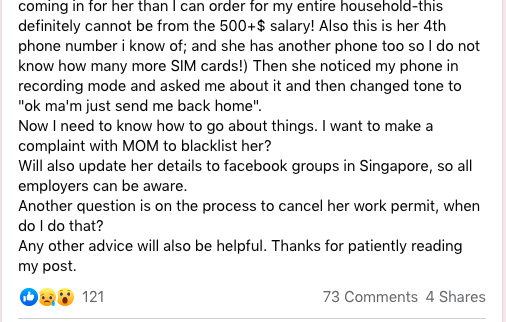

Ms Tan also added that the helper had at least four SIM cards that she knew of.

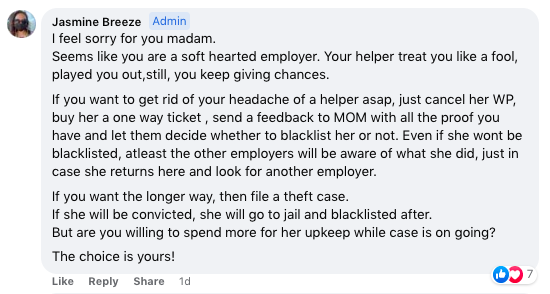

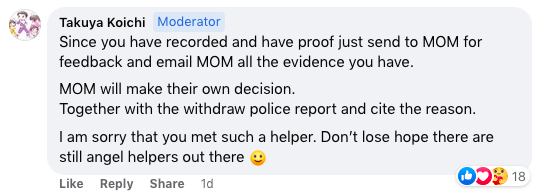

Asking for help as to what to do, Ms Tan wanted to know how to go about blacklisting the helper and how to cancel her work permit. She also asked other members of the group for any advice they could give her.

Those who commented on Ms Tan’s post asked for more information, such as how Ms Tan knew the helper stole her items.

Here’s what they said, as well as Ms Tan’s response:

TISG has reached out to Ms Tan for comment and clarification. /TISG

After speaking to a Bangladeshi man on the MRT, a netizen was surprised to learn that the former managed to build a 3-storey house.

In a post to Facebook group Singapore: Pitfalls and Reviews, a netizen who goes by the name of Victor Chan wrote that he had a small conversation with a Bangladeshi man on the MRT.

Mr Chan said that the Bangladeshi man worked here in Singapore, earning a salary of $3000 a month.

“He showed me a picture of his newly built 3-storey home+land all-in for S$60,000”, Mr Chan added.

While Mr Chan’s post itself was fairly short, it stirred up sentiments about the cost of living in Singapore as compared to that of other countries. Netizens who commented on the post also spoke about how expensive housing here is.

Here’s what they said:

At the beginning of the year, in his New Year’s Day Message, Workers’ Party Secretary-General Pritam Singh underlined that cost of living would be a “major pressure point” for many households in the coming year.

Mr Singh, who is also the Leader of the Opposition, said in a message that was posted on The Workers’ Party’s Facebook page and on its Telegram channel on the last day of 2021 that increased cost of living rates would affect low to middle-income families, especially those with both elderly relatives and young children to take care of.

This, aside from the unpredictability of COVID-19,” will make “2022 will be a year of new challenges for Singapore and Singaporeans,” the WP head said.

He outlined basic needs which now have higher costs, including electricity, transport, A&E hospital charges, and medical insurance premiums, and added that these “cost pressures that are likely to become more acute going forward.”

Mr Singh also mentioned the housing problem, as “HDB BTO prices remain high for younger Singaporeans, with resale flats even further out of reach for many.”

HOWEVER, HE UNDERLINED THE WP’S COMMITMENT TO MONITOR THE GOVERNMENT’S EFFORTS TO AID SINGAPOREANS IN NEED OF THE MOST HELP; “AND HOW IT UPGRADES ITS LEGACY SCHEMES FOR THE CIRCUMSTANCES OF TODAY AND TOMORROW, NOT YESTERDAY.”

He also said the party would continue in its mission “to provide a trusted alternative to voters and act as a balancing force in our political system” and highlighted some of the motions WP MPs have moved this year, including those related to HDB reform. /TISG

Today, there are many financial tools available to make payments in Singapore; Traditional methods like cash and credit cards, as well as newer digital platforms such as Apple Pay and GrabPay.

