As announced by Prime Minister Lee’s National Day Rally speech, the HDB Lease Buyback Scheme will be extended to all HDB flats. While it has generated a lot of hype since it gives Singaporean homeowners more flexibility around what they can do with their biggest asset, there is still a lot of discussion on whether one should participate in the scheme. Therefore, we wanted to crunch the numbers to actually assess whether consumers should be participating in the scheme to sell a portion of their HDB leases. And indeed, our analysis below shows that participating in the HDB Lease Buyback Scheme definitely seems like a financially savvy move, especially for those who want to stay at their current dwelling.

Estimating the Financial Benefits of HDB Lease Buyback

Simply put, HDB Lease Buyback Scheme allows HDB owners to sell the end portion of their HDB lease back to the government. Essentially, this measure allows elderly homeowners to generate some income using their their biggest financial asset (real estate) without needing to entirely sell their property and downsize to a smaller home. To assess whether this is a financially savvy move, let’s take an example of a 65-year old married couple living in a 4-room HDB flat. They purchased their home when they were 31 years old, and now they still have 65 years left on their lease. We estimate that participating in this scheme can net them a proceed of approximately S$400,000 in total, which we will breakdown step by step below.

The Property Value & Accelerated Depreciation

According to our research, a typical resale 4-room HDB flat costs about S$450,000. Since most home loans have maximum duration of 25-30 years, a family who has lived at their home for about 30 years should have fully paid off their mortgage and take full advantage of this value. According to the government’s website, the couple in our example could reasonably expect to sell the last 35 years of their lease to earn S$190,000.

Savvy readers may have noticed that this proceed is less than half of the property’s full value although 35 years represents more than half of the time remaining on its lease. This is because a HDB flat’s value depreciates in an accelerated manner, meaning that it loses more value each year in the beginning of the lease than at the end of the lease. For instance, if the couple actually tries to sell a home after 30 years, the buyer will only be able to live in the flat for 35 years. This means that the buyer will have an extremely difficult time selling the flat 20 years later, since there won’t be many buyers willing to purchase a flat with only 10 years left in its lease (since it’ll be worth nothing at the end of the lease). Because of this dynamic, HDB flats are more valuable in the beginning of its lease than at the end.

