-&-who-should-buy-it?")

A wealth accumulation tool, investment-linked policies may take some time for many to understand, especially with its extreme fund flexibility coupled with unexpected additional fees.

Let us help you break it down!

What is an Investment-Linked Insurance Plan (ILP)?

An Investment-linked insurance policy (ILP) is a policy that has life insurance coverage and investment components. Most policies contain various packaged funds with diversified risks for consumers to choose from according to their risk appetite. These respective funds would have various sub-funds in stocks, bonds, and more.

A consumer’s premiums would be used to pay for units in the sub-fund of their choice. Some allow consumers to choose their sub-funds, while others, like Great Eastern’s GREAT Series 10, have pre-allocated packaged funds for consumers to pick. When needed, some of these units purchased may be sold to pay for other charges, such as management charge fees. The management charge fee is charged monthly by deducting away the units that the customer has. The remaining amount would stay invested accordingly into the pre-allocated ILP Sub-Funds.

In the event of death, ILPs provide insurance protection for the policyholder. A claimant can be paid a lump sum payment of the policyholder’s account value or between 101% to 105% of the net premium. The net premium refers to the initial premium you placed in the policy, considering any top-ups or withdrawals you made.

There are two main types of ILPs – single premium ILPs and regular premium ILPs. With Single premium ILPs, you pay a one-time lump sum premium to be invested into a sub-fund. With regular premiums ILPs, you make premium payments on an ongoing basis. Single-premium ILPs typically provide slightly lower insurance coverage than regular premium ILPs.

| Net Premium = Total Premium Paid + Top-up – Withdrawals |

|---|

Why do people get Investment-Linked Policies?

Many people get Investment-Linked Policies for the following reasons:

- For flexibility of cash flow in their insurance coverage and wealth accumulation.

- For wealth growth. These individuals mostly have their basic coverage already done up.

- For individuals considering temporarily taking a “one stone kill two birds” approach and are uncertain on whether to focus their finances on insurance protection or wealth accumulation.

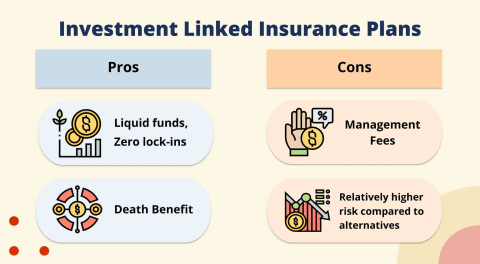

Pros of Investment-Linked Plans

Liquid funds with zero lock-ins.

As long as the minimum value needed is present in the account, most Investment-Linked Policies allow for partial withdrawals at any time throughout the policy’s lifetime. This gives users the option to draw from their policy if they need cash now in the case of an emergency.

Moreover, many policies allow policyholders to make top-ups according to their financial means. Some policies have options for ad-hoc and recurring top-ups according to one’s preference, subjected to various minimum top-up values. You can adjust your premiums as your income grows to grow your wealth quicker with your Investment-Linked Policy.

Some Investment-Linked Policies also allow policyholders to switch their packaged funds to suit their financial means or risk tolerance. Other Investment-Linked Policies provide their policyholders with the option of a “premium holiday” where premium payments can be temporarily stopped without the policy being terminated. Both of these increase the flexibility of ILPs as a wealth enhancement tool.

Death benefit

With a death benefit, claimants upon a policyholder’s decease or officiation of terminal illness are usually able to retrieve a lump sum of money. For Great Eastern’s GREAT Series 10, this death benefit comes as a lump sum payment, which is the higher amount between 105% of the single Premium paid or the surrender value of the policy, less any indebtedness under the policy.

Cons of Investment-Linked Plans

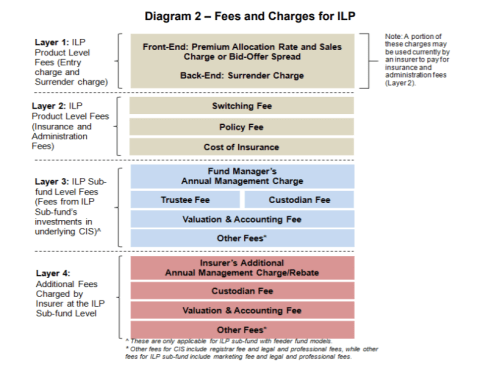

Fees and charges

ILPs have many layers of unseen costs. Often, these fees amount to a hefty price. Sometimes more expensive than separate life insurance policies and investments combined. Below is a chart of ILP fees and charges from the Monetary Authority of Singapore.

