It’s no secret that cars in Singapore are massively expensive: import taxes, COEs and registration fees can easily add up to S$50,000 or more, effectively doubling the price of a car. Given this, buying a car in Singapore is extremely difficult for an average Singporean consumer, especially without the help of vehicle financing.

When taking out a car loan, however, there are two primary options which every consumer will need to consider: 1) work with a bank that will loan you the money or 2) Receive a loan through the auto dealer that is selling the vehicle. But which one represents truly more economic deal? In this article, we breakdown the pros and cons of each approach, and highlight some other things to look out for during the process. Ultimately, the interest rate charged is the most important factor – but there are a number of other considerations to have in mind. Let’s get started.

Most Popular Cars in Singapore

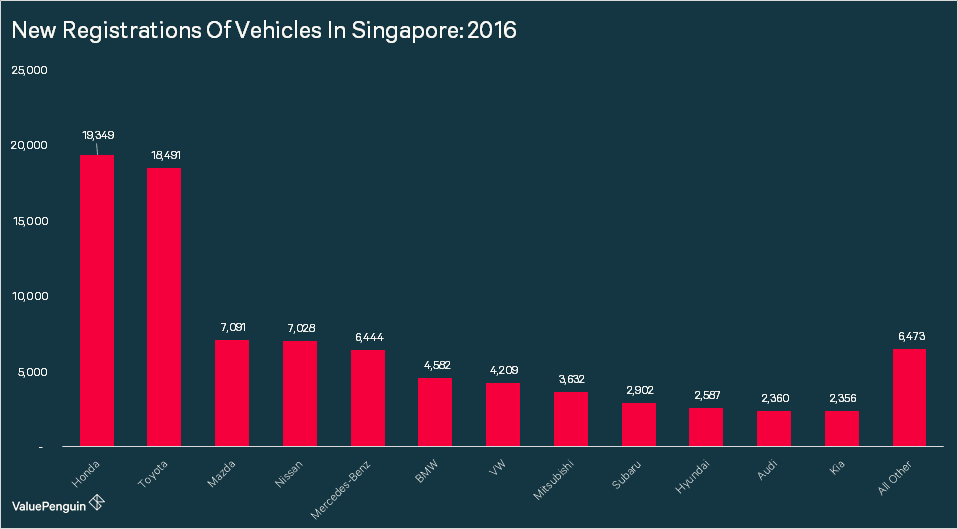

To put this discussion into context, let’s first explore where Singapore residents are getting their vehicles. This will allow us to create an accurate comparison of the average car loan rates through banks and the type of financing available through these popular dealerships. A great metric to track vehicles sales is by looking at the new vehicle registrations recorded by the Land Transport Authority in their 2016 Annual Vehicle Statistics report, featured in our chart below.

From this report, it is clear that Honda and Toyota are the two biggest names within the Singapore auto market. In 2016, these two companies accounted for a staggering 43.24% of new vehicle registrations on the island. Mazda, Nissan and Mercedes-Benz round out the top five, accounting for just 8.10%, 8.03% and 7.63% of new vehicle registrations, respectively.

What Vehicle Is a Good Baseline for our Comparison?

If we dig a bit deeper, we see that 10,109 of Honda registrations were within the SUV class. The majority of these purchases are likely the popular Honda Vezel – a two door vehicle branded as Honda’s “Urban SUV”. A quick web search shows that a Honda Vezel can be purchased at a number of Singapore auto dealerships for around S$100,000 with the cost of COE included. Without the COE, the vehicle can be purchased for around S$50,000. If you aren’t familiar with how the COE or vehicle depreciation works, you can read our blog on the topic.

So Where to Get Financing?

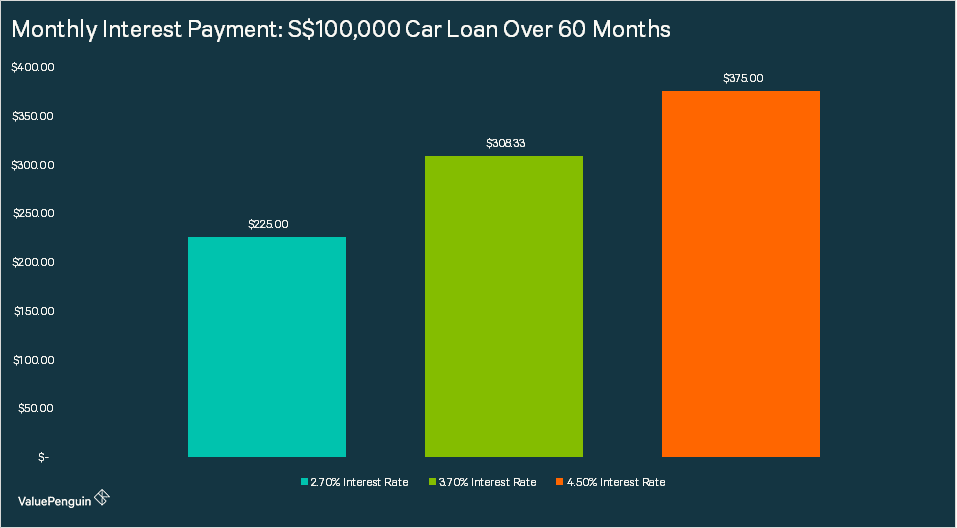

As we mentioned, the most important factor when finding the right loan is the interest rate and the tenure. We’ve done a lot of research, and found that some of the best car loans through banks are currently around 2.70%, with tenures between one and seven years. It is important to note that in Singapore, car loans charge interest on a flat rate rather than a rest rate. If you aren’t familiar with how this works, read our article that explains the difference between flat rate and rest rate.

