If you need money urgently and cannot borrow it from a friend or a family member, a tempting alternative might be to get a cash advance against your credit card. All you need to do is just walk up to an ATM and use your card to withdraw the funds that you need. Although it may be convenient, however, a cash advance can be extremely costly, costing 24-29% of annual interest rate on average.

If your need for cash is not immediate, a personal loan from a bank could be a much better alternative option. Given that personal loan’s average cost is about 12-15% per year on average, personal loans can help you save hundreds if not thousands in interest compared to taking out a cash advance. But how easy is it to get these loans, and what should you do if your credit score is not good enough for a personal loan?

Your next best option – pawnshops

If you own any valuables and need money in a hurry, a pawnshop could be the best choice. These businesses specialise in providing loans against your valuables such as gold jewellery, expensive watches, and electronic goods among other high-priced items.

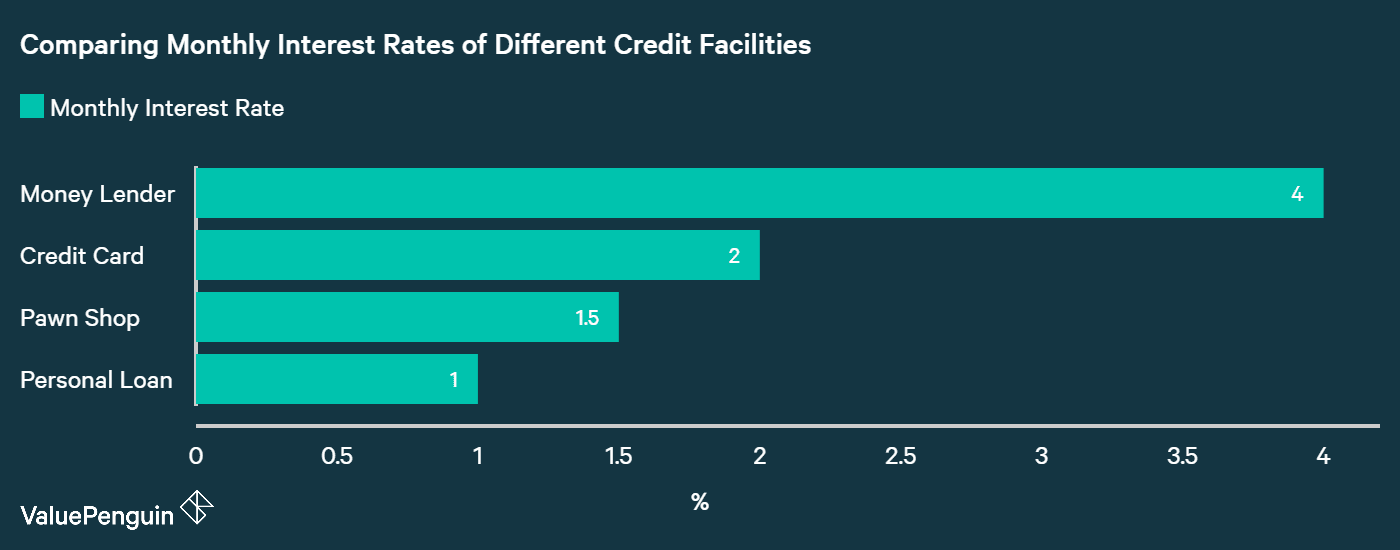

Contrary to popular belief, the interest rate being charged at these pawnshops can be surprisingly low. By providing your valuables as collaterals, you can expect to pay about 1.5% per month for a six-month loan, higher than 1%-1.2% of personal loans but definitely cheaper than credit card cash advances or loans from money lenders.

There is one major disadvantage about raising money by pawning your valuables: if you are providing a gold necklace worth S$10,000, then you may be able to get a loan of only S$6,000 to S$7,000 six to seven thousand dollars from a pawnbroker. However, you can still get back your valuable item as long as you make your repayments on time. The pawnbroker will sell your necklace after giving you due notice only when you default on repayment.

Bad credit and no valuables to pawn?

For those who can’t raise money from anywhere else, there is still one course of action remaining: they can turn to a moneylender. These businesses could be called “lenders of last resort” for individuals. Why should you consider a moneylender as the last place you should approach for a loan? Any why would a moneylender be willing to advance funds to you even though no one else is willing to?

The answer to both these questions lies in the . Moneylenders levy extremely high charges, about 2x higher than credit cards and 4-5x higher than personal loans. Consequently, they can afford to have very lenient credit norms as losses from bad loans from some customers can be made up from the amounts repaid by other borrowers.

| Loan Details | Legal Maximum Cost |

|---|---|

| Initial fee | 10% of the loan amount |

| Interest rate | 4% per month |

| Late fee | S$60 for each monthly late payment |

| Late interest charges | 4% per month |

Avoid moneylenders if you can, personal loans are the most economical option

As you can see, it is highly imprudent to borrow from a moneylender due to their extremely high costs. Paying an interest rate of 4% per month, which translates into 48% per year, can ruin your financial health if you are not extremely efficient about repaying your loan quickly. In contrast, personal loans from banks offer rates that can be one-fourth of those charged by moneylenders. If you have a poor credit record and are ineligible to borrow from banks, it may be a good idea to start working on improving your credit score. With a little effort and planning, you could soon be an acceptable credit risk for a traditional lender like a bank.

The article Which Loan Should You Get in Singapore With Not-So-Perfect Credit? originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

- Best Credit Cards with Promotions 2017

- Best Credit Cards with Promotions 2017

- Best Cashback Credit Cards 2017

Source: ValuePen