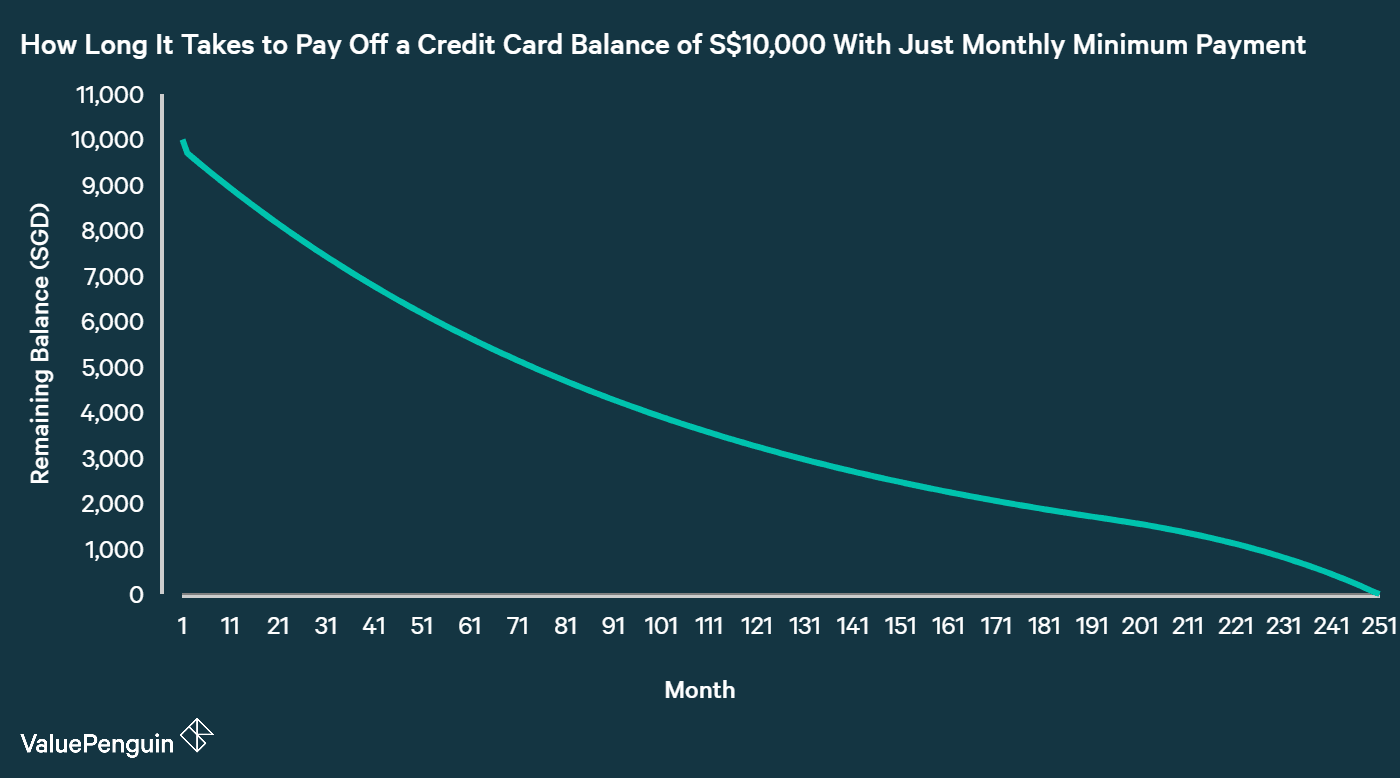

One of the biggest myths prevailing in credit card usage is that minimum monthly payments are designed to help consumers get rid of their balance in a timely fashion. However, as we are about to demonstrate for you below, such a statement cannot be farther away from the truth. In fact, making only the minimum payments on your credit card bill can cause your interest charges to skyrocket, inflating the total cost of your credit card debt. According to ValuePenguin’s calculation, making only the minimum payment requirement every month on a credit card balance of S$10,000 can take you 21 years to pay down your entire balance.

We based our calculation on two things. First, the average APR of credit cards is around 25%. Then, to obtain the time it takes to pay off a balance of S$10,000, we modeled credit card debt payback by using a method that most banks use to set their monthly minimum card payment: 3% of remaining balance or S$50, whichever is greater. Each month, a consumer reduces the balance by the minimum payment amount, which is offset by some increase in balance from interest charges. Because your payments are based on the percentage of your outstanding balance, as your debt shrinks so do your payments and interest charges.

Based on this methodology, we calculated that it takes about 21 years for a Singaporean to pay off his credit card debt of S$10,000 if he only pays the monthly minimum payment required. Over this quarter of a century, the consumer would pay approximately S$20,000 in interest – all of this, under the optimistic assumption that no new charges are put on the account. While it is possible a consumer may be able to afford paying significantly more towards their bill, minimum payments extend the total time it takes to repay the debt.

How to Avoid the Pitfalls of Minimum Credit Card Payment

Though it may seem unbelievable at first glance,these numbers represent just how much of a financial trap minimum credit card payments are. This problematic financial situation can be avoided in several ways.

First, it’s never a good idea to carry a balance on your credit card – ever. If possible, you should always avoid putting any charges on your card that cannot be paid off in full by the end of the month. Letting this rule slip, little by little, can quickly cause your debt to snowball into an out of control beast.

Secondly, it’s generally a good idea to create a fixed monthly payment schedule for your credit card bill. Ideally, you should be putting away as much as you can afford towards your credit card bill: the goal is always to pay down your balance entirely as quickly as possible. Merely putting a dent in your total outstanding balance doesn’t mean you should relax and pay less. If the average consumer we examined were to pay S$400 every month, the time needed to pay down that debt would be cut down to 3 years, reducing their total interest paid by close to $3,848.

Lastly, if you have too much balance for you to pay back soon, you may want to consider getting either a balance transfer or a debt consolidation plan. These instruments can help you avoid high credit card interest for a few months or to a few years. Typically, balance transfer loans are ideal for smaller amounts that take 12 months or less to payback, while debt consolidation loans are great for bigger balances that take a few years to repay. Using either of the instruments can help you save thousands of dollars in cost, and help you repay your obligations more quickly.

The article Why You Should Avoid the Monthly Minimum Credit Card Payment Trap originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

- Best Credit Cards with Promotions 2017

- Best Debt Consolidation Plans 2017

- Best Personal Loans in Singapore 2017

Source: ValuePen