Some enjoy the physical thrills of wielding cash and credit cards to make payments, while others prefer the convenience that digital payments bring, with these digital platforms integrated with their smartphones.

However, do you know that if you are smart about how you pay, you can save a significant amount of money in the long run?

In Singapore where there is a steady inflation rate of 2-3% each year, how are we able to best utilize the many payment methods out there in the market to earn the best deals and rewards for ourselves to combat this inflation?

Read on to find out more on how you can save as you pay.

Credit Cards

Credit card companies are constantly competing to offer the most appealing rewards for their consumers; Some cards offer lucrative sign-up rewards, while others give higher cashback for spending categories such as air travel, food and transport.

Cashback Cards

Cashback cards are a convenient alternative to points and miles cards that can offset your monthly card bill by earning rebates on specific kinds of spending.

To find the best cashback credit card that maximises rebates for your budget based on your income and spending numbers, check out our rewards calculator to compare between credit cards and see what value you could get from each cashback card in Singapore.

Below is a list of credit cards suitable for every need:

Best Unlimited Cashback Credit Card: Citi Cash Back+ Card

Individuals spending about S$7,000+/month can truly maximise their earnings with Citibank Cash Back+ Card. Cardholders earn an unlimited 1.6% cashback on all spend, which is higher than the 1.5% offered by most competitors. In most cases, consumers with very large budgets end up feeling restricted by typical capped rewards cards. With Citi Cash Back+, however, affluent cardholders can continue to earn on all of their spend, up to their full rewards potential.

Best Rewards Credit Card: UOB One Credit Card

If you consistently spend S$2,000/month, you’ll earn more with UOB One Card than with any other flat rebate card. Spend at this level earns 5% cashback, up to S$300/quarter–amongst the highest earning potentials on the market. This rate is further boosted to 10% on Dairy Farm Singapore transactions, Grab and UOB Travel and 6% on electric bills. Lower or inconsistent spend also earns 3.33% up to S$50 or S$100/quarter (depending on minimum spend), but these rates are slightly less competitive.

One of the best features of UOB One Card is that cardholders can ‘double’ their rebates through UOB SMART$ Programme, which also earns SMART$ credits with select merchants, which then offset future purchases. With UOB One Card, consumers can make the most of their daily spend, while only paying a S$192.6 annual fee. Overall, this card is the best flat rebate option on the market for average spenders.

1.1 miles per S$1 local & overseas spend, 2 mi overseas in June & December only

2 miles per S$1 spend on SingaporeAir online & app, SilkAir, KrisShop in-flight & online

3.1 miles per S$1 spend on Grab transactions (up to 620 mi/mo)

Free travel insurance

Hertz Gold Plus Rewards & Amex Selects Privileges

If you’re interested in applying for your first miles credit card and tend to fly with SIA, you may want to consider American Express Singapore Airlines KrisFlyer Card. Cardholders earn 1.1 miles per S$1 on general spend (2 miles overseas in June & December), 2 miles with SingaporeAir, SilkAir and KrisShop, and 3.1 miles on Grab rides (up to 620 mi/mo). Rewards are earned directly as KrisFlyer miles, which are credited to the consumer’s frequent flyer loyalty account. This is great because cardholders never have to worry about conversion rates, transfer fees or lengthy processing times. Amex SIA KF Card is also quite affordable with a S$176.55 fee, waived the first year. Overall, if you prefer taking SIA flights and want a straightforward miles card, this could be the option for you.

Best Luxury Travel Credit Card: Citi Prestige Mastercard

Affluent travellers who prioritise luxury perks should consider Citi Prestige MasterCard. Cardholders earn 1.3 miles per S$1 locally, 2 miles overseas, which are amongst the highest rates on the market. In addition, consumers can earn up to 30% annual bonuses based on the length of their relationship with Citibank. Simply using your card over time multiplies your earnings–few alternative cards offer such a bonus structure.

