Singaporean banks have been raising their fees like credit card charges in the recent months. What people may not realise, however, is that this fee hikes may continue for a long time, even several years. Here, we explain why bank fees are rising, why it will likely continue to rise over the next few years, and why consumers need to start preparing for it well in advance.

How Banks Make Money

Banks make money mostly on interest spreads. This means that they borrow money at relatively low interest rates, and lend them out at higher rates for profit. Therefore, banks generally measure their profitability in terms of their net interest margin (NIM), the spread between the rate they earn on loans and the rate they pay on deposits. Banks also charge fixed fees on their various value-add services to supplement their interest income.

When banks determine how much interest rates or late payment fees to charge, they generally maintain a spread against a reference rate like SIBOR. One of the key factors that influence the cost side of this is interbank lending rates, because banks lend to one another frequently for liquidity reasons.

Rising Fees: It’s Not Entirely the Bank’s Fault

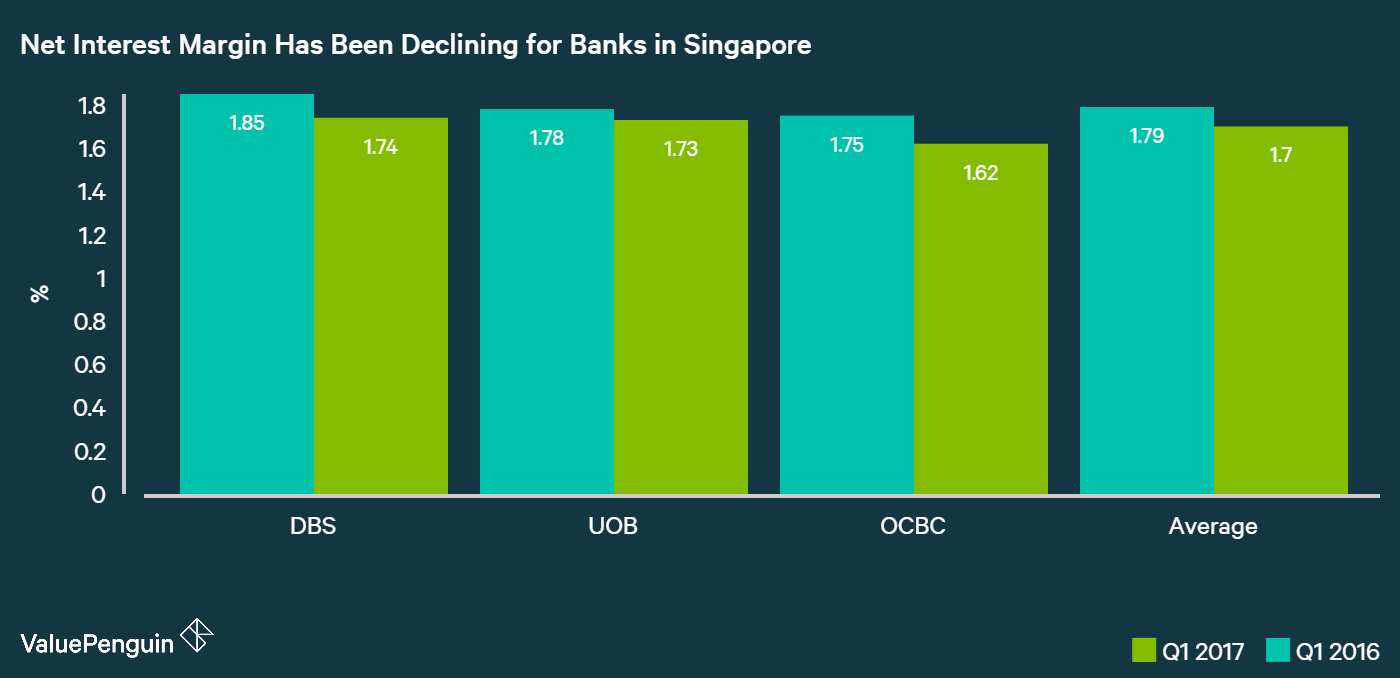

However, the problem is that banks in Singapore (and globally) recently began to face a headwind: rate hike in the US. When SIBOR rises, banks need to adjust the interest rates on the loans that they make in order to maintain their profitability. However, the rate they earn on their loans (which tend to be long-term) don’t adjust as quickly as the rate they pay on their liabilities (i.e. deposits, interbank lending, etc.). Therefore, as rates began to rise, their profitability in terms of NIM began to shrink, as we show for the 3 major Singaporean banks below.

