How much will getting into a car accident cost you in Singapore? The answer could be more than you might think. Our team at ValuePenguin took a look at the various ways a car accident could affect your budget in the short and long term so that you can make sure you’re prepared if the worst happens.

Upfront Cost

The most obvious cost of getting into a car crash, i.e. how much money it will cost to return you and your car to your pre-accident conditions, will vary depending on your car insurance plan. If you get into a car accident and are determined not to be at fault for the car accident, whether your car is insured under a comprehensive or third party plan is a moot point. Either way, the other party’s insurer will take care of the immediate costs of the crash, including any losses, damages and medical expenses. But what if you are determined to be at least partially at-fault for the crash?

If you have comprehensive car insurance, you can take a deep breath: your insurer will help to cover the costs of the accident in accordance with your policy. If, however, you only have some form of third party car insurance, you’re on your own, as your plan will only cover any expenses borne by the other party involved in the accident. You will have to pay for any and all associated costs of the accident yourself, including the expense involved in repairing or replacing your car, accessories, and any personal items, any medical bills incurred, etc. Thus, the immediate cost of a car accident will depend on the severity of the accident: how extensive the damages are, how badly you got hurt, and how expensive it will be to repair or replace your car entirely.

Long-Term Costs

Getting into a car accident will also have long-term consequences for your budget, as it can substantially affect how much you pay for car insurance in future years in two significant ways. First, it can deal a painful blow to your No Claims Discount (NCD). Next, merely having filed a claim, regardless of if you were determined to be at fault, may cause insurers to hike your premium. These two factors will separately cause your car insurance premiums to increase from what they were before the accident for years to come.

Effect on Your No Claims Discount

If you are determined to bear over 20% of the liability for a car accident, your NCD will suffer, setting you back at least 3 years from earning the maximum NCD discount on your car insurance premium. Here’s how it works. For each year you drive without having to file a claim, you earn 10% on your NCD, up to a cap of 50%. The higher your NCD, the more your car insurance premium is discounted — and this can lead to substantial savings. But when you get into a car accident for which you are judged to bear responsibility, your NCD will drop by 30% to a minimum of 0% when you renew your car insurance plan.

How your NCD changes after an at-fault accident

| Starting NCD | NCD After At-Fault Claim |

|---|---|

| 50% | 20% |

| 40% | 10% |

| 30% | 0% |

| 20% | 0% |

| 10% | 0% |

| 0% | 0% |

Therefore, if you get into a car accident with a 50% NCD, your NCD will drop to 20% when you renew your insurance policy. Depending on how much you are paying for your car insurance, this could mean an extra cost of anywhere from around S$200 to around S$1,000. It will take you 3 years of driving without accidents (for which you are deemed responsible) to build your NCD back up to where it was, and in the meantime, you will be paying hundreds more dollars each year on your premium than you would have otherwise. As you can see, suffering a hit to your NCD has a very real cost.

To prevent this from happening, many insurers offer the option to add a NCD Protector feature to your car insurance plan if you’re willing to pay a little extra. This feature, which typically costs about an additional 10% on your premium, will ensure that your NCD does not drop even if you do get into an at-fault accident (though many policies stipulate that the NCD Protector will only protect your NCD for one claim per year).

Effect of Having a Recent Claims History

Another way a car accident can have a long-term impact on your car insurance premium is in how insurers calculate your car insurance premium. When you fill out an application form for a car insurance plan, insurance companies ask if you have any recent claims history. How you answer this question contributes to their determination of how much of a risk is involved in providing you and your car with coverage.

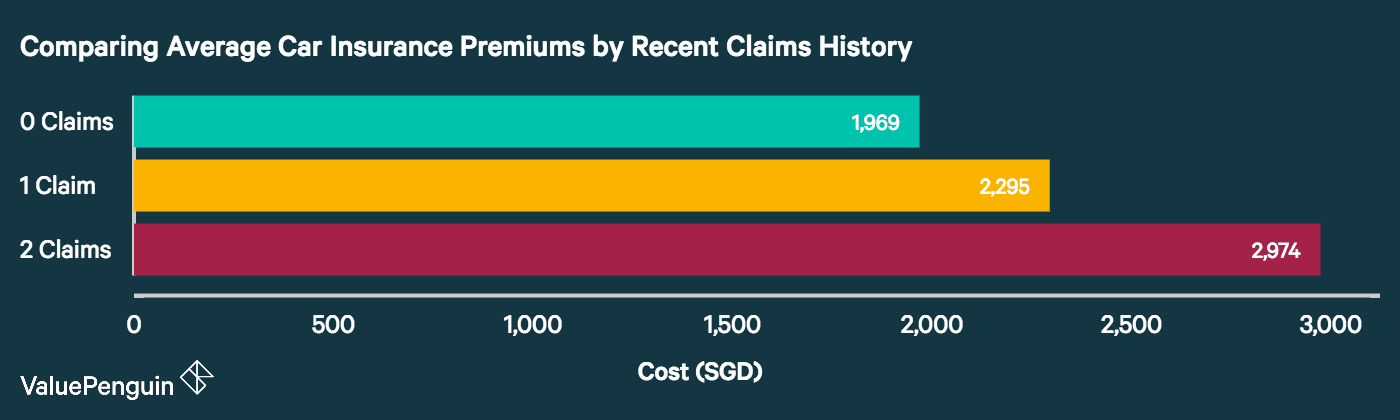

To see how different answers to this question might affect premium rates, we collected quotes from a selection of major Singapore insurers for a 2017 Toyota Corolla Altis, seeing how quotes changed for driver profiles that had 0 claims, 1 claim and 2 claims in the past 3 years. We held all other variables constant in order to ensure comparability. Our quotes and calculations all assume a 0% NCD to see how premiums change independently of any change in NCD.

We found that, on average, premiums increase by about 17% if you’ve submitted 1 claim in the last 3 years as opposed to no claims, rising from about S$2,000 to about S$2,300. If you’ve submitted 2 claims in the past 3 years, your insurer will charge you an average of approximately S$3,000, 51% more on your premium than if you had zero claims. And because insurers require you to provide claims history data for 3 years before the present date, this means that you stand to pay more on your premium for 3 whole years after your car accident. Note that building your NCD by 10% each year by maintaining a clean driving record will help to bring your premiums gradually back down again over the course of those 3 years.

Also, you should keep in mind that some insurers may refuse to offer you a quote online if you have any recent claims history and ask that you contact them in person or over the phone, while others may ask you to go into more detail. For example, they may ask you whether you were considered at-fault in a prior accident, or how much money your prior claims were filed for.

Parting Thoughts

Our study makes clear that if you get into a car accident, you’ll have to pay for much more than a hospital bill and car repairs, even if you have a comprehensive plan. Having an accident could potentially increase the cost of your car insurance for several years. For less confident drivers, it may be worth purchasing a NCD Protector to help mitigate this risk.

The article 2 Hidden Costs of Getting in a Car Accident in Singapore originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

- Average Price of Car Insurance 2017

- Best Car Loans 2017

- Probability of Getting in a Car Accident in Singapore

Source: ValuePen