Citi Prestige Card also offers more privileges than almost any other travel cards. Cardholders receive unlimited airport lounge access with no minimum spend requirements, free limo transfers, free hotel bonus nights, golfing privileges and more. While the S$535 fee is high, it’s reflected in the value returned to consumers and further offset by 25,000 annual renewal miles, worth about S$250. Ultimately, market-leading rates and luxury perks make Citi Prestige the best card for affluent travellers.

Best Credit Card with No Annual Fee: OCBC 365 Card

OCBC 365 Card offers a great no-fee way to earn cashback on daily purchases. Cardholders earn up to 6% rebates on dining and 3% on groceries, land transport, online travel bookings and recurring electricity and telco bills. There are no merchant restrictions (unlike competitors) and rewards are capped at a lofty S$80/month. Another perk is that cardholders can enjoy a fee waiver with S$10,000 annual spend – that’s just S$833/month. This spend level also meets minimum spend requirements, ensuring top rewards rates. Overall, OCBC 365 Card is definitely one of the best everyday options with a fee-waiver.

Best Credit Card For Online & Mobile Payment: DBS Live Fresh

If you’re a modern spender who frequently shops online and feels comfortable using digital wallets, look no further than DBS Live Fresh Card. Cardholders earn an impressive 5% cashback for spend in both categories, and an additional 5% on sustainable spend, with a total monthly cashback cap at S$75/month. There is a S$600 minimum spend requirement to access these rates, but it’s slightly lower than the S$800 required by most competitors. Paired with its SimplyGo functionality, DBS Live Fresh Card’s rewards structure is great for people looking to streamline their wallets and maximise rebates from tech-forward spend methods.

Here is an example of using several credit cards with a monthly spend of S$3,000:

Credit Card

Monthly payment

Annual Card Fees

Monthly Cashback

Annual Cashback

Net Savings per Year

UOB One Card

S$2,000 (House/Car Loan)

S$192.60

S$100

S$1,200

S$1,007.40

OCBC 365 Card

S$500 (Food)

S$192.60

S$30

S$360

S$167.40

DBS Live Fresh

S$500 (Online Shopping + Groceries)

S$192.60

S$25

S$300

S$107.40

S$1,282.20

By using the best credit card for individual spend categories, you can maximise your cashback and save up to S$1,282.20 every year.

With the increasing number of digital payment options and each offering varying rewards and promotions, how are we able to identify which is the best platform to use to get the best deals for ourselves?

Listed below are some platforms we have identified for you and how to go about getting the best deals.

GrabPay

Since its launch in 2016, GrabPay has evolved from an e-wallet with basic payment features to a popular payment option in Singapore.

Although Grab has seen a devaluation of its points across transactions back in January 2020, Grab remains to be a popular payment option with its wide merchant acceptance pool and ever-increasing partnerships to offer more lucrative rewards to its users. You can still continue to maximize the opportunity to earn points and cash rebates across all platforms with GrabPay.

Here’s how to do so:

