Crowdfunding is an intriguing opportunity for individual investors. If you are interested in this type of investment, it is helpful to research the various platforms in order to make a good choice. For the most part, you should be considering the same criteria that you would for any investment opportunity, including costs, returns and potential risks. In this article, we highlight the most important factors for differentiating between crowdfunding platforms as an investor.

Investment Type: Risks & Returns

Before you make a decision about a crowdfunding platform, you’ll need to explore the investment opportunities available from each site. Crowdfunding platforms in Singapore offer a range of investment opportunities including real estate investments, small business loans, equity investments, invoice financing and asset purchase agreements.

You should understand the risk and reward profile of each type of investment before committing your funds to a crowdfunding campaign.

Invoice financing and asset purchase agreements are typically the least risky investments, as they require that the borrower has completed work or has a specific use for the funds. Because of their low risk, these investments also offer lower returns than other opportunities. Small business loans are more risky, in the sense that they provide financing for general purpose work without a specific use. This means that business loans also offer investors slightly better interest rates, on average. Real estate investments vary greatly in risk, but tend to offer lower risk than equity investments, as they are based on tangible assets that can be sold in case of default. Equity investments offer the highest risk, and therefore highest potential returns, because they are based on the success of a company, and can result in high returns or the failure of the business.

High returns might be the reason that you became interested in crowdfunding in the first place. Small business loans tend to offer annualised returns of up to 25%. Invoice financing and asset purchase financing tend to offer annualised returns as high as 20%. Annualised real estate investment returns vary greatly depending on the specific type of investment. There is no ceiling to returns from equity investments, but they are also the most risky investments available from crowdfunding platforms because if the business fails, investors get nothing.

Performance Track Record

Some investors will naturally be cynical of the relatively nascent phenomena of crowdfunding. How can investors be comfortable lending through these platforms to businesses that were not eligible for more traditional forms of financing? First, investors can review or request more information from crowdfunding platforms, such as their average default rates. The best platforms offer default rates as low as 1.3 – 3.5%. These rates are comparable to those of commercial banks and should give investors confidence to invest. Other performance statistics to consider include percentage of on-time payments and total number and volume of deals completed. Not all platforms are open to disclosing their data, and it would be prudent to invest with platforms that provide statistics about their performance on their websites or through their customer service teams.

Fees

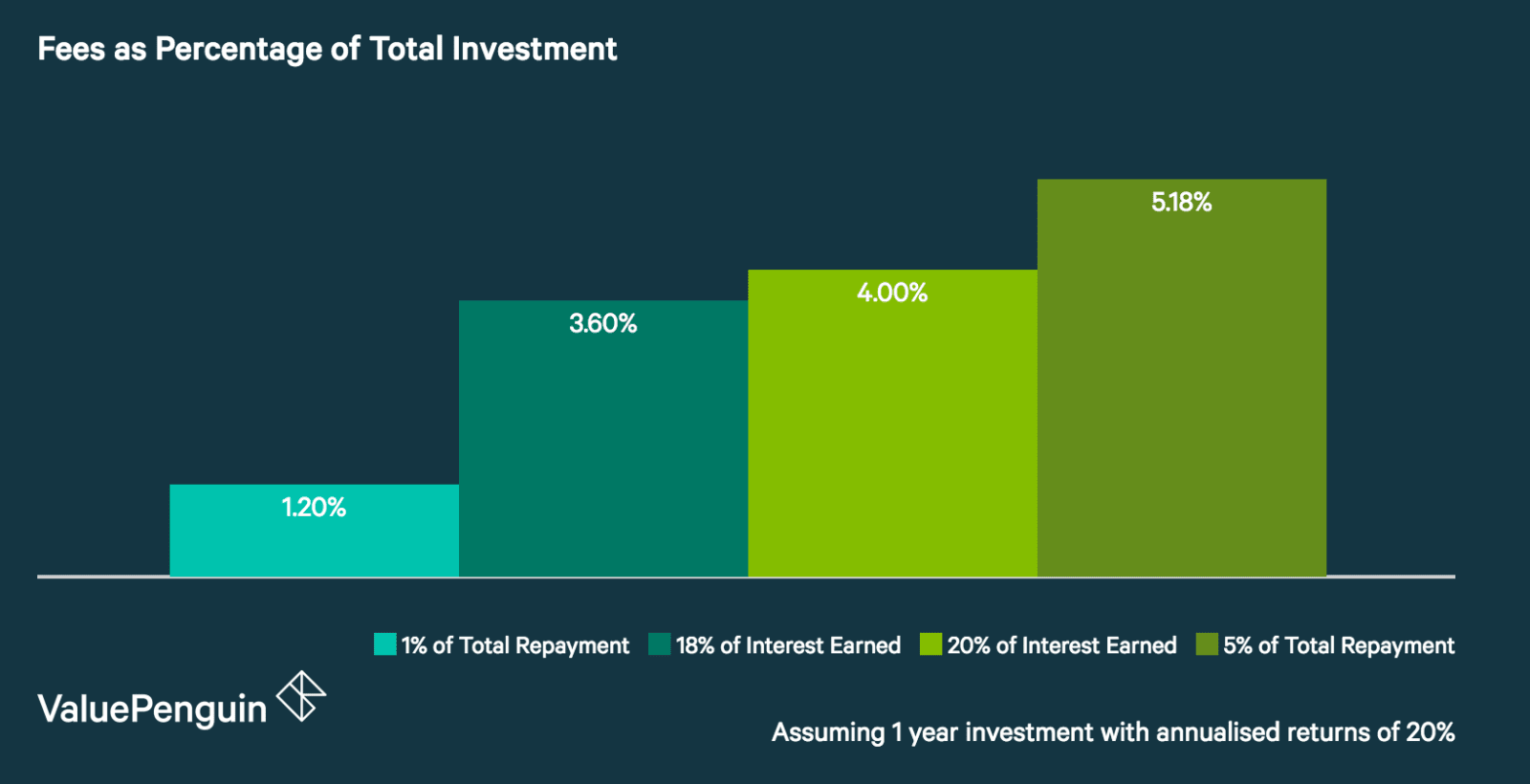

Similar to brokerage accounts, most crowdfunding platforms charge a service fee to investors. Some platforms charge very low fees or no fees at all. Others charge 1 – 8% on all repayments received or 18 – 20% of interest earned. Investors should have an understanding of the fees that they will be required to pay and how much these fees cost in relation to their expected returns. Since most of these investments last a few months to a year, minimising your fees per investment could actually add to a meaningful amount of savings. For example, assuming that a 1 year investment earns 20%, fees of 1% of total repayment will be the least expensive (1.2% of initial investment), followed by fees of 18% of interest earned (3.6%), 20% of interest earned (4.0%), and 5% of total repayment (5.18%).

Minimum Investment

Platforms have varying minimum investment requirements. Therefore, you may be forced to choose a platform based on the amount of cash that you have available to invest. Crowdfunding platforms that offer small business loans, invoice financing or asset purchase agreements generally require that individual investors commit at least S$100 – S$1,000 per campaign. Equity and real estate crowdfunding investment platforms tend to require more substantial contributions per investment opportunity, typically at least S$5,000. Additionally, the top equity and real estate crowdfunding platforms require that investors are accredited, meaning that they must have net personal assets of S$2 million, with their primary residence value accounting for no more than S$1 million, and an income of at least S$300,000.

The article 4 Factors to Consider When Choosing a Crowdfunding Platform originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

- Best P2P Crowdfunding Platforms for Investors 2018

- Best Online Brokerages in Singapore 2018

- Investacrowd Crowdfunding Platform – Review for Investors

Source: VP