")

The SRS is a voluntary savings scheme on top of your involuntary savings scheme, that is, your Central Provident Fund (CPF).

Parking your money in your CPF gives you the basic retirement income you need, but the SRS does more than that. You can contribute and channel your funds into SRS, and these SRS funds can be used for you to purchase investments so that you can take growing your wealth to the next level.

The best part is, contributions to SRS are eligible for tax relief and you will be able to make investment returns tax-free.

So, how do you get started? Let’s get right into it.

How Does SRS Work?

Opening An SRS Account

Diving into the technicals, the SRS account isn’t automatically opened for every Singaporean. To open an account, you would need to fulfil the following eligibility criteria.

You must be a:

- Singapore Citizen, Singapore Permanent Resident (SPR) or foreigner who derive any form of income may make SRS contributions in the current year, and be;

- At least 18 years of age;

- Not an undischarged bankrupt;

- Not having a mental disorder; and

- Capable of managing yourself and your affairs.

If you fulfil all the eligibility criteria as above, great! You’re now one step closer to maximising the benefits to be reaped from having and contributing to an SRS account.

You can open your SRS account with any of the 3 bank operators (DBS, OCBC and UOB). Apply via the banks operators’ online banking sites or mobile apps. Some of these banks also provide promotions and rewards for applying for SRS with them, so be sure to watch out for those limited promotions as well!

Making Contributions To Your SRS

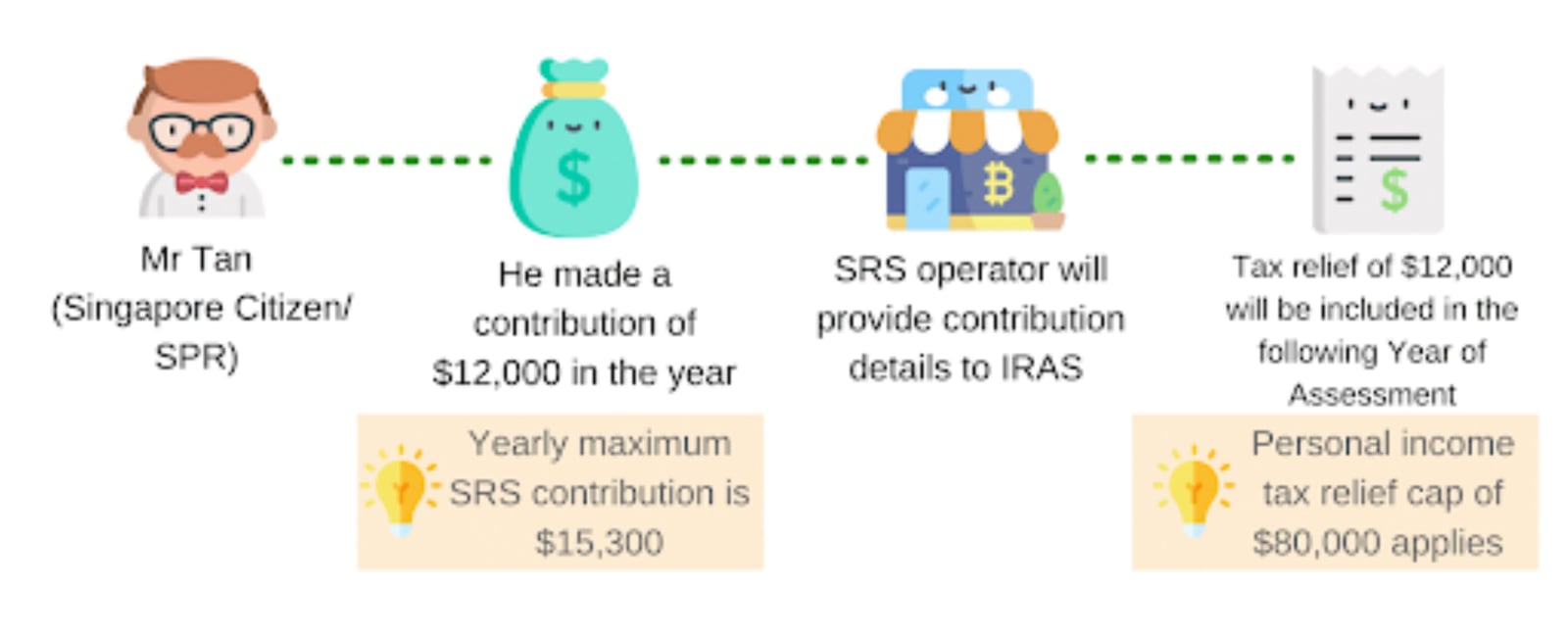

To use your SRS funds for purchase of other investment products, you will first need to make contributions to your SRS account. The full actual amount which you contribute in a year would also qualify for tax relief in the following Year Of Assessment.

Below is an example, provided by the Inland Revenue Authority of Singapore (IRAS).

Some important points to note would be that all SRS contributions have to be made by 31 December of the year, or any cut-off date as per your SRS operator (DBS, OCBC, UOB). This is to ensure that you would be eligible for the tax relief in the following year.

For Singaporeans and PRs, there is a cap on the yearly maximum SRS contribution – S$15,300. As for foreigners, the cap is higher, at S$35,700.

You can make SRS contributions anytime and at any frequency throughout the year, as long as it is before the cut-off date. Additionally, your employer can contribute on behalf of you as well. All SRS contributions will need to be in cash.