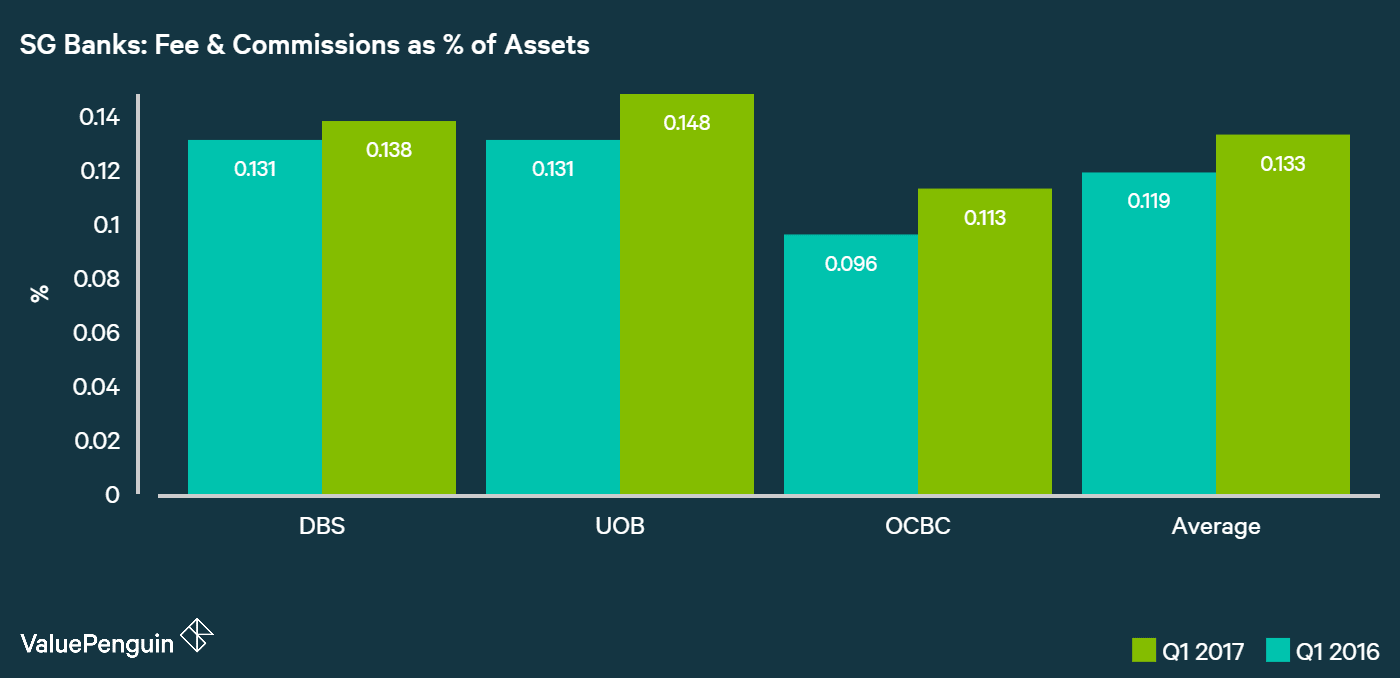

When Sibor spiked in 2015 when rates in the United States began to rise, and again this year, albeit slightly due to foreign exchange fluctuations, Singapore banks suddenly found themselves with a higher cost basis and lower NIM. In order to maintain their profitability, therefore, they had to hike their various fees accordingly. For instance, the top 3 banks’ fee and commission income as % of their assets increased by 12% on average in Q1 2017 compared to Q1 2016.

