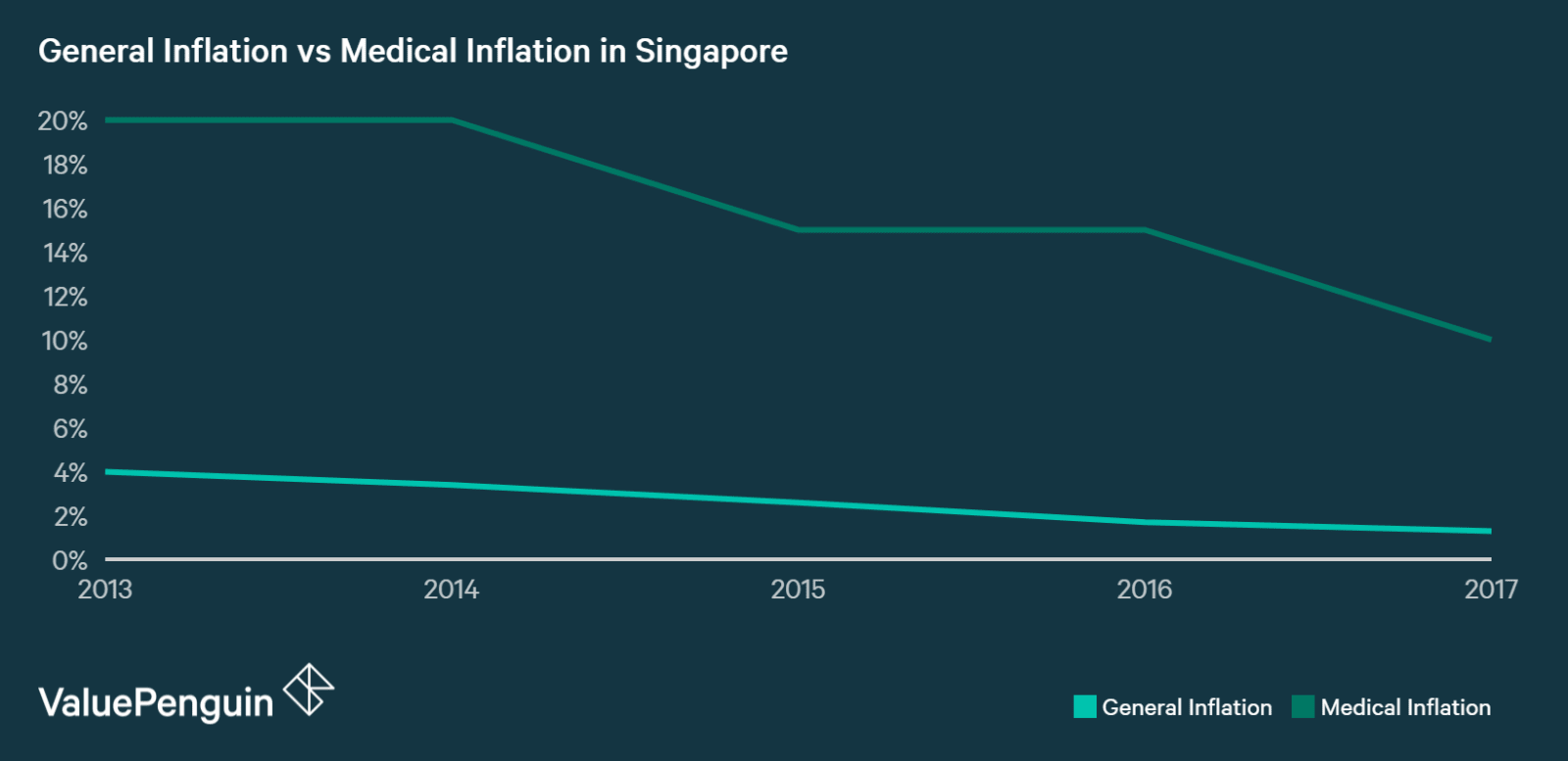

Singapore has been recording a high medical inflation rate for quite some time now. In fact, the country’s medical inflation rate, at 10 percent in 2017, is one of the highest such rates in Asia and has exceeded the country’s general consumer price inflation by many folds. Furthermore, factors like aging population and growing incidence of chronic illnesses are expected to make medical costs in Singapore even more prohibitive in the future. For example, an Angioplasty bill at the National Heart Centre costing S$25,226 in February 2017 is expected to rise to S$102,053 in ten years, according to AON. Given this scenario, how can consumers in Singapore best protect themselves from facing a potential healthcare expenditure shock?

Public vs Private Medical Insurance

Singapore’s already high medical inflation is expected to continue to rise even higher in the future, causing further consternation for its residents. Medical insurance, especially private insurance, is no longer just considered ‘good to have.’ In fact, it might be the most effective option left now for the consumer who wants comprehensive coverage and benefits.

From a public insurance perspective, the Singapore Government’s medical insurance strategy typically relies on the “three M’s”- Medisave, Medishield, and Medifund, with the first two being the most important. While Medisave covers routine expenses, Medishield covers the large expenses that one normally follows hospitalization. However, for all their benefits, public insurance does have its own limitations—Medishield does not cover certain conditions or procedures like ambulance fees, maternity charges or dental work, generally tends to have lower maximum payout level than private insurance and also doesn’t cover foreigners, which comprise about 30% of the population . Also, it only covers payments at Public Hospital B2 and C2 wards.

