So you got your driver’s license and your hands are itching to grab the keys to your very first car. As exciting as the prospect of tearing up the pavement in your new whip must be, owning a car in Singapore is no simple matter — especially as a millennial. As a matter of fact, it’s more expensive to be a carowner as a millennial than it is for any other age group. So to help ensure your life as a driver gets off to a smooth start, our team at ValuePenguin compiled a list of the top things millennials buying a car in Singapore should know.

How Much Car Can You Really Afford?

When buying your first car, you may feel tempted to “go big or go home.” After all, with the help of a car loan, getting that entry-level Mercedes to show off to your friends shouldn’t be that big of a deal, right?

Wrong. It is incredibly expensive to own a car in Singapore, from the initial sticker price, to regular upkeep, to daily costs you may not have considered yet. The last thing you want to do is saddle yourself with large recurring costs that’ll keep you strapped for cash for years to come, particularly as your professional life is just getting started. So we would advise that you err on the conservative side as you try to figure out how much car you can really afford by weighing the following considerations.

Consider Getting a Used Car

One of the first things you’ll want to keep in mind is that it costs more to buy a car in Singapore than it does practically anywhere else in the whole world. This is due to a couple of factors. For one thing, all of Singapore’s cars are imported from overseas, which has a cost (import tax, shipping, etc.) Consumers bear the brunt of that cost, which is factored into the sticker price you see at dealerships. Also, thanks to Singapore’s COE system, a new Toyota Corolla Altis 1.6 would run you about S$100,000. And that cheapest Mercedes C-Class model you’ve been eyeing would cost you nearly S$190,000.

Let’s say you bought a new Toyota Corolla Altis at the aforementioned price of roughly S$100,000, and borrow S$50,000 (50% of the purchase price) over 7 years to fund the purchase. If you used DBS, which currently charges 1.99% in flat interest and is one of the best car loans for new cars, you will need to pay a total of S$4,975 in interest, translating to equal monthly instalment payments of S$678.15 to pay off the loan on time. Consider the fact that the median monthly salary for university graduates was S$3,360 you’d be spending 20% of your pre-tax monthly income on your car loan payments alone.

An alternative we recommend is not purchasing a new car at all. The value of a car depreciates over time, depreciating the most within the first few years of its lifespan. This means that you can get great bang for your buck by buying a used car that’s still pretty new – like 3 or 4 years old – and still has a lot of miles left on it, saving yourself a good chunk of cash. For instance, a Toyota Corolla Altis 1.6 registered in 2014 currently lists at about S$80,000. You’d save 20% just by buying a 3-year-old car compared to a new one. Let’s assume you financed this purchase with a S$30,000 car loan from OCBC for over 7 years at its flat interest rate for used cars of 2.87%, paying the same down payment of S$50,000 upfront. You’d end up paying less in total interest over the 7 years (S$4,470) than you would for the new Toyota, and even more impressive, your monthly instalments would only be S$431.64, 36% lower than the alternative. This can free up over S$200 a month compared to how much you’d need to spend per month on paying off the loan for the new car.

And, of course, you can always buy a well-used car for a bargain from an authorised car dealership of one of the big brands, from a smaller used car dealership, or from your uncle.

Car Insurance is Especially Expensive For You – Don’t Be Fooled

The purchase and upkeep costs of the vehicle itself are not the only expense you’ll need to prepare for as a newly-minted carowner. You’ll have to factor in the cost of car insurance as well — and as a millennial, you’ll have to pay more than everyone else. This is the main reason car ownership is so much more expensive for millennials than other generations: Because younger drivers in their 20s and early 30s are statistically more likely to get into a car accident than older drivers, car insurance premiums are also higher for drivers in their 20s and early 30s. Our study of the average car insurance costs in Singapore found that drivers in their 20s have to pay an average premium of S$2,292 for a Toyota Corolla Altis compared to S$1,463 for drivers in their 30s and S$1,430 for drivers in their 40s. These figures assume 0% NCD and are the mean of premiums obtained for male and female driver profiles.

Don’t forget the extra excess you may have to pay as a millennial

If that weren’t enough, you also have to bear in mind that most insurers will also make you pay more out of pocket to cover repair costs after you have a car accident before their coverage will kick in due to your younger age. This policy is known as the “Young and/or Inexperienced Driver Excess” (“YIDR”) and is tacked on top of the “standard excess” everyone has to pay before car insurance will cover the cost of repairs when you file a claim. While the standard excess will typically cost you in the area of S$600 to S$1,000 depending on the terms of your policy, you’ll also have to pay the YIDR in addition, which will typically cost anywhere between S$2,000 and S$3,000. So if you buy a car insurance plan with an unforgiving YIDR policy that considers you a “young” driver, you could find yourself paying as much as S$4,000 out of pocket to fix your car before insurance will step in to help.