CPF Life Payouts & Cash Proceeds

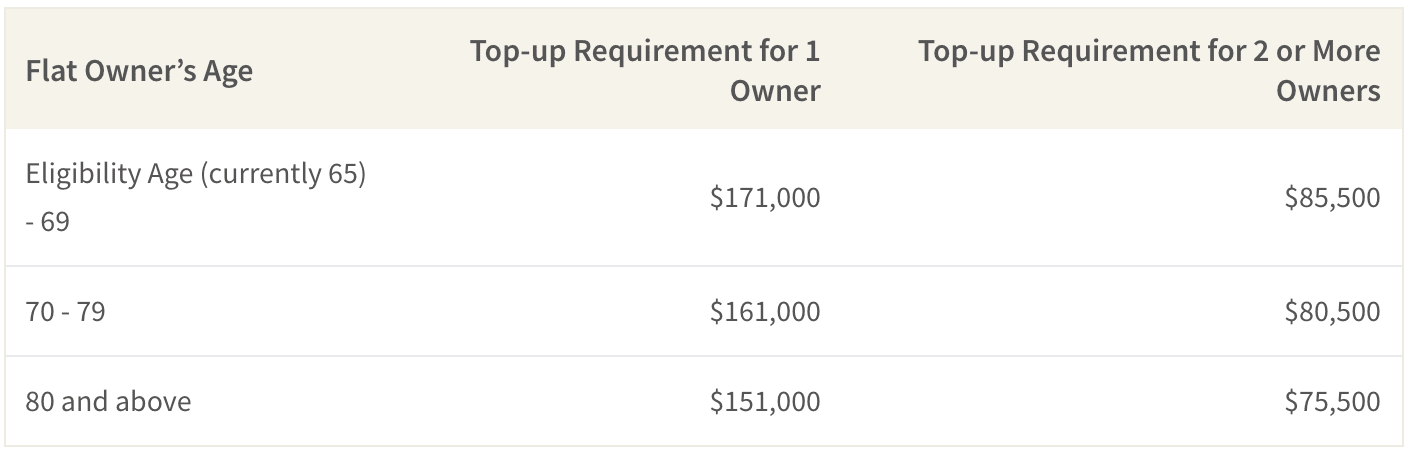

There’s another caveat when it comes to selling a portion of your lease back to HDB: instead of receiving the sales proceed in cash upfront, homeowners need to use the proceeds to top-up their CPF Retirement Accounts (RA) up to the amount shown in the table below. While this may sound like a bad thing to some people, it actually could result in a massive increase in payout. The CPF RA account can be used to purchase a CPF LIFE plan, which is one of the most effective ways of receiving a steady stream of income even compared to private life insurance plans.

