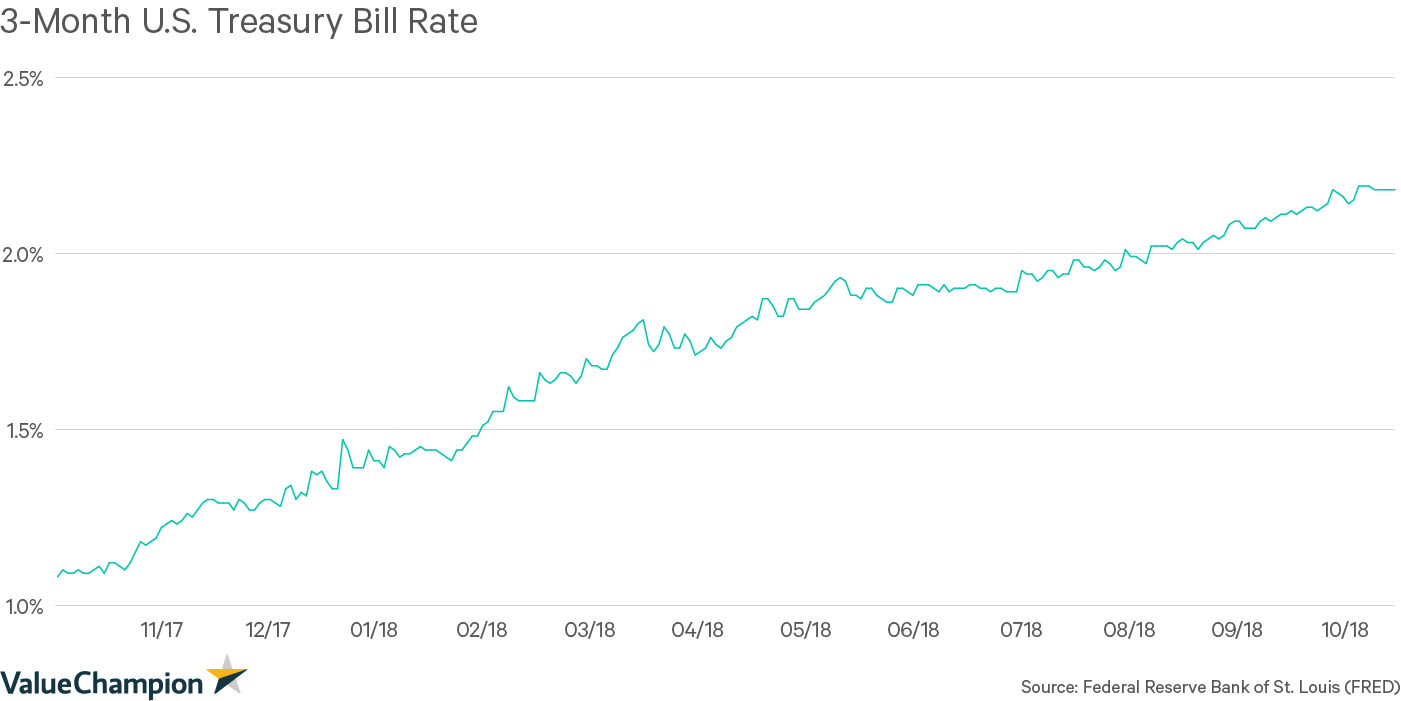

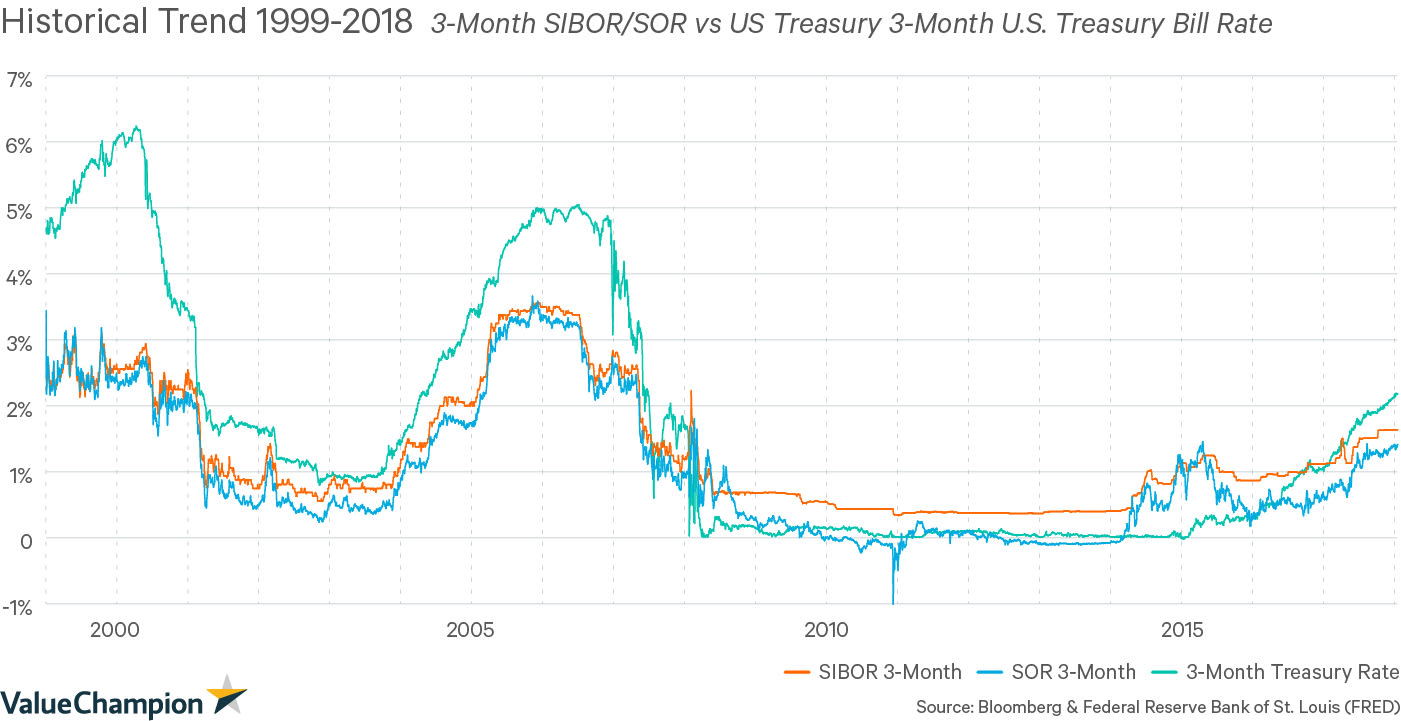

If you are familiar with trends in international banking and finance, you already know that changes in Singapore’s interest rates (SIBOR and SOR) are typically correlated to those of interest rates in the United States. Given the United States Federal Reserve has increased its target interest rate to 2.25%, Singaporeans should expect to see SIBOR and SOR rates increase in the coming weeks. But what exactly does this mean for individuals in Singapore?

Why Does the Rate Hike Matter to You?

For most Singaporeans, rising interest rates shouldn’t cause too much concern. However, higher rates mean that the cost of borrowing will increase, which impacts nearly all individuals, whether they are borrowers or not.

Homeowners & Prospective Homeowners

Homeowners are perhaps the most likely to feel the impact of rising interest rates. This is because mortgage interest rates change more frequently than other loans, and even change during an existing loan’s tenure. As a result of rising interest rates, homeowners will face higher mortgage payments. For example, if your annual interest rate rose from 2% to 2.5% you could expect to the cost of your monthly home loan payments to increase by 5% to 6%. Specifically, home loans with floating interest rates may see an almost immediate change in their monthly payment. This is because floating rates are typically tied directly to SIBOR or SOR rates. Individuals with mortgages with fixed interest rates may be shielded from rising interest rates in the short-term, but will likely face higher interest rates at the end of their loan’s lock-in period or if they hope to refinance their loan.

We strongly recommend that prospective homeowners compare rates before applying for any financial product; however, it is especially important to compare home loan rates, as these tend to change the most frequently. For prospective mortgage borrowers, it is important to understand the difference between fixed and floating rates. This is especially true when interest rates are rising. For example, it is generally advantageous to take out a fixed rate home loan compared to a floating rate loan when interest rates are on the rise. This is because a fixed rate loan protects borrowers from further increases of interest rates, despite their somewhat higher rate in the short term.

Other Borrowers

In addition to home loans, the interest rates for personal loans and credit cards are also likely to increase. For this reason, we strongly recommend that borrowers prioritise repaying their debts that are accruing a significant amount debt the fastest. These tend to be the types of debt with the highest interest rates, such as credit cards which charge about 20% to 30% on unpaid balances.

What About Individuals Without Debt?