As a result, the premiums placed into Investment-Linked Policies are not fully used to invest, as some would be used to foot the costs of these fees.

Relatively higher risk compared to other options

It is important to read the fine print when purchasing an ILP. Like other financial investment products, an Investment-Linked Policy carries investment risk and does not always provide guaranteed returns. This may make ILP’s unfavourable compared to other life insurance alternatives, like an endowment insurance plan.

GREAT SP Series 10 is an example of an ILP that does provide guaranteed returns. The policy assures that the guaranteed survival benefit of 4% of the single premium will be payable on survival of the life assured at the end of the policy term.

With non-guaranteed policies, to keep losses within their policyholders’ risk appetites, insurers have different packaged funds with diversified risks to suit different consumers.

When policyholders have full control over choosing their packaged funds, policyholders need to bear the financial risk of their investments. Hence, it is crucial for you to be aware of the amount of risk you are willing to take before purchasing a packaged fund. If you have the financial capacity to afford this risk, investing in an ILP might potentially bring returns higher than other participating plans (e.g. whole life policies or endowment insurance plans).

What should I look out for before investing in an Investment-Linked Policy?

When choosing a suitable ILP, it is important to avoid common misconceptions. Beyond that, below are some traits that you can look out for when considering purchasing an ILP.

A low and affordable starting premium

This gives you room to experiment without breaking the bank. If you wish to withdraw completely from the ILP, any penalties will also be minimised.

Clear packaged funds

Compared to ILPs that allow policyholders who might not have the necessary investing knowledge to pick their sub-funds, packaged funds are sub-funds pre-picked by insurers that are experienced in the market. This allows ILP investors a clearer understanding of the financial risk they are taking when they choose to purchase an ILP. Through this, they can better select a fund more suited to their risk appetite.

Clear charges and fees

Clear charges and fees will help you estimate the total cost you might incur if you purchase this ILP. This will allow you to better see where it will function in your financial plan and weigh the growth it may achieve in the long run.

Great Eastern’s GREAT SP series 10 is a great starting point for those seeking exposure to Investment-Linked Policies. With a low starting sum of S$10,000, a short maturity period of only one year and guaranteed returns of 4%, it is a good policy to consider if you are keen to dip your toe into Investment-Linked Policies without committing long-term.

What is GREAT SP Series 10

GREAT SP Series 10 is a single premium investment-linked insurance plan.

With a starting principal sum of S$10,000 and a maturity period of only one year, policyholders can get 4% guaranteed returns and 100% capital guaranteed at maturity. This rate is extremely competitive and is comparable with some of the fixed deposits with higher returns that are currently available on the market.

What makes the GREAT SP Series 10 policy more attractive than other investment vehicles with similar returns, such as fixed deposits, is that it provides added insurance protection with guaranteed acceptance. Upon death or terminal illness, GREAT SP Series 10 provides additional insurance protection at no extra insurance charge. This protection comes as a lump sum payment to the policyholder’s claimant. It would be either 105% of the single premiums paid or the surrender value of the policy, whichever is higher, less any indebtedness under the policy.

The whole premium is invested upon initiating the policy. Policy Protection will be up to specified limits by SDIC.

This policy can be purchased by any Singapore Resident with a valid NRIC or FIN between the ages of 17 to 80 (age next birthday), subjected to full knowledge and understanding of the requirements demanded by the plan.

You can refer to the table below for features of GREAT SP Series 10:

| Details | GREAT SP Series 10 | |

|---|---|---|

| Premium | Single Premium | |

| Principal Capital | Minimum of S$10,000 | |

| Returns | 4% guaranteed returns | |

| Maturation Period | 1 year | |

| Insurance Protection upon Death or Terminal Illness | The higher of the two:

|

|

| Are there additional insurance charges? | No. There are no insurance charges. | |

| Amount of premium invested | 100% of the premium will be invested. | |

| Policy Protection | Up to the specified limits of SDIC | |

How can I learn more about GREAT SP Series 10?

Learn more about GREAT SP Series 10 here!

The policy is underwritten by The Great Eastern Life Assurance Company (Company Reg. No. 190800011G).

As buying a life insurance policy is a contractual commitment, early termination of the policy usually involves high costs and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid. You should seek advice from a financial adviser before purchasing the policy. If you choose not to seek advice, you should consider if the policy is suitable for you.

This content is for reference only and is not a contract of insurance.

Full details of the policy terms and conditions can be found in the policy contract.

This policy is protected under the Policy Owners’ Protection Scheme administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic, and no further action is required. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact us or visit the Life Insurance Association (LIA) or SDIC websites.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Information is accurate as of the article reviewed on 07 March 2023.