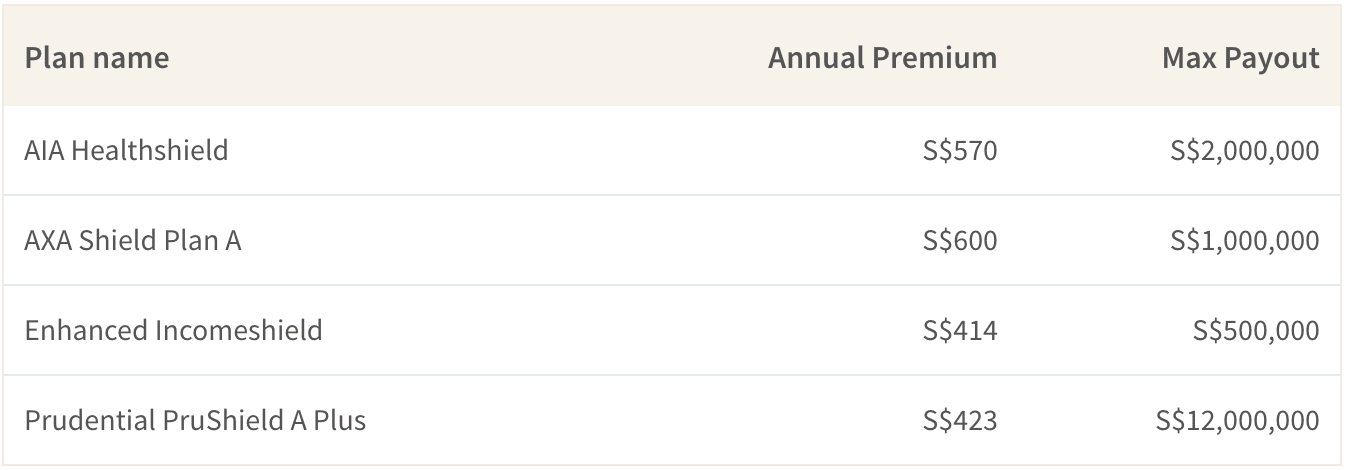

For a more comprehensive protection including coverage for more conditions and procedures, a higher coverage limit, better hospital accommodation, shorter waiting time for life threatening conditions, one can opt for a private medical insurance, which 60% of Singaporeans actually purchase. Singaporeans already covered by Medishield can opt for an integrated shield plan, which provides benefits of additional private insurance over the existing Medishield benefits. According to the Ministry of Health, the following insurers provide “Plan A” (which provides access to A/B1 class wards in hospitals) integrated shield plans on top of Medishield.

When choosing a health insurance policy, one should prioritize a few main factors, which we list below. By following a step by step comparison process, one can select the right policy and beat the challenge of the growing medical inflation rates.

- Covers the facilities, features and benefits that one precisely needs

- Has adequate payout/coverage for one’s needs (one should ideally review this every 3 to 4 years)

- Has an easy claims process as well as minimum limitations at the time of claims

Other Options for Consumers Who Can’t Afford Medical Insurance

While getting a medical insurance can be the most cost-effective way of mitigating potential risks related to high medical cost, those who may not readily afford it still have other options to reduce their medical bills.

Negotiate with Care Provider

First, you should try to negotiate with your hospital. Most hospitals are incentivised to do their best to accommodate the patient’s financial situation and maximise the chance of full payment over the long term: since the medical service has already been rendered, hospitals just want to make sure they collect as much of the bill as possible. Therefore, you can often negotiate a few terms. For example, if you make an initial lump sum payment immediately, you may be able to negotiate a discount for the balance of payment. Otherwise, you can also ask to divide your payment into smaller, more easily manageable for interest-free instalments that you can pay down over a longer period of time.

Earn Rebates to Offset Your Bill Slightly

Besides negotiating with the hospital, paying your bill with a good cash back card can also reduce your bill by 3-5% through earning cash rebates on your expenses. For example, POSB Everyday Card provides 3% rebate on your local medical spend at hospitals, medical and dental clinics in Singapore. To qualify for this benefit, you have to spend S$500 in a calendar month on the card, which should be relatively easy for paying medical bills.

Borrowing as a Last Resort

For bills that are too large to be managed effectively by the methods above, getting a bank personal loan can be a valid last resort. While they can still become a meaningfully burdensome debt at 8-10% effective interest rates, these loans are much more affordable than a typical loan from a loan shark or a moneylender. Not only that, by dividing up your payment into regular monthly instalments over several years, it can help you pay your medical upfront and avoid a medical bill induced bankruptcy and ruining your credit score. Still, if you think you can reliably repay the loan within 6-12 months, we advise paying the whole bill with a credit card, and then transferring your balance to a balance transfer loan, whose upfront processing fee combined with interest-free repayment period can be much cheaper than personal loans.

The article Singapore’s High Medical Inflation – How Can Consumers Manage Their Medical Bills? originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

- Best Cashback Credit Cards 2018

- Best Personal Loans in Singapore 2018

- Best Credit Cards in Singapore 2018

Source: VP