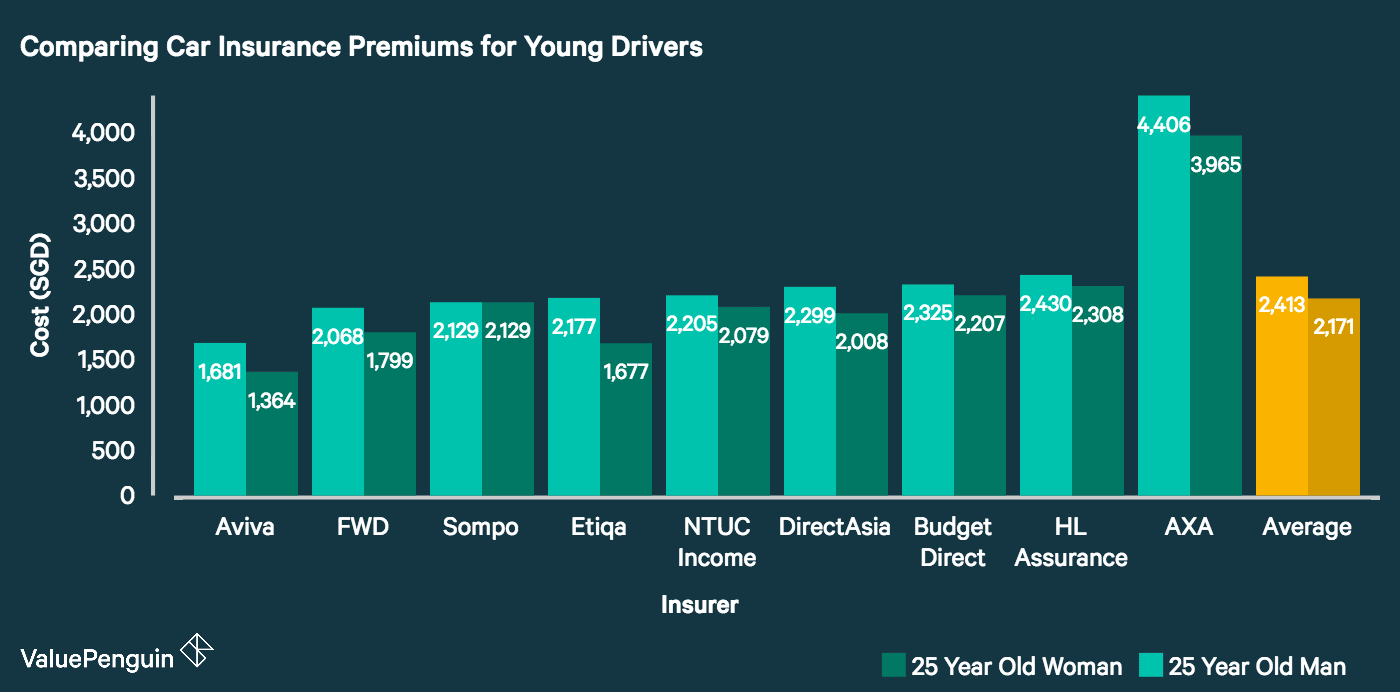

The good news is that by doing your research, you may be able to find a car insurance plan that won’t make you pay the additional young driver excess. This is because not only do different insurers charge a different amount of money for their YIDR, but they also have different age cutoffs after which you’ll no longer be susceptible to the additional excess. Our team at ValuePenguin compared the young driver excesses at a variety of Singapore’s top car insurance providers so that you can compare each policy to your situation and pick a plan that’s right for you.

| Company Policy | Annual Premium for 25-Year-Old Male Driver | Young and/or Inexperienced Driver Excess |

|---|---|---|

| Aviva | S$1,681.17 | S$2,500 for drivers aged 24 and below |

| FWD Classic | S$2,068.27 | S$2,500 for drivers under the age of 27 |

| Sompo ExcelDrive FOCUS | S$2,128.87 | S$1,500 for drivers under the age of 23 years old if designated as a named driver. If not named, S$3,000 |

| Etiqa Private Car Policy | S$2,177.49 | S$2,000 for drivers under the age of 27 |

| NTUC Income Drivo Classic | S$2,205.48 | S$0 if designated as a named driver; if not named, S$2,500 if unnamed driver is under the age of 27 |

| DirectAsia Value | S$2,289.95 | S$0 if designated as a named driver; if not named, not covered by the plan |

| Budget Direct | S$2,324.71 | S$500 for drivers below 25 years old if designated as a named driver. If not named, S$1,500. Additionally, S$500 for drivers with less than 2 years’ possessing a valid driver’ license if designated as a named driver. If not named, S$1,500. |

| HL Assurance Car Protect360 | S$2,429.94 | S$3,000 for drivers under the age of 27 |

| AXA Essential | S$4,405.82 | S$500 for drivers under the age of 27 if designated as a named driver. If not named, S$2,500 if below 27 at AXA Premium Workshops; S$5,000 if below 27 for non AXA premium workshops |

| Average Premium | S$2,427.77 |

Overwhelmed? Consider These Alternatives to Car Ownership

If all of this seems totally overwhelming to you, you may wish to consider the following creative alternatives to owning a car yourself:

- To circumvent dealing with the expense and inconvenience of actually owning a car in Singapore, some Singaporeans have taken to renting cars from Uber, driving them a few hours a day as Uber drivers, and using them the rest of the time for personal use. According to our study, you’d only have to drive between 2 and 3 hours a day to break even on your Uber rental.

- With the right cashback credit card, our analysts at ValuePenguin have found that it may actually cost less to use ride-sharing apps like Grab and Uber for all your transportation needs than to own a car yourself in Singapore. The Citi Cash Back Card and Standard Chartered credit cards, for example, offer 20% off on your Uber and Grab rides.

Closing Thoughts

Ultimately, buying a car is a daunting investment, and all the more so for young professionals in Singapore. Nevertheless, the more you know before pulling the trigger on such a big purchase, the better equipped you’ll be to surmount the obstacles along the way.

The article Top Tips for Millennials Buying a Car in Singapore originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

Source: ValuePen