Can I Make Contributions To My SRS Forever?

You can continue to make contributions to your SRS account until you start making withdrawals from your account, at or after the statutory retirement age that was prevailing when you

- made your first SRS contribution; or

- on medical grounds.

Who Qualifies For SRS Tax Relief?

All SRS contributions allow individuals to qualify for tax relief, which is good news.

However, this is subject to a few conditions.

Firstly, ensure that you are a tax resident in the Year Of Assessment.

Another limitation of the SRS tax relief scheme is also that there is a personal income tax relief cap of S$80,000 and this applies to SRS contributions as well.

When you make contributions to your SRS, these funds are non-refundable. Hence, it is crucial that you do your calculations, and ensure that you are actually able to qualify for the SRS tax relief and reap the benefits from contributing to your SRS.

Apart from this limitation, most other SRS contributors should be able to benefit from the tax relief offered. However, you will not qualify for SRS tax relief if

Your SRS account is suspended as at

- 31 Dec of the year of contribution; or

- The amount of such contribution is withdrawn from your SRS account in the same year of contribution.

It may sound confusing, but rest assured that you will be able to qualify for SRS tax relief as long as you don’t make any withdrawals.

Withdrawals From SRS

Unlike your CPF, you can withdraw funds from your SRS account at any time, making them more flexible than the former.

However, the withdrawal amounts are subject to tax, and the prevailing tax rates would be determined based on the circumstances of your withdrawal. For a simpler understanding, you can refer to the below table for the types of withdrawals from SRS.

| Type Of Withdrawal | Amount Subject To Tax | 5% Penalty Fee? |

|---|---|---|

| Withdrawal on or after prescribed retirement age | 50% of withdrawal sum | No |

| Withdrawal on medical ground | 50% of withdrawal sum | No |

| Withdrawal in full due to terminal illness | 50% of withdrawal sum less an exempt amount of up to S$400k | No |

| In the event of bankruptcy | 100% of withdrawal sum | No |

| Early withdrawals before prescribed retirement age | 100% of withdrawal sum | Yes |

An important factor to note is that there is a 5% penalty fee imposed on any withdrawal made before the prescribed retirement age, reinforcing the CPF Board’s ideal of the SRS account as a retirement scheme.

What Can I Invest In Using SRS?

Now let’s move on to the interesting part. What can you invest in using your SRS funds? SRS gives individuals the freedom to invest in a wide plethora of investment products and instruments, helping you to boost your wealth and retirement sum.

Investment products approved by the SRS include the following:

- Stocks

- Bonds

- Exchange-Traded Funds (ETFs)

- Real Estate Investment Trust (REITs)

- Unit Trusts

- Fixed Deposits

- Regular Shares Savings (RSS)

- Insurance

- Singapore Government Securities (SGS)

- Robo-Advisors

No one wants to see their hard-earned money go to waste in investments that do not perform well. There are so many investment instruments which you could invest in, including the Singapore Savings Bond (SSB), or stocks and ETFs on online brokerages.

Investing in products like stocks which are prone to volatile market fluctuations may lend investors less stability, but also offer potentially handsome returns and rewards. On the other hand, safer investments such as fixed deposits and bonds may not give the aggressive investor the returns he or she was looking for.

As cash and investments purchased with SRS funds can only be withdrawn after the prescribed retirement age, we recommend that you choose to invest in a medium-to-long term investment product for optimal performance and results.

Regardless, since every investor has a different risk appetite and profile, it all boils down to your own preferences and financial lifestyle on which investment instruments you would like to invest in and which is the best for you.

How To Maximise Your SRS Account

With your hard-earned money being contributed to your SRS account, you wouldn’t want to let it go to waste and sit idle. To best maximise the funds in your SRS account, you should not let your deposits stay in your SRS account, as interest rates applied on your SRS funds follow the low default interest rate of 0.05%.

How best can you maximise the funds in your SRS account?

Firstly, ensure that you do invest your SRS monies into investment vehicles to help drive the growth of your portfolio and wealth. Since there are so many approved SRS investments, you can feel free to take your pick. Robo-advisors, such as Endowus and StashAway are approved and you can directly invest in a wide range of customised portfolios for you with your SRS funds on the robo-advisor platforms themselves.

For any funds left uninvested, it would be good not to let them sit idle as well, or else you would be better off contributing your funds to your CPF account, which earns a much higher rate of 4% per year.

You could consider parking the remaining uninvested funds in your SRS account into cash management accounts, which have potential returns of up to 2%, also far surpassing the default SRS rate of 0.05%. These cash management accounts offer high liquidity, and much lower risks compared to typical investment vehicles, and can be great options for those seeking security in their investments.

Is Investing Using SRS Ultimately Worth It?

Certainly, parking your funds in your SRS account can bring you benefits, and one of the biggest is surely your savings on your income tax. Every cent which you contribute to your SRS account is tax-deductible, and this can help you save a great deal of money, all whilst contributing to your nest egg during retirement.

Conclusion

In conclusion, the SRS is a government scheme that aims to help everyone in Singapore build their nest egg comfortably as the population ages. CPF may provide Singaporeans with a basic retirement income, but investing with SRS funds is a great alternative for you to enjoy tax relief. With so many choices of investment vehicles to choose from, your SRS funds can also be put to work to help you grow your wealth with a peace of mind.