{kind=link}

The decision not to have kids is becoming more prevalent, with Japan, South Korea, Hong Kong, the United States and a handful of European countries seeing a decline in family size over the past decade.

The reasons for not having a child are plenty. Whether it is struggling to find financial stability or placing greater priority on career growth, there is a myriad of reasons why people forego having children.

However, the underlying theme for all of these reasons is money. Having a child is expensive anywhere but can be especially costly in cities like Singapore. So how much does it cost to raise a child in Singapore? We break down the expenses below.

Pregnancy & Healthcare Costs

Spending money on a child starts before they’re even born, as it is imperative for mothers to ensure the well-being of their future baby. Taking maternity exercise classes to stay in shape and adjusting one’s diet to ensure the fetus receives the proper nutrients are just some of the costs faced by couples in addition to the standard prenatal doctor visits.

In total, prenatal care can cost close to S$3,000 when taking into account ultrasound visits, vitamins, harmony testing and blood tests. The average bill for childbirth ranges between S$1,143 and S$7,909 for a normal birth or between S$2,228 and S$12,261 for a C-section birth.

In most cases, the cost of childbirth in a subsidised ward will be offset by the MediSave Maternity Package and MediSave limits. However, couples choosing a B1, A or private hospital ward may end up paying between S$1,500 and S$4,909 in out-of-pocket expenses.

In some cases, you may experience pregnancy complications that can add an additional several thousand dollars in out-of-pocket costs, even with coverage from MediShield Life and private insurance.

| Type of Delivery | MediSave Maternity Package LImit |

|---|---|

| Vaginal Delivery | S$1,650 |

| Vaginal Delivery (Assisted) | S$2,150 |

| Caesarean Section | S$3.050 |

| Caesarean Section (w/ Tubal Ligation) | S$3,500 |

| Caesarean Section (Hysterectomy) | S$4,850 |

| Additional Hospitalisation Stay | S$450/day |

| Source: Central Provident Fund Board | |

The birth of your child is the beginning of a lifetime of continual healthcare expenses. Barring any abnormalities and terminal illnesses (which can cost parents thousands of dollars over the course of childhood), you will be responsible for their health insurance premiums and any out-of-pocket medical and dental costs.

Luckily, Integrated Shield Plan premiums are reasonably affordable for children and the full coverage provided by them may keep emergency medical attention affordable. Furthermore, new parents will also receive a MediSave grant of S$4,000 to pay for their child’s MediShield premiums. You can use this grant while your child is a newborn for outpatient visits and vaccinations.

Baby Bonus Scheme

In the Budget 2023 speech, Finance Minister Lawrence Wong announced there would be enhancements to the baby bonus package for Singaporean children born as of 14 February 2023. Parents are now eligible to receive a total of S$11,000 in Baby Bonus Cash Gifts each for their first and second-born children and S$13,000 each for their third child and beyond.

The payout schedule for these cash gifts is in installments of six months for the first six and a half years of the child’s life. This enhancement in the baby bonus can greatly help to alleviate a lot of the costs associated with having and raising a baby during the first few years.

