Consumer debt has been on the rise in Singapore. In face of rising unemployment, Singaporeans have been resorting to borrowing more money in order to keep funding their purchases of homes and cars and even for starting their businesses. As of 2016, households in Singapore were sitting on S$309bn of debt, which increased by 18% from S$260bn in 2012. However, this practice of borrowing is about to start becoming much less appealing. In fact, as the US Fed continues raising its interest rates, it’s more important now than ever for Singaporeans to start repaying their loans. Below, ValuePenguin analayses this issue one by one.

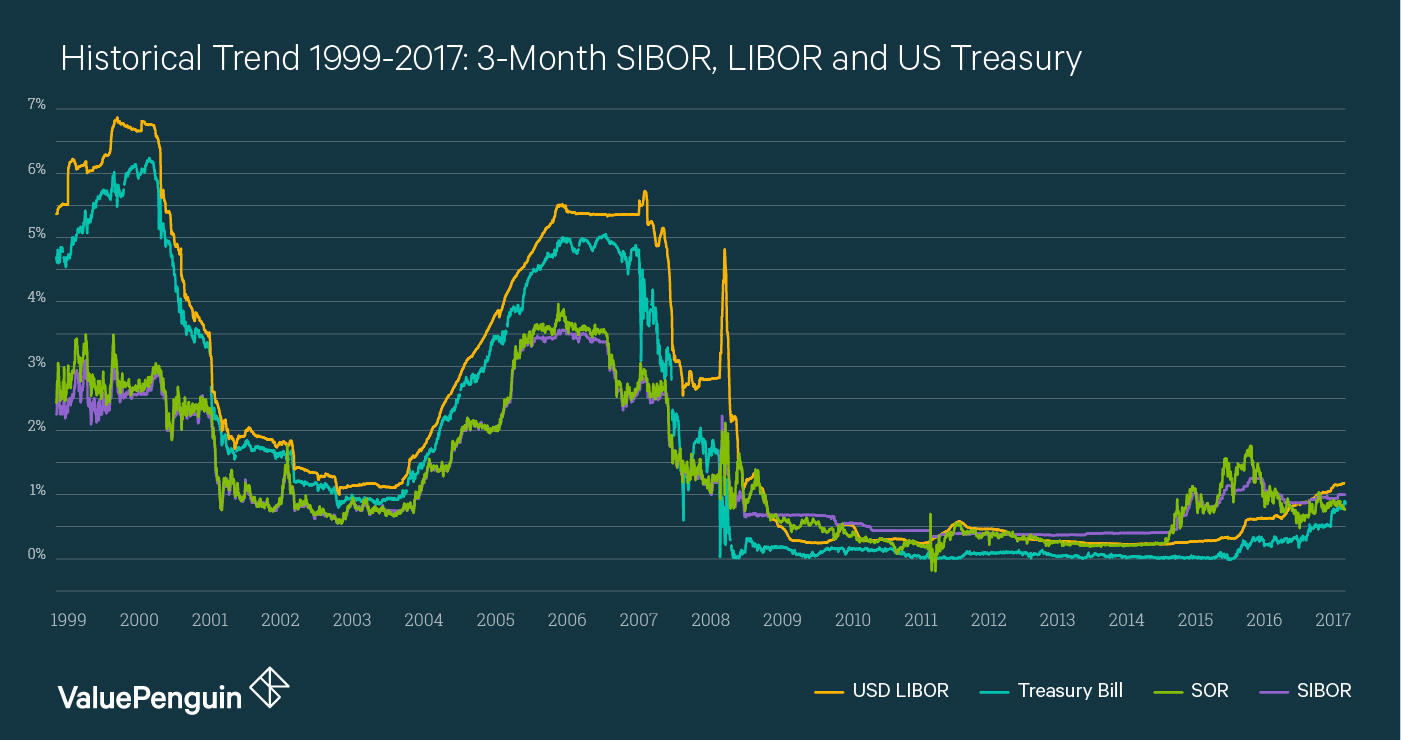

When US Rates Rise, Rates In Singapore Also Rise

First thing to recognise is that interest rates in Singapore and the US are very correlated. For instance, between 1999 and 2017, SIBOR and US treasury rates have had a correlation of 92.9%. This is why 3-month SIBOR has already risen to 1% from 0.87% in 2016, while the US Federal Reserve continued to hike its interest. This correlation exists because Monetary Authority of Singapore controls SIBOR primarily to regulate Singapore Dollar’s value. An increase in the US rates usually leads to an increase US dollar’s value, causing other central banks (including the MAS) to eventually increase its own rates to keep SGD’s exchange rates steady over the long run. As the Fed continues to work through its rate hike for the next few years, SIBOR is likely to rise upwards as well.