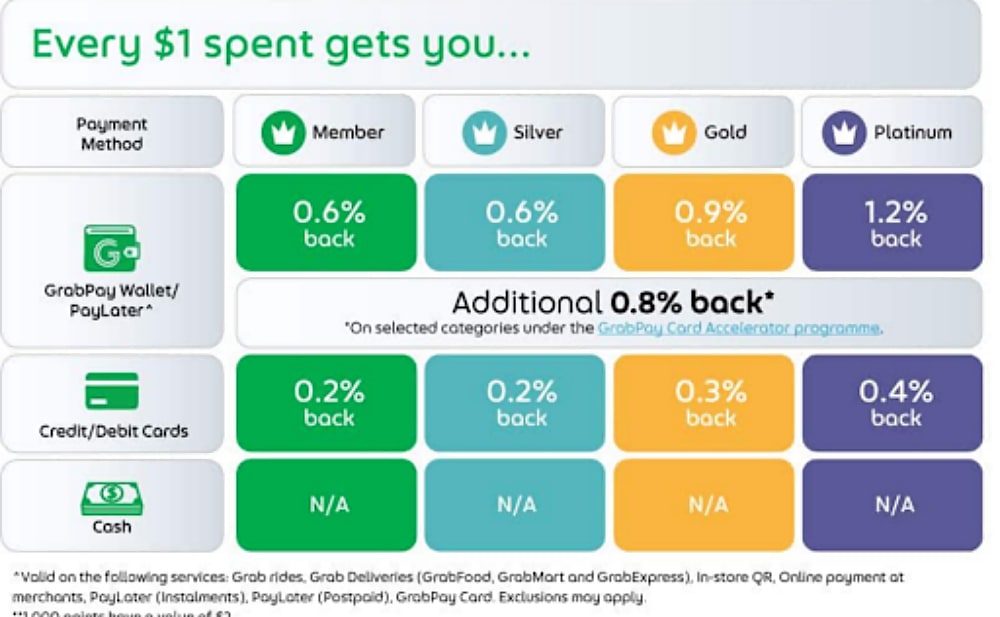

GrabPay Card Accelerator

For those who want to maximize the number of Grab points earned, the GrabPay Card accelerator allows you to earn an additional 0.8% cashback, on top of your current cashback based on your membership tier, by spending on selected categories:

Do take note that booster points are capped at a maximum of 20 transactions per month and 500 points for each transaction. Strategise well to make full use of this reward scheme!

Linking your GrabPay Account to other platforms

Besides using your GrabPay wallet or Mastercard at merchants, you can also maximise the potential of earning additional cashback by linking your GrabPay account to other platforms such as the Fave App or Samsung Pay.

This approach allows you to earn GrabPay points, cashback from FavePay transactions as well as Samsung Reward points. For the same spending, you earn double to triple the points.

That’s not all, some credit cards issue points or cash rebates for topping up their e-wallet using their credit cards, including GrabPay.

This means that you can continue to stack the rewards with the same spending!

Use GrabPay for your daily expenses

Using GrabPay for your expenses allows you to reach higher membership tiers and earn Grab points faster with every purchase.

Source: Grab

Assuming that you are a Platinium member, you could earn up to 9,800 Grab Points with a monthly expense of S$1,000. Here is a breakdown of how to do so:

Categories

Money Spent

Points Earned

Additional Points (Accelerator)

Total Points Earned

Groceries

S$300

1800

1200

3000

Dining

S$300

1800

1200

3000

Transport

S$50

300

0

300

Streaming Apps

S$25

150

100

250

Online Shopping

S$200

1200

800

2000

Gym

S$125

750

500

1250

S$1,282.20

Here are some of the redeemable rewards from the various categories available on the GrabRewards catalogue.

Food & beverage:

1,500 points: $3 off merchants such as Gong Cha, or a personal pizza from Dominos

2,500 points: $5 off merchants such as Burger King, Crave, ToastBox and SaladStop!

5,000 points: $10 off merchants such as Marche Movenpick, Hans Im Gluck, and Dunkin’ Donuts

Shopping:

2,500 points: $5 off merchants such as Cold Storage, Giant, Guardian, and Sephora

5,000 points: $10 off merchants such as Foot Locker, RedMart and Zalora

10,000 points: $20 off merchants such as Lazada, Tangs, Amazon, and EAMart

Services & Entertainment:

5,000 points: 500 KrisFlyer miles, $10 off merchants such as Kimage and Perky Lash, $10 gift card for Blizzard Entertainment and Razer Gold, Everyday movie voucher from Cathay

Alternatively, you could use the points to offset purchases within the Grab App, such as GrabMart, GrabFood or Grab Car rides.

ShopeePay

ShopeePay is the digital wallet service offered by Shopee. ShopeePay allows you to make both in-app payments and offline transactions by scanning the merchant’s ShopeePay or SGQR code.