Education Costs

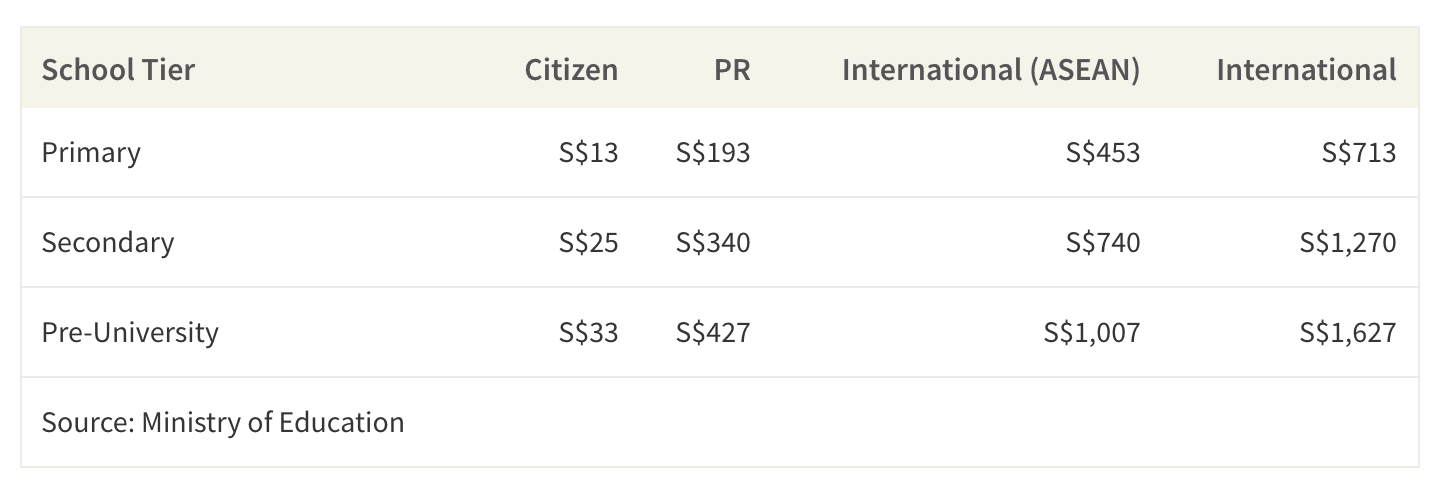

While Singaporean schools aren’t quite as expensive as those in some other countries, they will still cost parents a hefty amount. Quite possibly, your cheapest expense will be your child’s primary and secondary education since Singaporean citizens pay a reasonable S$13-S$33 per month for compulsory education.