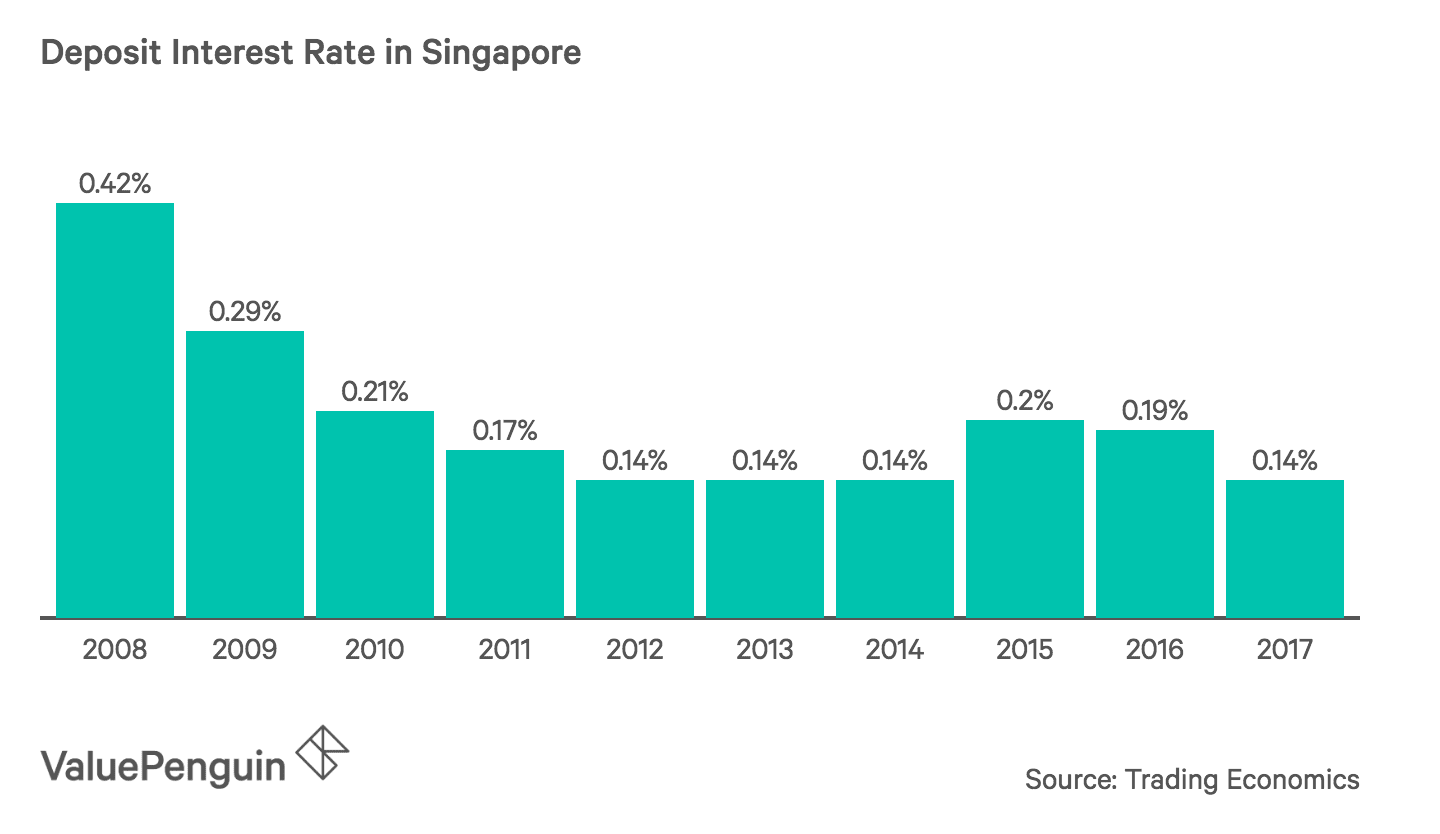

Individuals that are saving more than they are borrowing will likely benefit from rising interest rates. For example, as interest rates rise, individuals with savings in deposit accounts, such as certificates of deposit (CD) or savings accounts will earn more interest from their savings. The rates from these accounts have been very low in the past decade, but are poised to provide Singaporeans with better rates as interest rates rise generally. Other safer investment such as bonds also tend to perform better following rate hikes.

The impact of rising interest rates for more higher risk investments, such as stocks, is typically less positive. This is because, in general, market valuations tend to eventually decrease following interest rate hikes as consumer spending tends to dampen and businesses are more constrained by the rising cost of debt. Therefore, investors should proceed with caution. Still, it is important to realise that the reason the U.S. Federal Reserve (Fed) felt comfortable raising interest rates was due to strong economic indicators in the United States, which are typically a good sign for investors globally.

What Does This Mean for Small Businesses

Similarly, rising interest rates should not cause local SMEs to panic, but are worth monitoring as they will increase the cost of borrowing for nearly all businesses. Borrowing costs will likely increase because interest rates will rise for many business loans. Additionally, rising interest rates in the United States may cause the U.S. dollar to appreciate in comparison to the Singapore dollar. This would make it more expensive for small businesses that rely on goods from the U.S.

Key Takeaways: Be Cautious, But Don’t Panic

As interest rates rise in the United States, it is reasonable to expect that interest rates in Singapore will follow the same trend. This raise the cost of borrowing for both individuals and businesses and may dampen returns for the average investor. On the other hand, those that are able to save more than they borrow are likely to benefit as deposit rates increase. Because rising rates often change the landscape of financial product offerings, we recommend that individuals check rates frequently before applying for anything from a new credit card to a home loan, in order to ensure that you get the most affordable deal.

Do you have an interesting story about how you or your business has handled a previous rate hike? We’d love to hear more about your experience. Please feel free to reach out to us at [email protected].

The article What Do Rising Interest Rates in the U.S. Mean for Singaporeans? originally appeared on ValueChampion.

ValueChampion helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValueChampion:

Source: VP