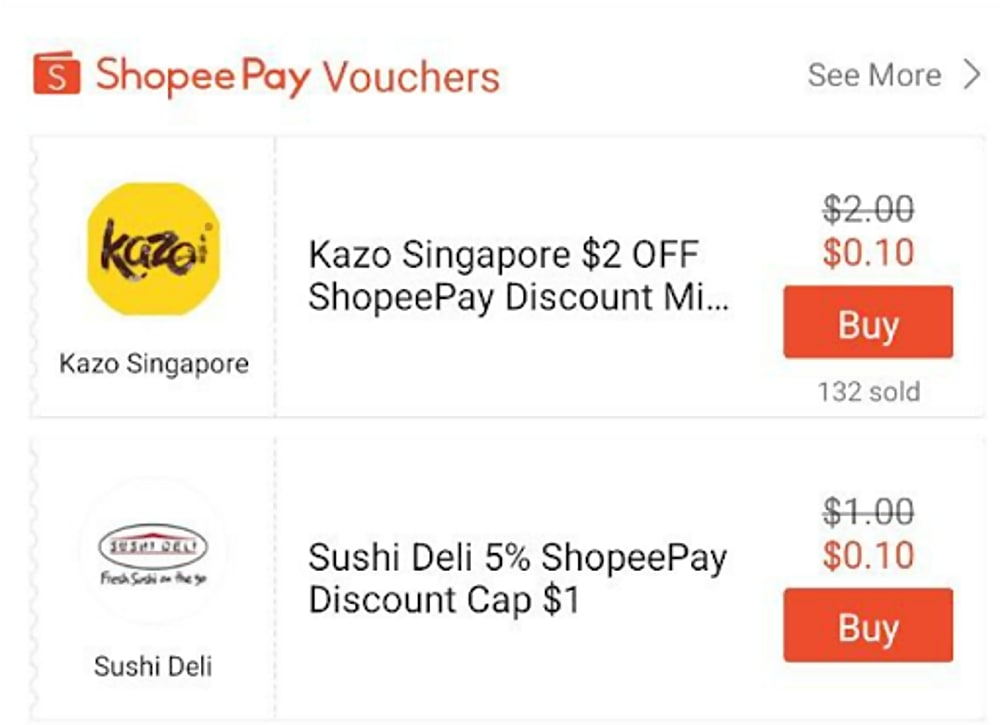

ShopeePay In-app Vouchers

Enjoy upsized cashback vouchers of up to 18% cashback for your in-app purchases. You are able to stack cashback vouchers on top of seller vouchers to enjoy greater savings, especially during monthly sales such as Black Friday or the 11.11 sale.

Source: Shopee SG

In addition, you could stand to win seasonal prizes and be part of exciting lucky draw prizes when you top up your account or transfer funds to other users using ShopeePay!