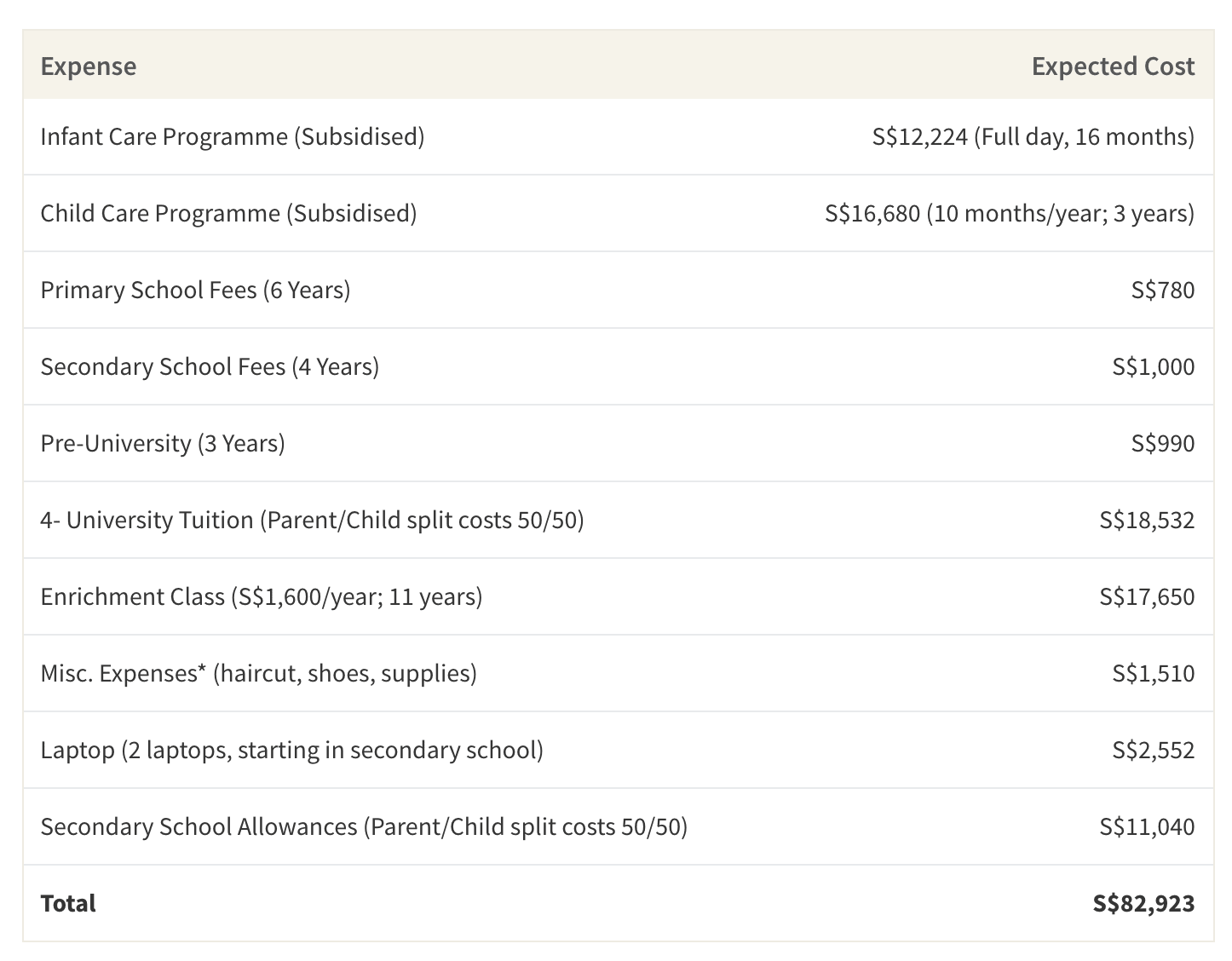

However, if your child is allowed to attend an international school, these costs can increase to S$17,000-S$48,500 per year. Enrichment classes cost another S$1,300-S$1,910 per year. If your child takes 3-4 enrichment classes per year throughout their education, the total cost of these classes can increase to over S$70,600.

Early education programmes like infant care and daycare programmes can also cost quite a bit. For instance, the total cost for 16 months of infant care is approximately S$21,824. The total cost for a 3-year childcare programme averages S$25,680. Lastly, a university can cost you a lot.

Even if you choose to only help your child pay for half the tuition, you will end up paying approximately S$18,500 for a typical 4-year arts & sciences degree. All things considered, you will end up paying around S$83,000 in total just for education-related expenses.

However, it would be unfair to disregard the schemes and subsidies that are available to low-income households, which can bring down the education cost significantly. For instance, students attending Government and Government-aided schools whose families qualify for the MOE Financial Assistance Scheme (FAS) can get free textbooks, school attire and subsidised lunches.

They also do not have to pay any standard miscellaneous or supplementary fees. Furthermore, tuition fees for post-secondary education institutions are also highly subsidised with additional schemes available for Singaporeans that can reduce costs by up to S$4,000 per year. Lastly, working mothers can qualify for subsidies for infant and child care that reduce those expenses by up to 35-44%.

Estimated Total Monthly Education Fees

Travel Costs

While travelling with children can be an enjoyable experience, it is not without its own set of costs. Adding an extra person to your itinerary means spending more money on food, airfare and excursions.

Considering that the average Singaporean household spends S$662 per person on travel per year, this accumulates to S$11,912 for the first 18 years of a child’s life. Families in the upper-income decile who spend an average of S$7,554 per year on travel may spend almost S$40,000 on their child throughout his or her childhood.

