Today, consumers in Singapore can earn a variety of “rewards points” where ever they go. Not only do many credit cards in Singapore already provide a lot of points already, now some mobile payment apps are also touting their own rewards in an effort to attract more users. However, consumers should be more careful before signing up for a new card or a payment app just because they were enticed by flashy marketing materials promising a lot of rewards points. Mainly, there are three precautions people should take before making a decision.

Not All Points Are Made Equal

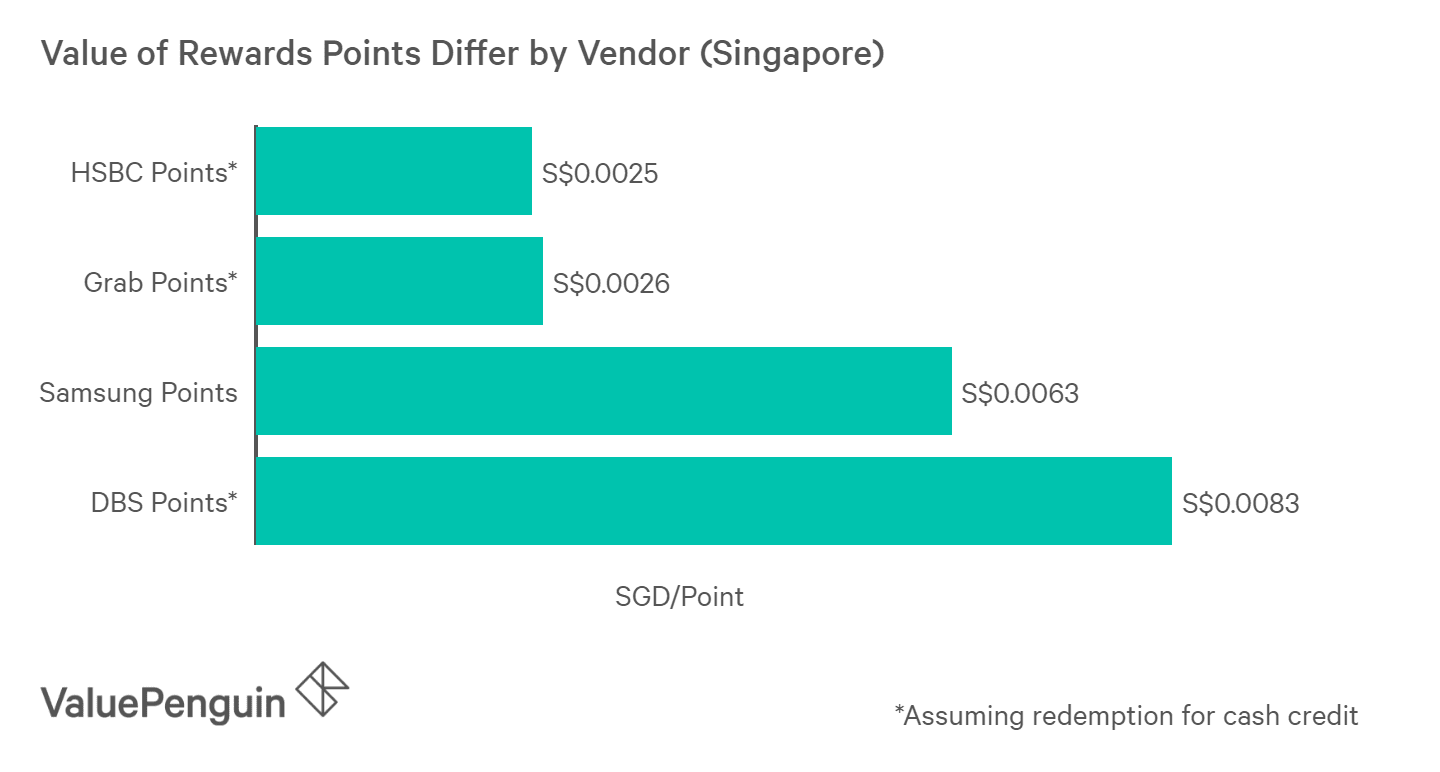

First, marketing phrases like “5x points” can be very misleading because not all points are worth the same. Even if a card promises 10x points for every dollar you spend, you could be earning more with another card that promises 5x points per dollar if the points themselves are worth different amount. For example, many banks offer reward points that are worth about S$0.0025 per point when converted into cash credit. However, other banks like DBS’s points are worth S$0.008, while Grab Points are worth about S$0.0025 each. However, this doesn’t mean DBS cards are worse than other cards because different banks will provide different amount of points per dollar. Therefore, when choosing which card or payment platform to use, consumers have to compare how much reward they can receive in dollar terms instead of merely going for the option that provides more points.