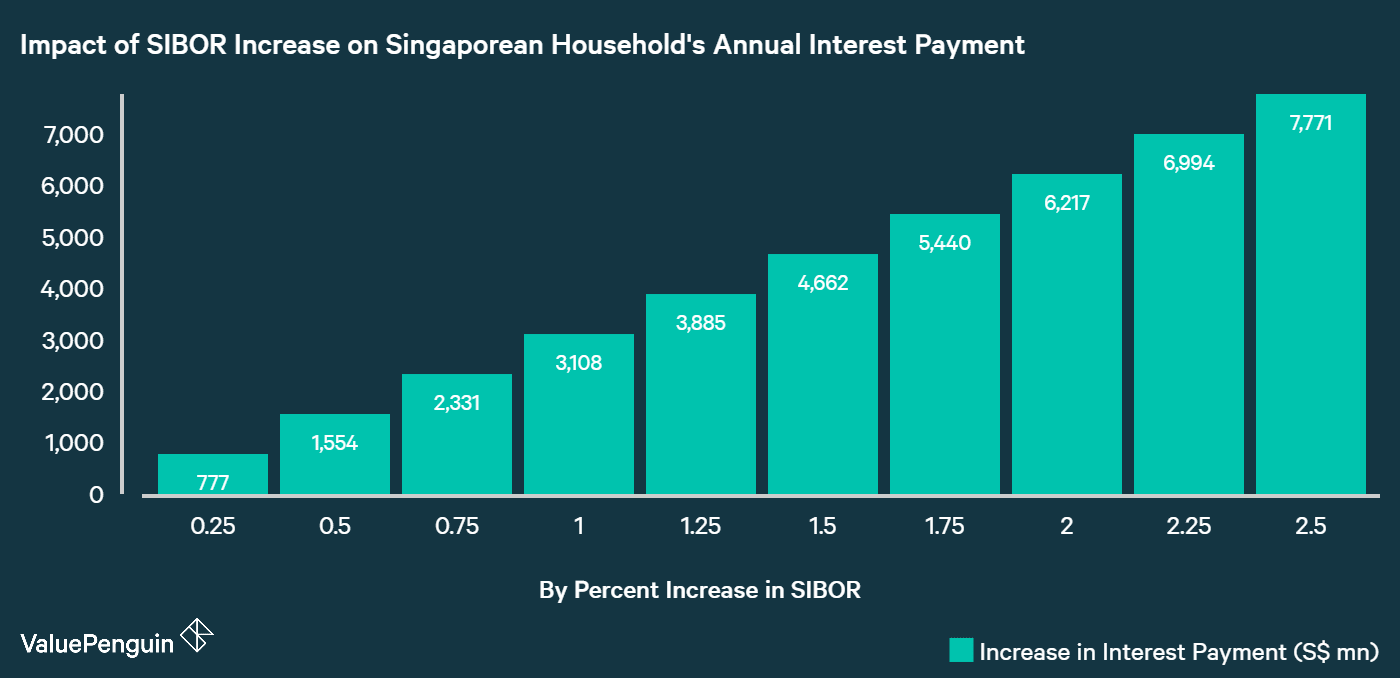

Each 0.25% Increase In SIBOR Can Cost Singaporeans S$777 Million Per Year

What this means is that Singaporeans are about to start paying a lot more on their loans than they have been for the past few years, as US interest rate drags up SIBOR. Currently, Singapore households possess S$310bn of debt, of which S$235bn was mortgage loans, S$10bn in car loans, S$10bn in credit card debt and another S$56bn in personal loans (i.e. study loan, personal loan, etc.). This roughly translates to S$12bn in annual interest payment alone.

| Outstanding Amount (S$ mn) | Estimated Interest Rate | Estimated Annual Interest (S$ mn) | |

|---|---|---|---|

| Home Loans | 234,710 | 1.5% | 3,521 |

| Car Loans | 9,773 | 3% | 293 |

| Credit Card Debt | 10,265 | 25% | 2,566 |

| Personal Loans | 56,083 | 10% | 5,608 |

| Total | 310,831 | 3.9% | 11,988 |

What’s interesting is that every 0.25% increase in US rates and thus in SIBOR could lead to extra interest payment of at least S$777 million per year (S$310bn x 0.25%) by the Singaporean households. That’s equivalent to a reduction of S$615 reduction in annual spending for every single household in the country (S$777mn / 1.26mn households). If 3-month SIBOR were to rise again back to its pre-2009 level of around 3.5%, that translates to a whopping S$8 billion of extra annual interest expenditures for Singaporeans (or S$6,000 per household), a whopping 65% increase from their current interest obligations.

Why It’s More Important Now Than Ever to Start Paying Off Your Loans

What does this mean for an average household? If your family has S$600,000 in total debt (i.e. S$500,000 in housing loan, S$50,000 in car loans, S$45,000 in personal loans and S$5,000 in credit card debt), every 0.25% increase in your interest rates will lead to S$1,500 less money that you can spend in a year, assuming nothing else changes. If rates rise up by 2% over the next 3-4 years, your interest payment alone can increase by S$12,000. Spending S$1,000 less every month can have real impact on the quality of your family’s life.

When rates were at historic lows, borrowing to consume was cheap and affordable. However, as the US Fed seems committed to its rate hike program for the next few years, it’s crucial for you to start planning ahead and begin reducing your debt obligations. For instance, it would be wise to start reducing your spending so that you direct more funding towards loan repayment. You can also refinance your mortgage or car loan at a lower rate now so that you have some extra funding to pay off your principals more quickly. If you have a lot of personal debt or credit card debt, you could utilise the newly available debt consolidation plans to help pay down your high-interest debt steadily.

The article Why It’s More Important Now Than Ever to Start Paying Off Your Loans originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

Source: ValuePen