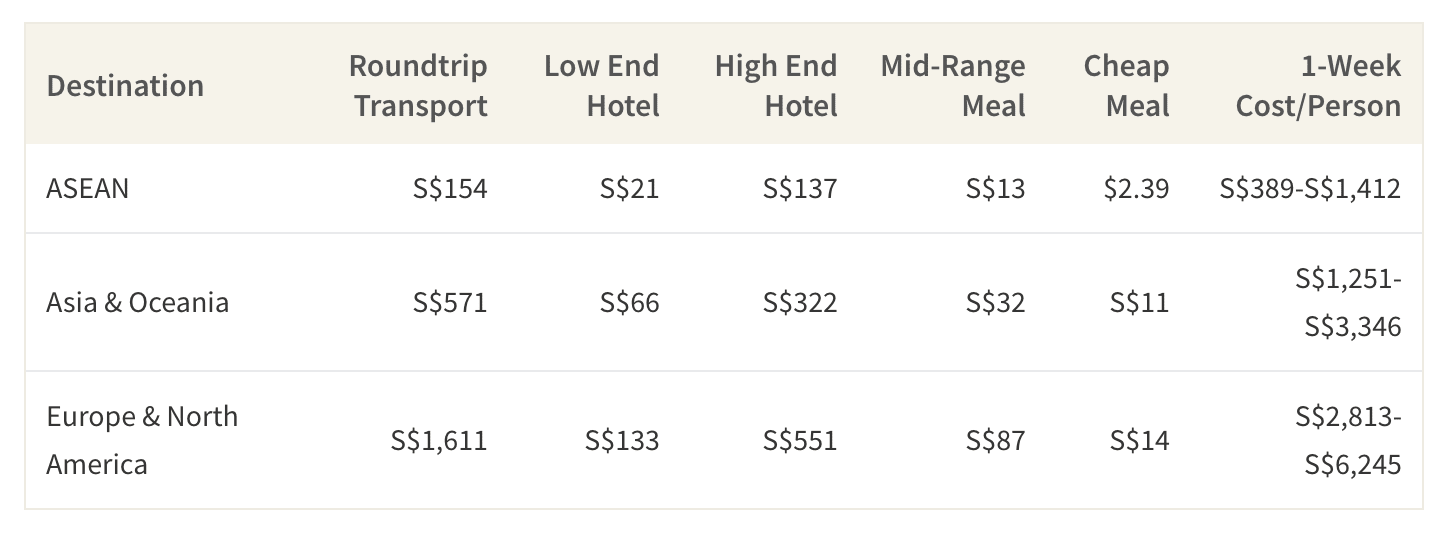

Unsurprisingly, in today’s age of revenge travel, airfare will end up being your greatest expenditure. While travelling with a toddler might not make too much of a dent in your wallet—flights will often offer free seats or discounted rates—-you will have to pay the full airfare each time you fly after your child reaches age 4.

On the lower end, you will be paying S$154 per year for a child’s roundtrip transportation to somewhere within the ASEAN region. However, on the other end of the spectrum, you can be paying as much as S$1,611 in roundtrip airfare should you choose to go to Europe or North America.

Housing Costs

While living in a small flat may be okay for a single person or a couple, you may require more space once you have a child. This means couples will usually have to upgrade their flats to something that can accommodate their new family members. This can be a considerable cost considering how expensive property in Singapore can get. For instance, the average resale price of a 4-room flat is 50% higher than that of a 3-room flat, equivalent to a cost difference of almost S$150,000.