Why Fees Are Likely To Continue Rising

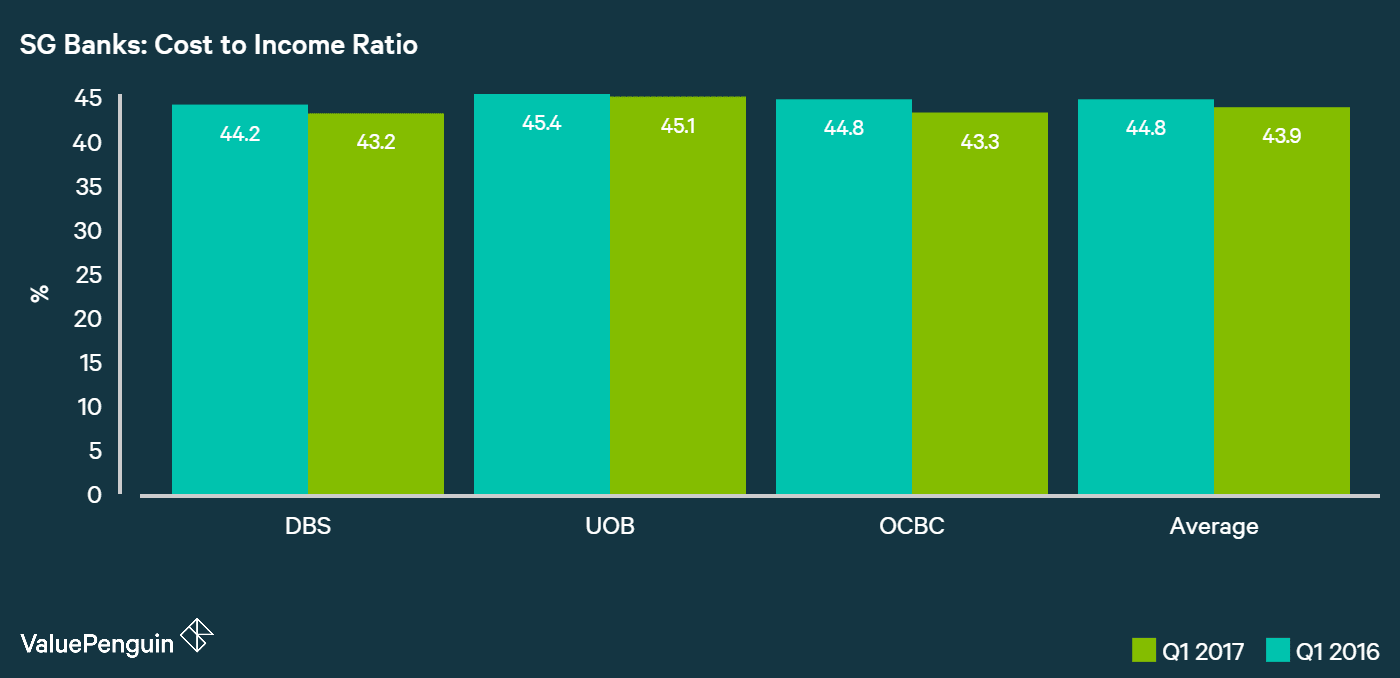

Because SIBOR is very correlated to the interest rates in the US, it began to rise since the US Fed decided to increase its rates over the next few years. The fact that US rates are poised to rise again for the next several means then means that banks’ NIM might be under pressure for much longer, and that those banks may need to continue to raise their fees to protect their profitability. For instance, despite the fact that their NIMs declined from 1.79% to 1.7% on average in just 1 year, the top banks in Singapore were able to maintain a stable cost to income ratio of around 43.9%, which actually declined from 44.8% from a year ago, thanks to their fee hikes.

Bad News for Consumers With Poor Financial Conditions

This is a very bad news for consumers who have a tendency to be late on their credit card bills or loan repayments. It may have been relatively “easy” to handle extra charges of S$40 to S$60 whenever you were a week or two late on your debt obligations. Now, this may cost you up to S$100 just for a late credit card payment.

What this means for consumers is that they should start to reduce their liabilities meaningfully going forward. With average household debt on the rise, we estimated that each 0.25% increase in SIBOR could cost Singaporeans almost S$800mn of extra interest payment per year. Higher late charges and other fees can be an additional burden that can be a meaningful blow to their spending power. Therefore, if you have racked up a lot of unpaid credit card bills, personal loans or even home mortgages, it may be a good time to start funneling more of your funds towards repaying your liabilities instead of buying things.

The article Why Consumers Need to be Ready for a Continued Rise in Bank Fees originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

- Best Credit Cards with Promotions 2017

- Best Personal Loans in Singapore 2017

- Best Debt Consolidation Plans 2017

Source: ValuePen