Not only that, credit card rewards points tend to be much more useful than “newer” rewards points that one can earn by using a mobile payment app. First, many mobile payment apps actually require users to top-up their app accounts with credit cards; often, this could prevent users from earning credit cards rewards like miles and rebates on their purchases which tend to be much more significant than rewards from the apps. Not only that, while credit card points can be redeemed for cash back (i.e. statement credit), vouchers and miles, points from mobile payment apps seem to be more limited in their redemption methods.

Not All Redemptions Are Worth the Same

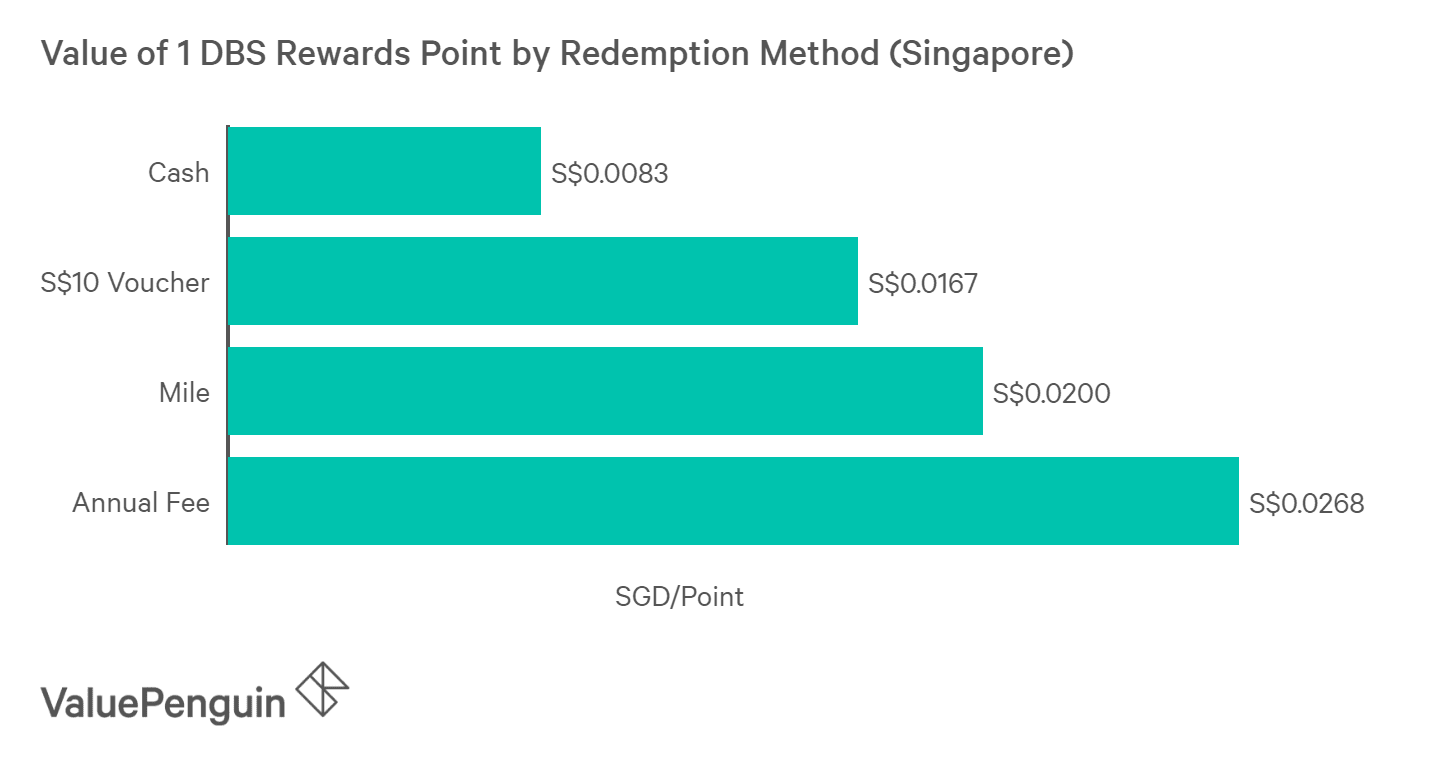

Secondly, a lot of consumers make the mistake of redeeming their points for anything that comes to mind. However, this can be a very big mistake because a point’s value can vary widely depending on the redemption method. As a rule of thumb, redemptions that have more restrictions tend to be worth more. For example, a point at HSBC or OCBC can be redeemed for cash credit for about S$0.0025. However, it could be worth up to 2x more when being redeemed for miles or an annual fee waiver.

