You may have heard a friend mention using “cash out refi” to pay for a home renovation or to afford their child’s university tuition. What they are referring to is called cash out refinancing. Also known as a reverse mortgage or second mortgage, it allows property owners to borrow against the financial value of their home. Freeing up that much cash may sound very appealing, but is it really a good way for people to get extra cash?

How Does Cash Out Refinancing Work?

Cash out refinancing allows private homeowners to take out a loan from a bank based on the the homeowners’ equity in their homes. While a traditional home loan can only be used to make the initial home purchase, this special type of loan can be used for many purposes like home renovations, tuition or investing.

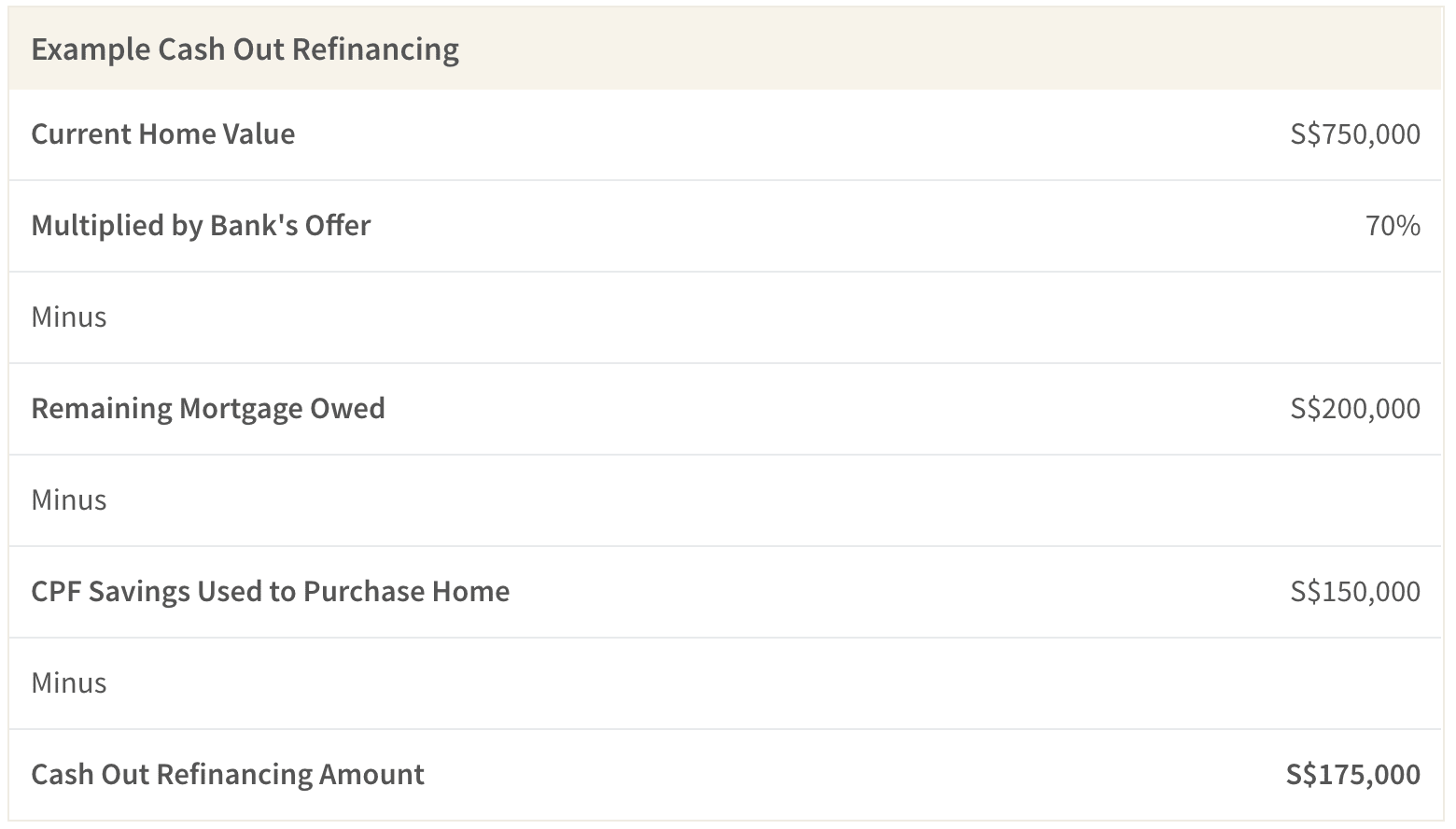

The amount that homeowners can borrow for their property from cash out refinancing is ultimately determined by the value of the home that the homeowner personally owns. The amount that the homeowner personally owns is called equity and is calculated by subtracting the outstanding home loan amount from the current assessed value of the home, which is determined by the bank. Additionally, any CPF savings that were used to pay for the home are subtracted from this amount. Ultimately, banks tend to offer up to 60% to 80% of a homeowner’s current assessed property value as a refi loan. For reference, the table below shows an example cash out refinancing loan.

To get a cash out refinancing loan, you should contact a few banks to compare loan amounts and interest rates. Many banks offer cash out refinancing to private homeowners and typically require a Notice of Assessment, NRIC photocopy and a CPF property withdrawal statement for each borrower.

When Does Cash Out Refinancing Make Sense?

Interest rates for cash out refinancing loans can be significantly lower than those of other types of debt. For example, even the cheapest personal loans charge flat interest rates of 4% to 6%, while education loans and renovation loans charge 3% to 6%. In contrast, most cash out refinancing loans charge interest rates of 1% to 2%. For someone who needs to borrow at least S$20,000, opting for the cash out loan instead of a personal loan could result in thousands of dollars in savings.