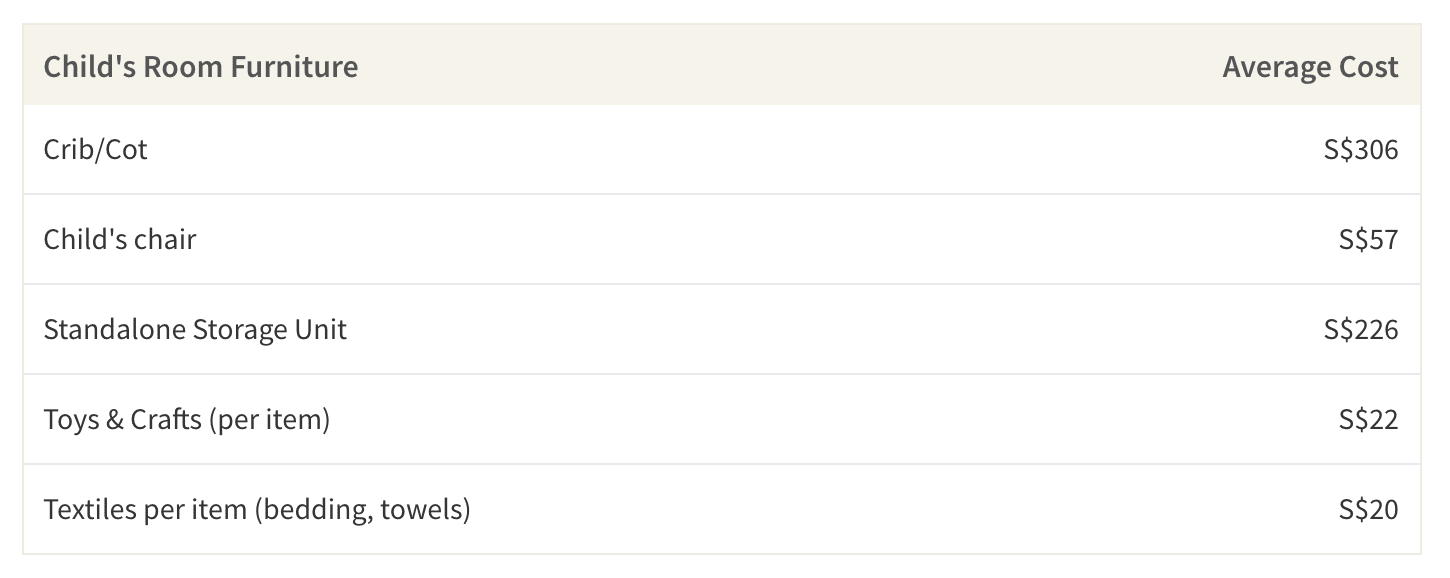

However, whether you decide to stay in your current home or upgrade, you will likely spend money on furnishing your child’s room—and then re-furnishing it several times later to match the age. Calculating how much you’ll spend on your child’s room varies as children require different items at different stages of their life.

While furniture for your baby may cost less than furniture for a 16-year-old, a 16-year-old won’t need sensory toys, safety measures and disposable items such as diapers. On the other hand, a 16-year-old may require an expensive laptop, adult furniture and more expensive entertainment.

Outside Help

If both parents work, it may be necessary to enlist outside help to care for your child during the day. Furthermore, enlisting the help of relatives may be difficult since more and more seniors are working to keep themselves financially afloat. This leaves many parents with the option of hiring outside help, be it a part-time nanny or a full-time domestic worker.

Suppose you hire a part-time babysitter for the four hours between when your child comes home from school and when you return from work at a rate of S$25 per hour. This translates to about S$2,000 per month. A full-time nanny will be even more expensive, due to the comprehensiveness of their care and professional training. They usually command a salary of S$2,500 per month, resulting in a total cost of S$30,000 per year.

Alternatively, full-time foreign domestic helpers (FDW) will set you back S$14,000 for the first year including one-time costs and then S$12,500 thereafter. In addition to this expense, you will also have to take care of a new member of your household—one that you will have to provide for almost in the same capacity as your child. Not only can that add stress to your life, but it can also increase the risk of unforeseen expenses if your domestic worker has an accident or becomes ill.

Food & Clothing

Children also come with plenty of miscellaneous costs. Everything you provide for yourself, you will have to provide for your child as well. To examine these costs, we looked at the typical monthly household expenditure for food and clothing. For instance, the cost of adding one more person to your family can mean an extra S$4,193 spent on food. Over 18 years, your child will be living in your home, which will amount to almost S$75,500. Clothing costs less—only around S$9,900 per additional family member.

However, it is worth noting that these costs will fluctuate depending on your lifestyle. While some families may need to start buying food in bulk, others may already be buying enough food to accommodate a third family member. Furthermore, some families may choose to spend extra on their child’s clothing, while others may be content with getting hand-me-downs from family and friends.