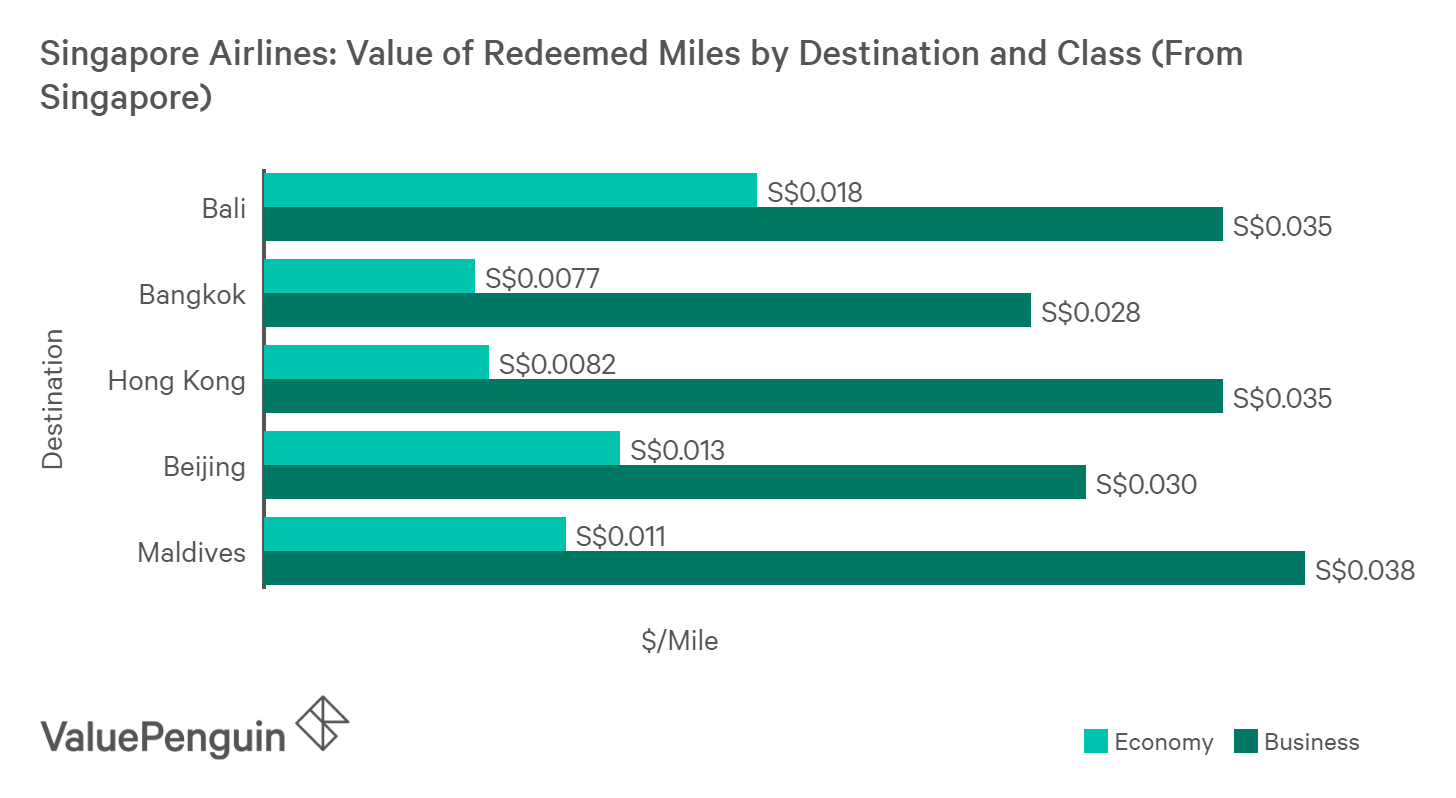

Not only that, miles themselves can vary in value depending on their redemption method. In fact, miles redeemed for more expensive flights tend to be worth much more than miles redeemed for cheap flights. While we assumed value of S$0.01 per mile for our calculation above, a mile can actually be worth 3-8x that amount for more expensive business or first class tickets.