Why Should Homeowners Be Wary of Cash Out Refinancing

While the calculation above may make refi loans seem very attractive, it’s not without its own downsides. The reason that banks are able to offer such low rates for reverse mortgages is that the borrower’s property is typically used as collateral. This means that a debtor who cannot repay his cash out refinancing will have his home repossessed by the bank, which can sell the home to recoup its loss. The potential of losing one’s home upon defaulting is the most severe risk associated with cash out refinancing.

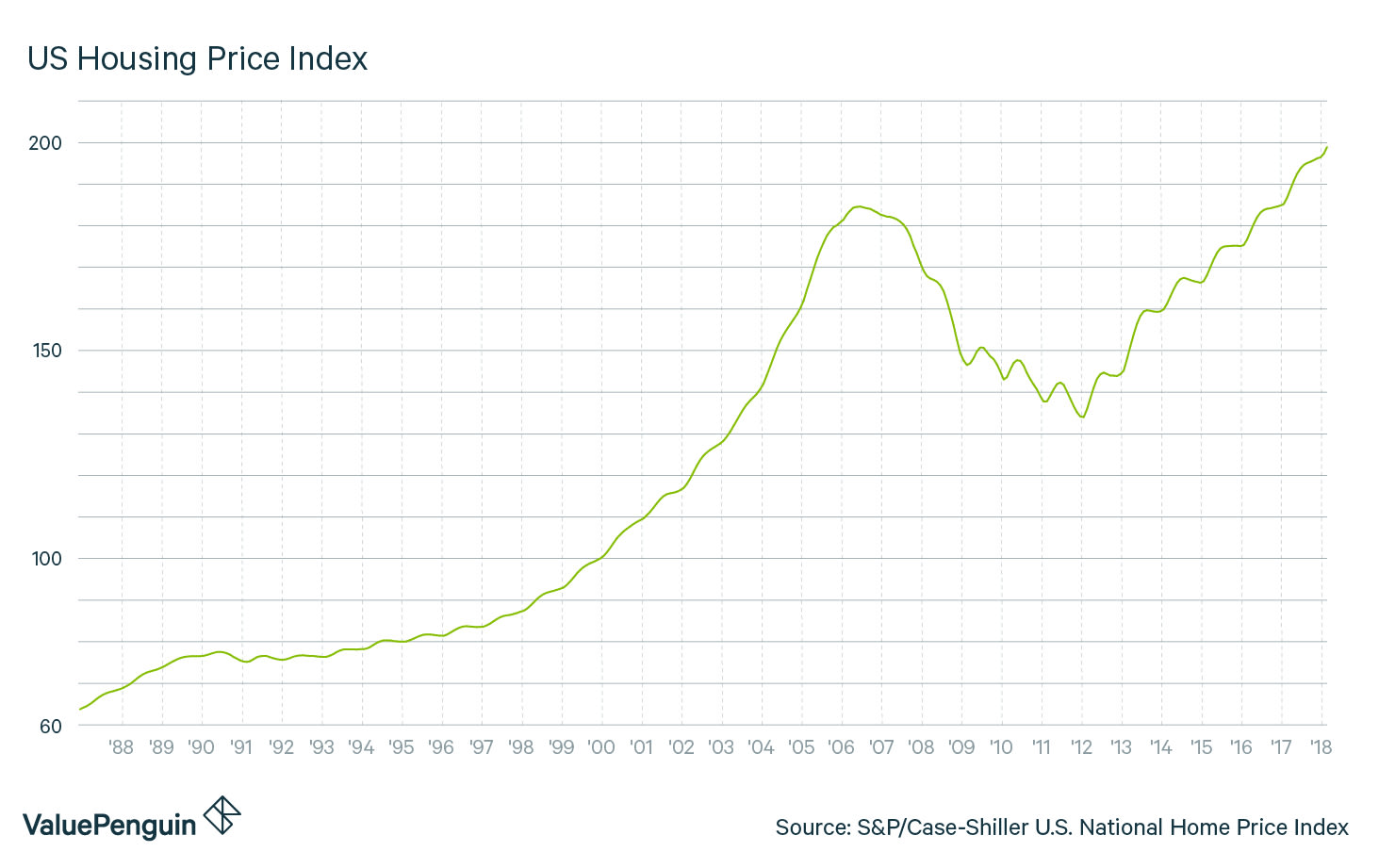

This is a particularly big risk in situations where property values drop significantly. When the real estate market drops, people who took out cash out refinancing may end up owing more money to the bank than the remaining value of their home ownership. This was a significant problem in the United States housing crash of 2008. As housing prices increased rapidly, many Americans took on second mortgages in order to take advantage of their properties’ rising value. However, when housing prices crashed between 2007 and 2012, many individuals lost their homes because their properties values fell far below the amount that they owed and they were unable to repay their lenders.

It is also important to note that cash out refinancing is not available to HDB lease holders. Borrowers should also beware of prepayment penalties that penalise homeowners for repaying their reverse mortgage earlier than the agreed upon termination date. These fees could negate the benefits of cash out refinancing.

Bottom Line

Cash out refinancing, also known as a reverse or second mortgage, can be a relatively inexpensive way for private homeowners to take on debt to fund home renovations or to pay for college, which tend to have very predictable result in form of higher property value or higher earning potential for the family. With that said, we strongly suggest that individuals use these loans carefully and not for discretionary spending or speculative online trading as the worst case scenario could leave them without a home.

The article Is Cash Out Refinancing a Smart Financial Move? originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

- Best Home Loans 2018

- Best Personal Loans

- Home Loan Calculator: Find the Best Home Loan with Our Mortgage Experts

Source: VP