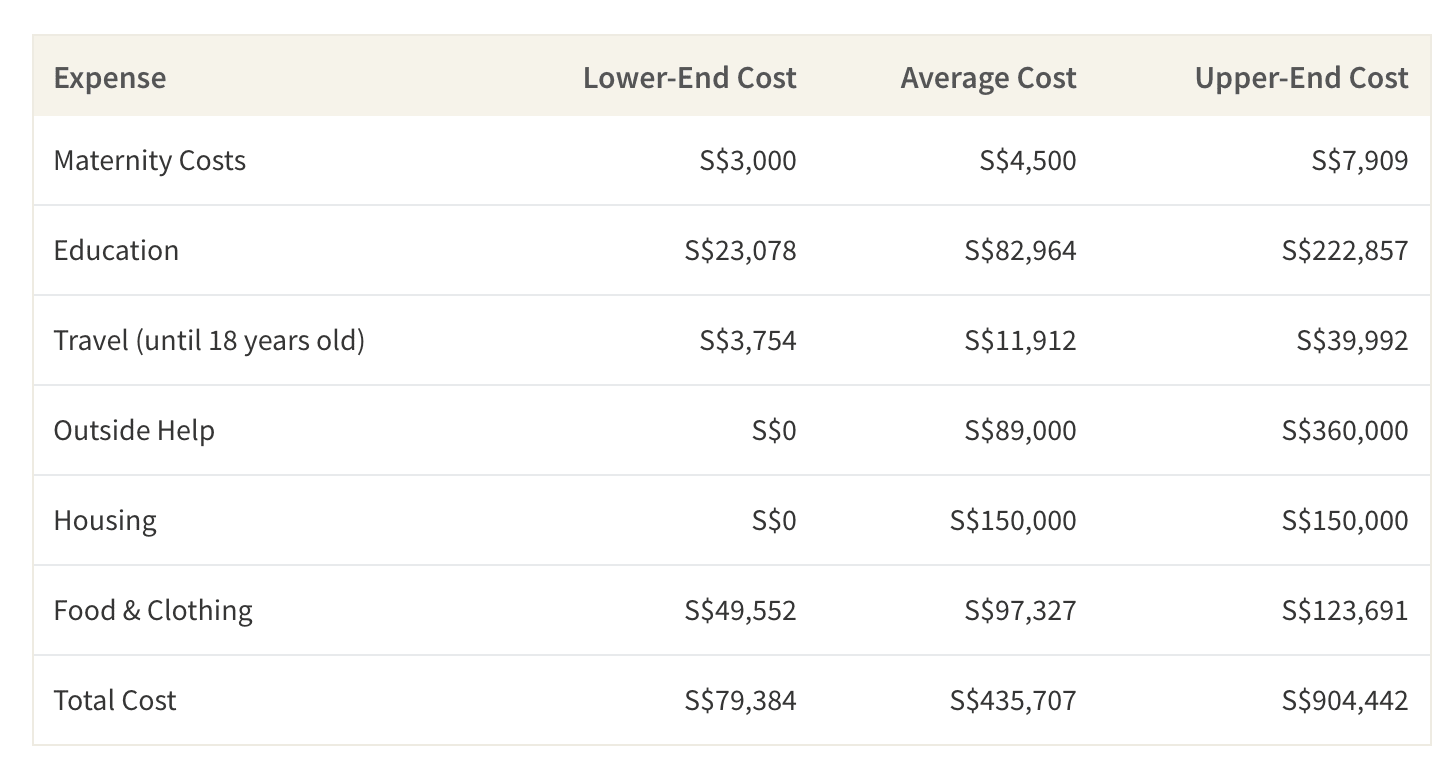

What is the Total Cost of Raising a Child?

Not including healthcare, new housing or additional insurance costs, the first 21 years of your child’s life can cost an average family approximately S$435,707. Thus, when comparing two identical families, the family who chooses not to have a child will save an average of S$20,747 per year for what would have been the first 21 years of the child’s life. Even with the government’s Baby Bonus Scheme of S$11,000 – S$13,000 per child, this sum still amounts to over S$426,000 over the course of childhood.