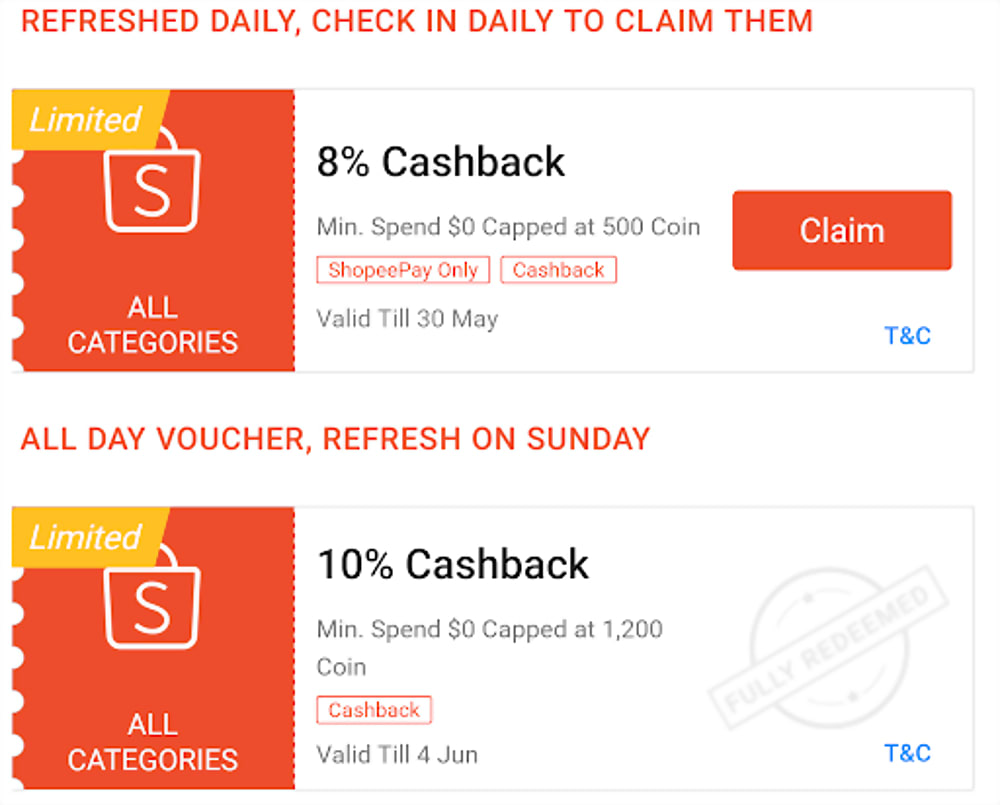

ShopeePay Offline Vouchers

In addition to the 2% cashback capped at $1 whenever you make a payment by ShopeePay, ShopeePay Scan & Pay vouchers offer direct discounts or cashback at the price of S$0.10 or S$0.01. These discounts and cashback vouchers differ from merchant to merchant so do remember to check the app to see what kind of vouchers your favourite brands offer!

Source: Shopee SG

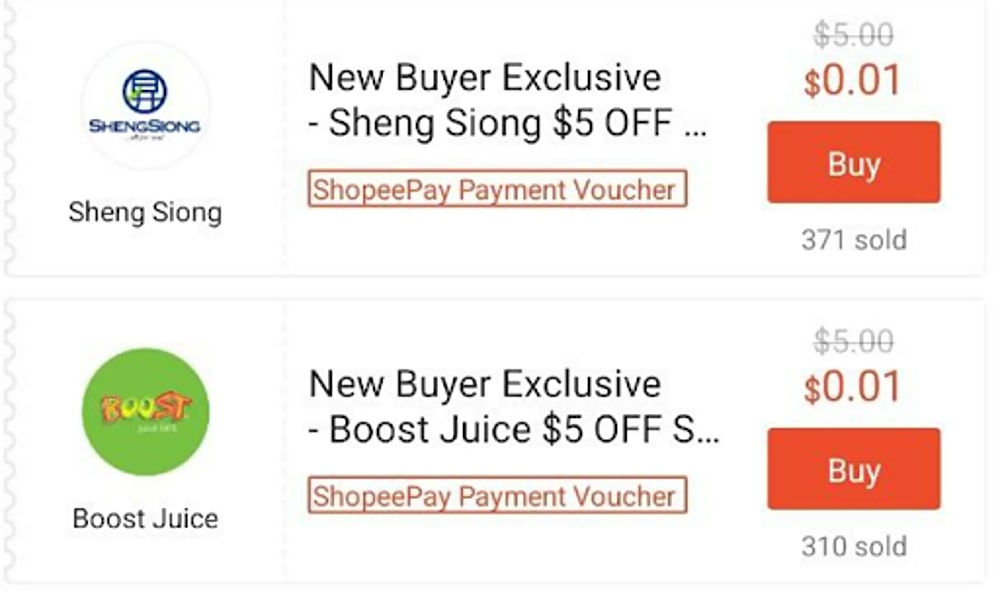

For first time users, enjoy up to $5 off on your first purchase with ShopeePay Scan & Pay vouchers with your favourite brands!

Source: Shopee SG

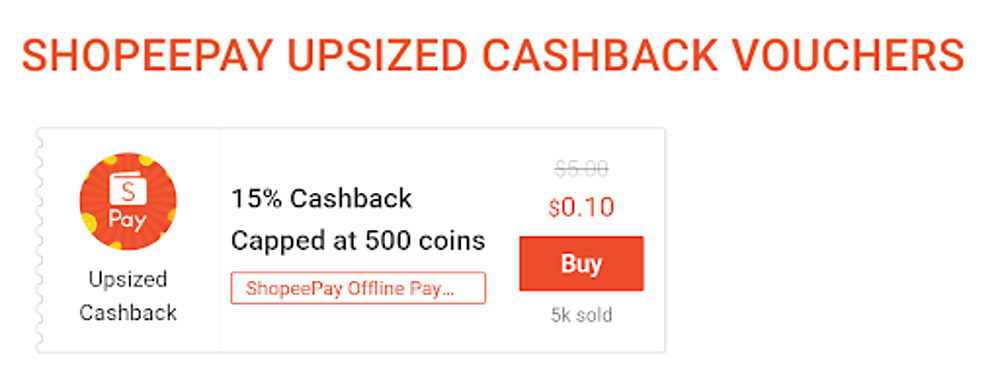

ShopeePay also offers upsized cashback vouchers of 15% cashback capped at 500 coins at the price of S$0.10 which is applicable to all merchants that accept ShopeePay as a payment method.