Now it’s important to understand that every dealership is going to be a little bit different in what interest rate they will provide you, as the buyer, for a dealer-financed vehicle. While we have found some dealerships that “pass through” the bank rate to consumers as a means to sell more cars, we have also found some dealerships that charge one time fees or higher interest rates than banks as a means to generate additional revenue. In general, it’s almost always beneficial for the consumer to cut out as many middlemen as possible. In the case of a car loan, the middlemen would be the car dealer.

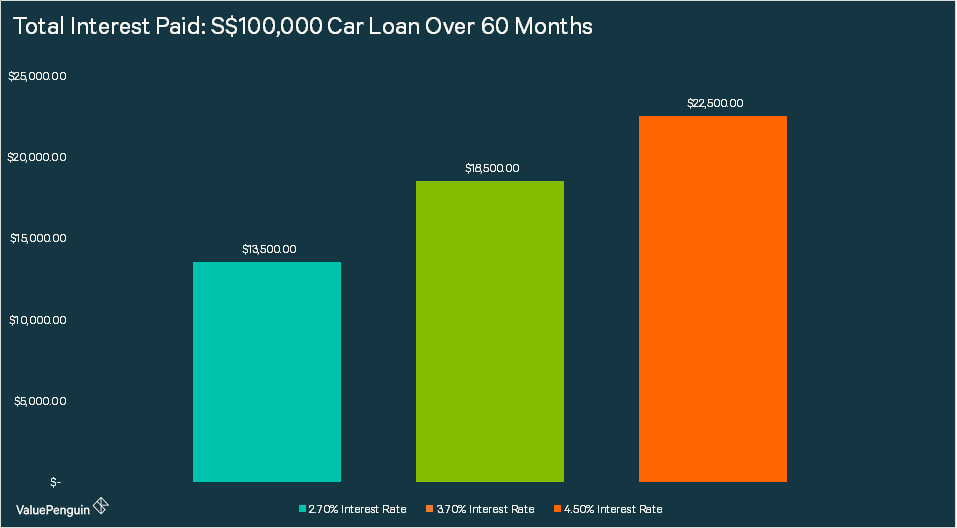

The chart below compares a 2.70% loan (the best found at banks) and a 3.70% and 4.50% loan (two hypothetical interest rates which could be found at dealerships) over a 60-month time frame. A 4.50% auto loan is quite high – but this will provide us with the high end of expected monthly payments.

In this example, the difference in monthly payments between the 4.50% loan and the 2.70% loan is just S$150. While this may look like a small difference, banks and dealerships make their money on the interest paid over the life of the loan – not the monthly payment. Over 60-months, this difference can add up substantially.

If we compare the total interest paid between the 4.5% loan and the 2.7% loan, it is S$4,844. Keep in mind this is a S$4,844 paid out over 5 years, which is roughly S$1,000 of difference per year.

The bottom line is that, like with many financial decision, the interest rate charged should be the biggest determining factor when deciding between bank and dealer financing.

What To Look Out For

Auto dealerships are known for not always providing straight-forward answers when it comes to the cost of a vehicle, and the vehicle’s financing. Here are a couple of things to look out for if you are considering using dealer financing:

- Low monthly payment sales pitches. Dealers will sometimes offer extremely low monthly rates as an incentive to make a sale. The downside for consumers is that these low monthly rates generally come with longer loan terms. Remember – financing companies make their money on the total interest payments, not the monthly payment amount.

- Charges or fees for paying off the loan early. This may come as a surprise, but many dealerships (and even banks) will charge you for paying off a loan early. This is done to help make sure they receive the interest payments they were expecting from the loan. As with any financial decision, reading the fine print is critical.

One More Thing To Consider…

Now, before you go out and apply for a loan it is important to keep in mind some new car loan regulations which have been updated by the Monetary Authority of Singapore. These rules, updated in May 2016, restrict how much consumers can borrow towards a vehicle. The table below shows the maximum Loan-To-Value (LTV) permitted based on the vehicle’s worth.

| Open Market Value of Vehicle | Maximum Loan-To-Value | Maximum Loan Tenure |

|---|---|---|

| Less Than or Equal to S$20,000 | 70% | 7 years |

| More than S$20,000 | 60% | 7 years |

In simplest terms, these regulations mean that a 40% down payment is required for vehicles with an OMV above S$20,000, while just a 30% down payment is required on vehicles with an OMV below S$20,000.

Final Thoughts

Whether you go with bank or deal financing, the interest rate charged and the features of the loan are most important. Spend some time shopping around and running the numbers before making your decision. You will be happy you did. At Value Penguin, we will be with you at every step of your car buying experience.

The article Car Loan Analysis: Should you get financing from a bank or an auto dealer? originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

- 4 Tips on Buying a Car in Singapore

- Overview of Singapore’s Lending Environment – 2017

- Best Credit Cards with Promotions 2017

Source: ValuePen