It is possible that a couple can spend modestly and save money on having a child. For instance, if they qualify for the maximum government subsidies, have familial help while at work and don’t contribute to university tuition, total costs can decline to less than S$100,000. However, considering all the things we did not include in our calculations, that figure can still easily surpass our approximation. Lastly, if the couple doesn’t upgrade their home, they can save an average of S$150,000 from that alone.

This is not to say that you will be better off financially if you choose to not have kids. A child can bring value to a family that is simply not quantifiable. Rather, this article can be used as a hypothetical breakdown for curious couples who want to know whether they can afford to give a child the life they imagined for them. As with most hypothetical scenarios, these costs are aggregates of the status quo and will not reflect everyone’s individual situation. Your cost of raising your child may be more or less than the costs calculated above.

Methodology

To get our calculations, we used publicly available data to examine the top non-negotiable expenses every parent must consider to ensure a healthy and happy life for their child. These costs included childbirth, education, housing, food, clothing and travel.

For healthcare, we included prenatal expenses and basic delivery costs. We kept the S$3,000 prenatal expenses standard but adjusted the delivery fee to reflect the lowest possible bill at a subsidised B2 or C ward to a private hospital ward. The estimated bill at KK Women’s and Children’s Hospital was around S$1,500 for a B1 ward normal delivery with no complications.

On the upper end of the spectrum, we found that the average out-of-pocket costs for private hospital delivery were around S$4,909 for normal delivery. Healthcare is tricky to calculate as there are many factors that can change pricing, including fees for different doctors, type of delivery, complications and whether or not the family chooses to get maternity insurance.

For education costs, we looked at school and university tuition and fees, enrichment classes and infant/child care programmes. Our low-end figure assumes that the couple would receive the maximum subsidy for early childcare, the child gets into university on a full-ride scholarship and the child does enrichment classes at a community centre. On the other hand, our high-end figure looks at no-expense-spared education, consisting of multiple private enrichment classes per week, a medical degree path and no subsidies (i.e. the household earns more than the qualified amount).

Housing and outside help were calculated in a similar manner. Our low-end housing cost estimate assumes that the couple would not move to a bigger flat. Due to constraints, we omitted calculating fringe costs associated with home purchases such as interest rate payments, grants and loans. Similarly, outside help such as nannies and FDWs remained at zero at the low end because, in the best financial scenario, the couple would utilise the help of their parents while they were at work. On the upper end, we kept the costs the same as for the median expenditure because our assumption for this study was that the couple is already living together and would only need to pay the extra amount to upgrade to a bigger home.

Travel, food and clothing were calculated based on the lowest possible expenditure (taking the spending on the bottom quintile of the population) and the highest possible expenditure (upper quintile). We used a basic calculation to estimate the total expenditure over the first 18 years of a child’s life by finding the expenditure per person in the average 3.4-person household.

With that figure, we found the annual expenditure for that person and then multiplied it by 18. This is an overly simplified estimate as children usually take up fewer resources than parents—clothing can be cheaper and food can be shared. Given data limitations, we were also unable to account for household economies of scale, in which families are able to reduce the marginal cost of additional children by purchasing food in bulk, for example.

Having a child also lends itself to indirect costs. These range from everything like higher insurance premiums, new insurance obligations (e.g. life insurance), and utility bills to lost wages if a parent chooses to stop working to take care of the child. These costs are harder to calculate but are necessary to consider when deciding whether or not you can afford a child. We did not include these in our study as they were outside our scope of calculation.

The article How Much Does it Cost for Millennial Families to Raise a Child? originally appeared on ValueChampion.

ValueChampion helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValueChampion:

- Best Life Insurance 2019

- Best Cheap Health Insurance 2019

- Average Cost and Benefits of Health Insurance 2019