Source: Shopee SG

However, do take note that these vouchers are not stackable. In addition, users are limited to one voucher per visit. Be strategic about when and what you use the vouchers on!

ShopeePay Promotions & Giveaways

During major events such as the 11.11 sale or the celebration of Shopee’s birthday on 12.12, be on the watch out for ShopeePay rewards to reap the best benefits!

Promotions during the 11.11 sale include: Plant a ShopeePay seed on Shopee Farm from 8 Nov to 14 Nov with a minimum top-up of $8 to the Shopee wallet and stand to win an additional $100 Shopee vouchers. 90% off deals with ShopeePay. Limited-time only vouchers on popular brands.

How to Make Payment via ShopeePay?

From the homepage of the Shopee application, tap the wallet icon with text below that reads “Top up now for exclusive rewards” to enter the ShopeePay page.

Transfer enough money to pay for your item either via Paynow transfer or your credit/debit card.

When checking out, be sure to select ShopeePay as the payment mode and apply the ShopeePay vouchers (if applicable) to enjoy further discounts or cashback.

Buy Now Pay Later (BNPL)

BNPL payments are all the rage now in Singapore. So, what’s the fuss with BNPL?

BNPL, as its name suggests, allows you to delay your payments and split them up into monthly instalments. Pay your balance on time, and zero interest is charged. If you miss a payment, you would be charged a late payment fee ranging up to S$60, depending on your BNPL provider.

BNPL Provider

Installment

Late Payment Fee

Atome

3 months

S$15 – S$30

Hoolah

3 months

S$5 – S$30

Grab PayLater

Up to 4 months

S$10

OctiFi

3 months

From S$15

Pace

3 months

S$10 – S$60

Rely

Up to 3 months

S$1 – S$40

Split

3 months

None

BNPL has a similar framework to your traditional 0% credit card instalment plans, but with the addition of multiple perks.

Optimise Cashback/Miles on Credit Cards

Suppose you are making an online purchase of S$3,000 on a desktop computer using your OCBC Frank Card that gives you a 6% rebate capped at $75 per month.

Although there is a 6% rebate offered that should warrant you a cashback of S$180, there is a monthly cap of S$75. Hence, you are only able to get back S$75 and miss out on S$115.

How are you able to ensure that this S$115 that you have missed out on goes into your bank account? Do you look for another credit card with a higher cap per month?

BNPL solves this problem without the need to look for alternative credit cards or payment methods. Suppose you put the purchase on a three-month instalment plan with Atome. Each month you are charged S$1,000 and awarded a cashback of S$60, a figure below the monthly cap of your Frank Card. After three months, you will have received a total of S$180 in cashback.

Earn Additional Interest in Bank Accounts/Insurance Savings Plan/Investments

As you will not be paying the full amount upfront via BNPL, you will be able to keep a sum of the amount for a period of one to two months and receive interest on the balance in your bank account or insurance savings plan or receive earnings on your investments.

Although this may not amount to much depending on the interest rates your bank or savings plan offers, who would say no to money!

Additional Rewards & Perks

Since BNPL payment services are rather new in Singapore, BNPL providers are giving attractive rewards to attract and acquire customers, so as to gain a larger market share.

Atome: S$10 off first online purchase. Merchant-specific discount vouchers.

Pace: OCBC Yes! Debit Card holders S$50 off with min. spend S$250. Merchant-specific vouchers.

Rely: 12% cashback on the first transaction. Merchant-specific cashback vouchers

Conclusion

There are so many payment methods out there in the market with attractive rewards and perks. Some prefer direct cash discounts, others prefer cashback rewards, while the rest prefer to pay in instalments.

What is your preferred method of payment to maximize your savings?

Grace Beverly believes that working hard and hardly working are two different sides of the same productivity coin. Studying at Oxford University and throughout her career, she realized that one of the biggest challenges people have is balancing work and time out in a way that works for them.

