")

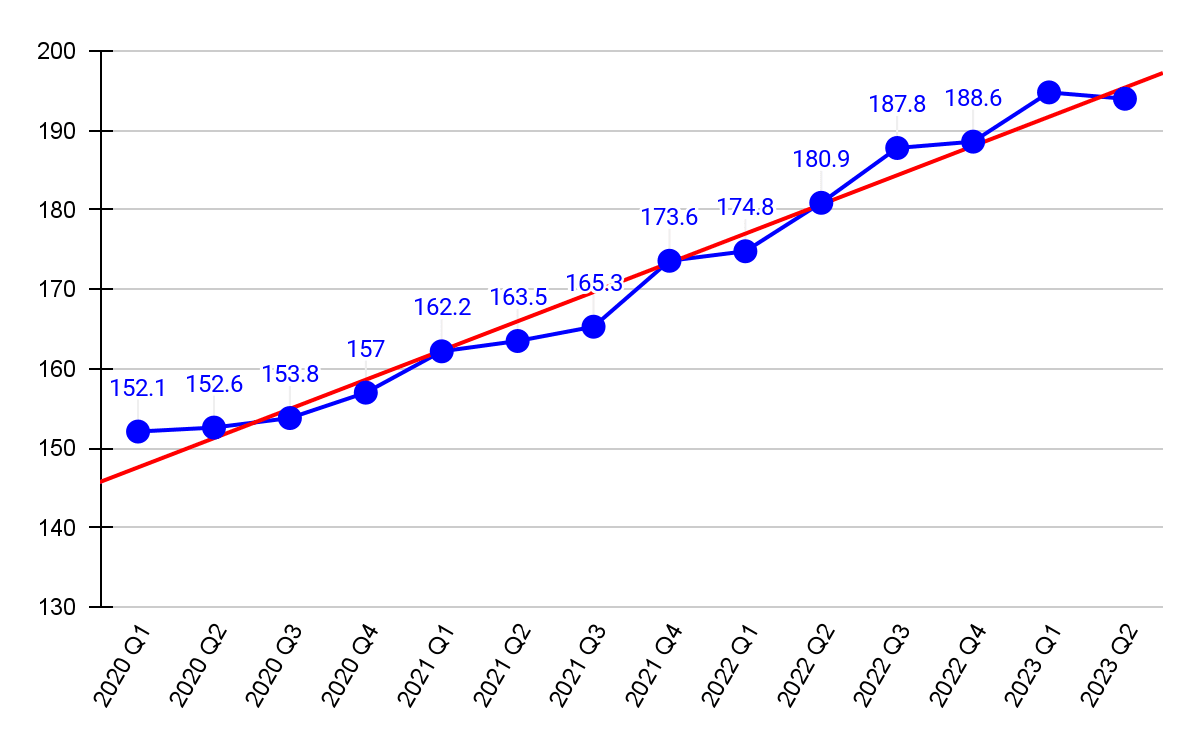

The recent Urban Redevelopment Authority (URA) flash estimates have revealed the first decline in Singapore private home property prices by 0.4% since the first quarter of 2020. Considering the prior quarter had witnessed a 3.3% gain, this sudden price dip has drawn lots of attention, especially from those looking for the right time to buy a private property in Singapore.

Singapore Private Home Property Price Index 2020 to 2023 2nd Quarter

Find the Cheapest Home Loans in Singapore

Why a Sudden Fall In Private Home Prices in Singapore

The decline in prices did not surprise market watchers since several rounds of cooling measures and fluctuating economic factors have been shaking up the property scene lately.

The multiple rounds of Fed hikes have pushed Singapore mortgage loans’ interest rates to an all-time high. Homeownership in Singapore has become increasingly expensive. With the economy still struggling to get back on track, many potential home buyers are taking a wait-and-see approach instead of making hasty purchases. With fewer eager buyers, sellers’ negotiating power naturally took a hit.

Another subtle factor is the promise of nearly 100,000 new private and public homes that are being rolled out between 2023 and 2025. Reportedly, private housing supply is around 9,250 units this year, the highest number in a decade. By ramping up the housing supply and homeownership opportunities in Singapore, the prices seem to soften in tandem.