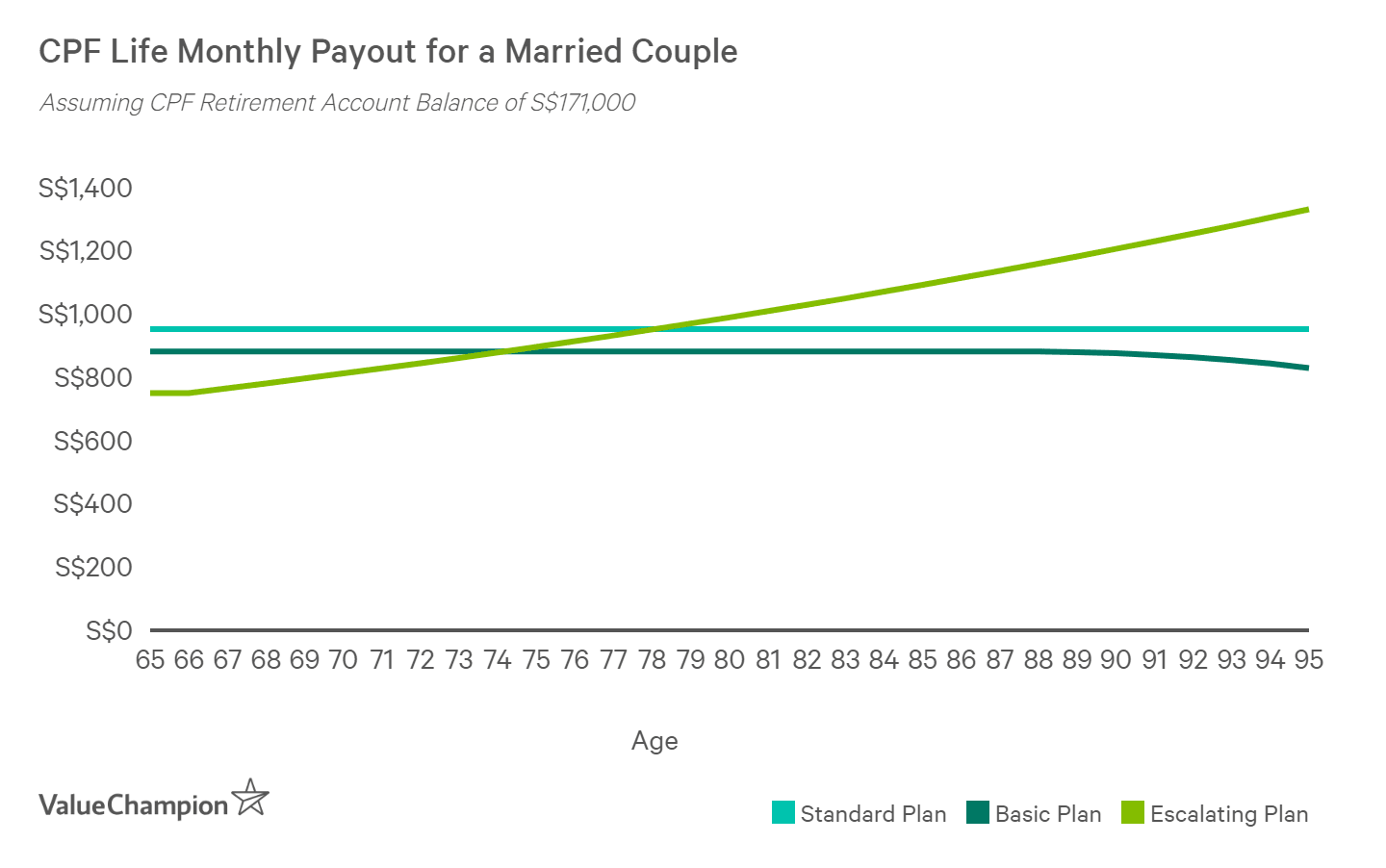

For example, let’s say that the couple had contributed about S$25,000 in their RA before the sale. Then, the couple can use the S$190,000 sales proceeds to top-up their RA to the legal requirement of S$171,000. Then, they can use the S$171,000 to purchase a CPF Life Plan to immediately earn a net yield of 7% every year (or approximately S$950 per month) from the age of 65 until they pass away, according to the CPF LIFE Payout Estimator. This is an extremely high payout rate, considering that it involves zero risk (government guarantees your payment); in comparisoninvesting in the stock market, which is much riskier, tends to yield about 10% per year. Given that the average life expectancy for people at the age of 65 is 84.1 for men and 87.5 for women, this couple stands to receive about S$250,000 from their S$171,000 of investment.

Additional Upfront Cash Payment

That’s not all. After topping-up their RA account to the legal requirement, they can also receive the remaining proceeds as cash (up to S$100,000) along with a Lease Buyback Scheme (LBS). In case of the couple in our example, they can receive S$44,000 upfront in cash after topping up their RA. On top of this, they stand to receive another S$10,000 since their property was a 4-room flat and their top-up amount was greater than S$60,000. This brings our total proceeds to about S$300,000.

Option to Rent Out a Room for Additional Income

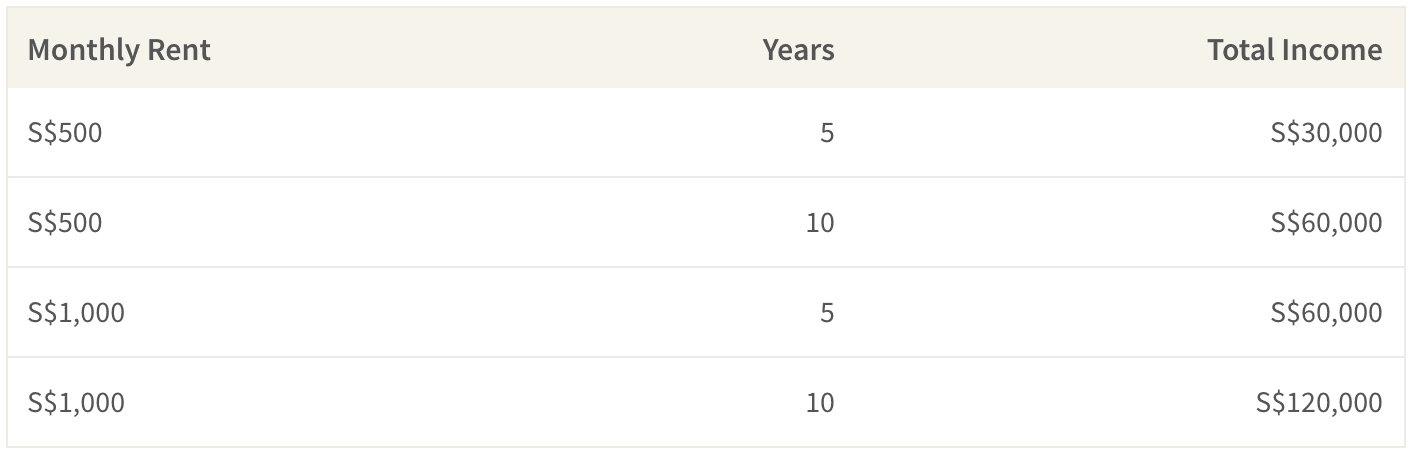

For those who are both willing and healthy enough, renting out the extra room can be another huge benefit of keeping their large HDB flat through the Lease Buyback Scheme instead of downsizing to a smaller flat. For example, a room in Singapore can easily fetch a price of at least S$500 to S$1,000 per month, according to various real estate listings websites. If you are able and willing to host an extra person at your abode for 5-10 years (i.e. while you are healthy), that could mean extra S$30,000 to S$120,000 of income. This wouldn’t be an option for those who sell their flat to move to a smaller one, since they won’t have the extra room to rent out.