The truth is, all of us need money, but we also want careers that challenge us. To that end, Beverly has a number of tips from her book Working Hard, Hardly Working.

Time management

The Eisenhower method of time management is a prioritization plan that helps work out what is urgent and important and the order in which things need to be worked on. The idea is to divide tasks into categories such as urgent; important;delegate and don’t do.

Save dates in your diary

The next step is to put each task from the list into your calendar and “time block” it according to how long you need. You can then plan tasks or meetings around this. This helps you sort out administrative tasks easily, too.

Change your to-do list to a to-do table

All tasks are not created equal, and therefore a table format is better than a list. Divide it into three columns; Quick Ticks (things that take 5 mins or less), Tasks; (which can go up to 30 mins) and Projects (the Herculean ones that need more time). Also include things that won’t get done in a day but need to be monitored.

Get into ‘deep work’

Deep work is about reclaiming concentration and committing to work without the constant distraction and the ping of notifications. It’s like having an exam in school.

Do nothing

This one seems contradictory to all of the above, but it isn’t actually. Scheduling a time for doing nothing actually prevents burnout from doing too much. It should be a planned exercise for our lives. So a ‘planned’ nothing could be anything from keeping two-week nights free to taking a whole day off on the weekend to do nothing.

Figure out what makes you feel good

Cancel a plan, make a plan, and give yourself a treat — anything that helps you feel better that isn’t destructive is a good thing.

Make sure you don’t overdo a good thing

Once you know what’s good for you and how to relax when you need it, don’t get complacent. Make boundaries which can be time-related, space related or task-related. Make specific areas in your home for where you work, where you sleep, and whether you can or want to work on a weekend. For example, you could decide to work some Saturdays but never on a Sunday.

Watch out for self-sabotage

Most of the time we can feel ourselves doing this, we know we would feel a lot better if we go for a run or get some fresh air, and yet we do nothing. Sometimes we have to push ourselves a little bit to feel better in the longer term. If you force yourself to do something, and it doesn’t feel good both in the medium and long term, then you know you were right.

Losing your job and dealing with the stress that comes with it is really hard to cope with, especially when you have bills to pay and a family to support. Whether you’ve been retrenched, downsized or forced to leave for other reasons, the financial anguish takes a huge toll.

Careers give us a sense of purpose and structure, and losing all of this can leave people floundering and feeling lost. It also makes an individual feel powerless. But take heart that no matter how impossible the situation looks, there is always light at the end of the tunnel.

Author of the book The Importance of Work in An Age of Uncertainty: The Eroding Work Experience in America, Professor David Blustein says that work helps us satisfy our need to achieve, earn an income, and connect with others and feel like authors of our own stories. In fact, our jobs are often so integrated into our identities that it is common to feel as though we have lost a sense of self when we lose our jobs.

Getting a hold of yourself

Understand that it is perfectly normal to feel disappointed, sad, angry or frustrated and process this accordingly in order to move on. In addition, if you feel relief instead, it could mean that you weren’t happy there anyway and not living up to your full potential, so take that as a sign to move on to greener pastures.

Emotional support and finances

Make sure you have your family or some good friends around to support you during this trying time. If you have a family depending on you for financial support, talk to them about how your job loss will impact all of you and what sort of changes or cutbacks you may need to make going forward.

Expand your social network

Often our work friends form part of our social life as well since inevitably you end up spending so much time together. So when you lose your jobs, you may lose friends too or simply drift apart. Find ways to connect with people, whether it’s doing volunteer work, joining a book club or simply getting out more.

Develop new skills that are marketable

Figure out how you want to move forward. Develop new skills that will help you in your next job and make you more marketable. Think about what you want to do next and work towards that, building on developing yourself to achieve that goal.

Update your resume and start applying for new opportunities

Create a portfolio which you can present to a recruiter or hiring manager to showcase your work from previous roles. Doing this will also make you feel more confident and good about yourself and your past achievements.

Once this is done, go all out for the jobs you want, and don’t be disheartened if you don’t hear from employers in the beginning. If you have been rejected at the interview stage, try and find out the reason for this so that you can look towards filling in the gaps in terms of the requirements, allowing you to aim for the role you really want.