The additional round of Additional Buyer’s Stamp Duty (ABSD) adjustment on 26 April 2023 was another clear sign that the government is making a resolute effort to keep the local property market sustainable. The rates are adjusted at all levels, but the significant increase of ABSD for foreign buyers from 35% to 65% points to the attempt to keep overseas property investors at arm’s length so that Singapore private property prices can remain affordable for locals.

What’s Next – Will Prices Continue To Fall?

Even though the number of private condos purchased by foreign buyers has dropped to 71 units in May from 113 units in April, it is still hard to say if cooling measures in Singapore, such as the new ABSD rates, can truly play its part in keeping private home prices down for the rest of the year. The sudden drop in sales volume could be just a knee-jerk reaction. Singapore is still a safe haven for foreign investors in the long run. Despite the high property prices, housing in other cities like Shanghai is still much higher in comparison.

In Singapore, HDB upgraders make up a large portion of private property buyers. With the HDB Resale Price Index showing no sign of slowing down, the potential for this pool of buyers to fetch higher proceeds from their HDB flat sale to fund their private home purchases remain relatively high for the year. However, there are only 15,748 units of flats reaching their Minimum Occupancy Period (MOP) in 2023 as opposed to 31,325 in 2022. This also points to the fact that there is a much smaller pool of HDB upgraders to fuel the price growth in the private home sector for 2023.

However, it is safe to say that the Singapore property market has been resilient for many decades. Coupling that with the low unemployment rate and rising median monthly household income, it is still possible to expect growth in private home prices in Singapore in the near future.

Related: A Step-by-Step Guide to Property Investing in Singapore

How Much Mortgage Loans You Need To Buy Your First Private Property in Singapore

If you are ready to purchase your first private property, the first step is to assess the affordability based on a thorough calculation of your cash-on-hand, the amount of Central Provident Fund (CPF) available in your Ordinary Account (OA), any existing loans that may affect your Total Debt Servicing Ratio (TDSR) and your monthly income to support the home loan repayment.

Suppose you are a Singaporean buying your first property in Singapore, which is a S$1 million condo. Your financial calculation should include 25% in the down payment, in which 5% must be paid in cash, and the remaining 20% can be funded by cash or CPF OA. The down payment breakdown will look something like this:

| Down payment for Private Property Purchase | Amount |

|---|---|

| Option To Purchase (5%) | S50,000 (cash) |

| Outstanding downpayment (20%) | S$200,000 (cash or CPF-OA) |

| Buyer’s Stamp Duty (BSD) | S$24,600 (cash or CPF-OA) |

| Total down payment | S$274,600 |

Next, you must assess if your TDSR and monthly income qualify you for the mortgage loan to cover the remaining 75% of the purchase price. Use the ValueChampion Home Calculator to get an idea of the monthly repayment. The result will determine if your monthly disposable income is enough to pay for the monthly home loan repayment.

Do note that the maximum loan tenure is 35 years for private properties in Singapore. The longer you stretch your tenure, the more interest you will pay; however, shorter tenure will mean that your monthly repayment will be much higher.

Finally, you must ensure your new home loan is within your TDSR. This framework implemented by the Monetary Authority of Singapore (MAS) allows you to utilise only up to 55% of your gross monthly income to service your total debt obligations.

So, if your current salary is S$8,000 monthly, your maximum monthly debt repayment limit is S$4,400 (S$8,000 x 55%). If you are taking out a home loan on top of any existing loans, you must ensure that your monthly loan repayments will not exceed S$4,400.

Related: How to Handle Mortgage Stress

Conclusion

If you are ready to pamper yourself with that dream home, thoroughly research the market for the best mortgage loan package with the lowest interest rates. This will not only make your cost of home ownership reasonable but also ensure it remains affordable should the property market fluctuates due to unexpected economic changes.

Refer to our Best Home Mortgage Loans in Singapore 2023 for top deals in the market.

Read More:

Cover image source: Unsplash

The article originally appeared on ValueChampion.

•

ValueChampion helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

•

More From ValueChampion:

•

Best Cheap Mortgage Insurance in Singapore 2023

Real Estate Investment: How to Build a Solid Property Portfolio

Pros and Cons of Paying Off Your Mortgage Early