Hoarding Points Can Backfire Over Time

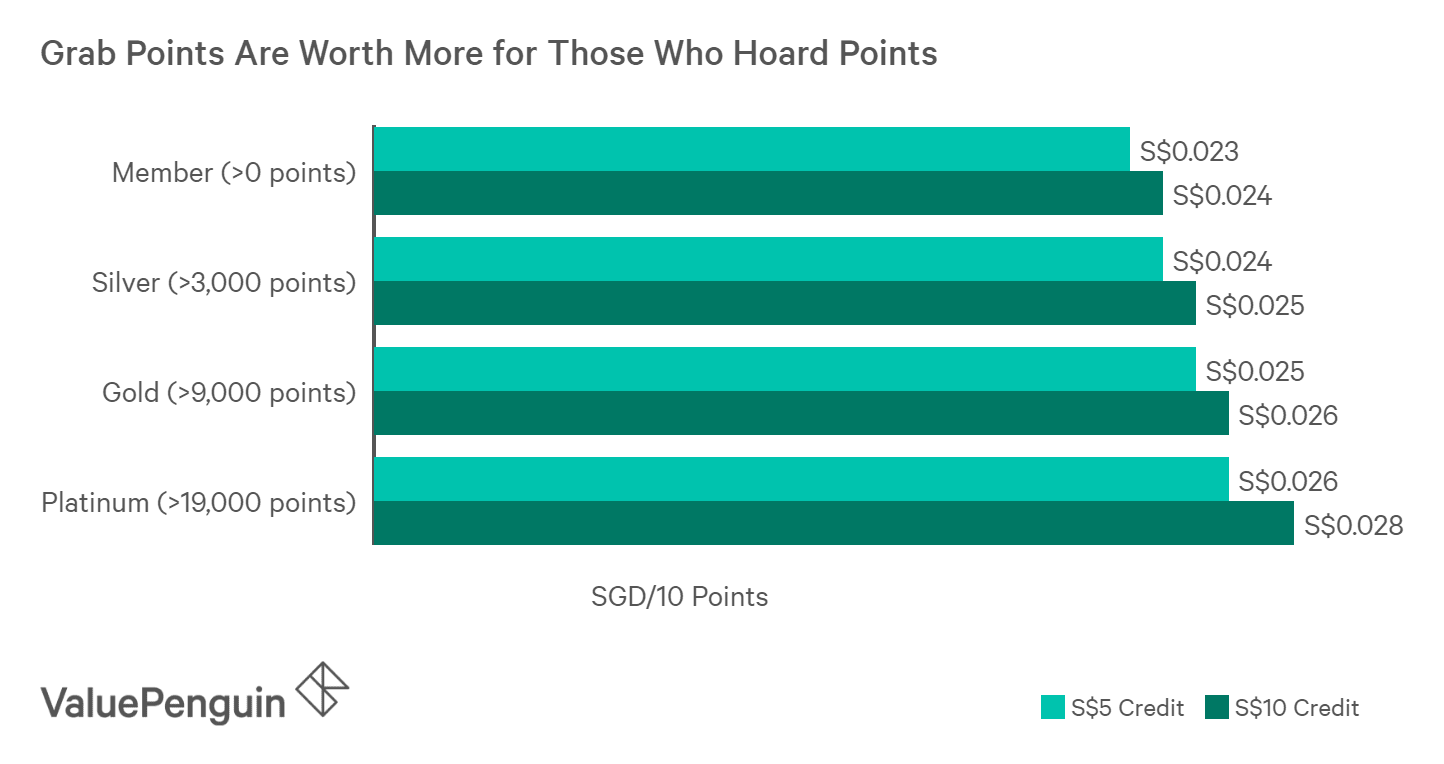

Last but not least, some points providers will try to encourage people to hoard their points for a long time by providing certain incentives. For example, Grab users get different rewards status and better redemption options depending on how much points they hold. While the increase in benefits from this type of tier system are sometimes quite meaningful, going overboard with the hoarding strategy can back fire over a long period of time for two reasons. First, unlike cash, points cannot be invested to increase in value. This means that a point’s worth will gradually decline along with inflation. Not only that, many points or miles providers all over the world have also actively devalued their rewards over time to reduce their costs. From this point of view, actively redeeming points whenever you have an opportunity could be a better way to maximise the value of your points.

How to Maximise the Value of Your Rewards Points

To make sure you get the most bang for your buck when it comes to rewards points, it is first and foremost imperative that you find the right product that fits your needs. If it’s a credit card, you want to make sure you find one that provides the most rewards (in dollar terms) for your biggest spending categories. If it’s a mobile app, you want to choose one that you actually can use frequently because it is widely accepted everywhere. Once you’ve found the right products and you are earning points, it is generally wise to redeem points for miles, vouchers or annual fee waiver than for cash credit. Lastly, you should aim to redeem your points at least once every two to three years; they can sometimes decline in value if you wait too long, if not expire.

The article 3 Rewards Point Traps That Singaporeans Fall For originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

- Best Rewards Credit Cards 2018

- Best Cashback Credit Cards 2018

- Best Credit Cards for Online Shopping & Mobile Payments 2018

Source: VP