How Do Alternatives Stack Up?

Certainly, there are alternative options for homeowners, such as inheriting the property to their children or selling the property to “right-size” to a smaller place. But how do they actually stack up against LBS in terms of financial payout?

First, inheriting it could be worthwhile if you think about it as a ways to save money on rent. For example, it’s very unclear whether your children will be able to fetch a price that’s better than S$190,000 that you can get today if they decide to sell your flat. Still, given that the average rent in Singapore is about S$2,000 for a 4-room HDB flat, they could save about S$840,000 in rent (S$2,000 x 12 months x 35 years) if they decide to live at your flat for free until the lease expires. However, that could be rather unrealistic it means they will have to wait another 20-30 years before they inherit the place.

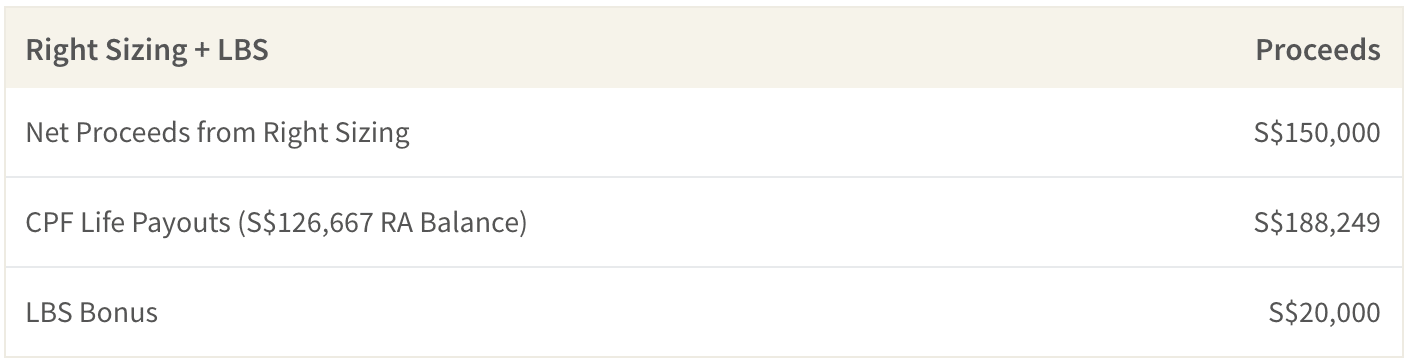

The other option of downsizing is viable option, especially for those who don’t want the extra hassle of renting out a room. For instance, they can immediately earn S$150,000 from selling a 4-room HDB for S$450,000 and buying a 3-room HDB for S$300,000. Not only that, they can use their new unit to participate in the Lease Buyback Scheme to earn S$126,667 which they can use to top-up their RA and get a CPF Life plan. In total, the total proceed could be about S$360,000, which is actually better than doing the Lease Buyback with your original flat but without renting.

Other Considerations

All in all, we believe that many homeowners should seriously consider participating in the Lease Buyback Scheme in one way or another. However, with all things in life, this decision also may depend on other factors like your age and health. For instance, the reason why LBS and CPF Life work really well in tandem is because the life expectancy has increased so much over the years. Therefore, it may not work so well financially for those who don’t live long enough to receive CPF Life payouts that exceed what they put in. Even still, even this risk is somewhat mitigated since CPF is supposed to transfer whatever is remaining in your account to your spouse or your children.

The article Is HDB Lease Buyback Really Worth Pursuing? originally appeared on ValueChampion.

ValueChampion helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValueChampion:

Source: VP