For homeowners looking to improve their homes’ living conditions or to boost their values, renovation can seem like a daunting task. To help you understand and orchestrate this process smoothly, we’ve compiled a list of considerations important to a successful home remodeling project.

Get the basics first

Not all expensive projects add much value to your home. In fact, you should prioritize renovating some of the most basic but not-so-conspicuous features like windows, doors, electrical wiring, and plumbing. These types of projects typically cost under S$10,000 all combined, whereas a luxury kitchen renovation, for example, can cost S$30,000 alone. You can live with a S$20,000-kitchen instead of a S$30,000 one, but you should never have a leaking ceiling, a non-functional faucet, or a room without electricity. No potential buyer, not even you, would want to live in such a home. Therefore, it is much more financially prudent to allocate your budgets to these foundational features first, before spending the rest on giving a “wow” touch to your property.

Some renovation works pay off better

In terms of the money you get back per every dollar you spend (return on investment or ROI), not all renovation projects are equal. For example, minor kitchen renovations typically yield some of the highest ROIs of around 110%. That is, if you spend S$100 to upgrade your kitchen facilities, all else equal, you can sell the house for S$110 more. These “high-payoff” projects, including bathroom and kitchen upgrades, can be important for homeowners looking to maximise their home’s sale value. Not only that, they increase the “curb appeal” of your property, which means these areas tend to leave stronger impression on potential buyers and compel them to reach a buying decision.

Don’t simply follow the trend

You should not renovate your home in certain ways just because it is the “trend,” especially if you intend to reside in your home long-term. True, landlords can rent out their properties more quickly and save about 37% of cost by adopting the “industrial” style, a recent design trend in rental properties. But trends come and go quickly, whereas home renovation is a long-term project. Therefore, owner-residents can benefit from opting for classic design options with timeless materials like woods and marbles. While these materials can cost anywhere between 20% to 150% more than others depending on how they are installed, they help boost the value of a home over the longer-term.

Hiring an interior designer may pay off

If you are looking to do a large-scale overhaul of your home, you should consider hiring an interior designing company to manage the installation process. While they can cost anywhere between S$1,200 and S$5,000 depending on the size of your project, interior designers offer a unique value by outlining the look & feel of the renovation, as well as specifying where each fixture fits by the millimetre. Given that an average person only goes through one or two home renovations over her lifetime, getting an experienced expert’s tried and true advice can be priceless.

For one, interior designers can help you avoid spending more money to re-do a project because it turns out to be different from your expectations. They can also help you tailor your interior design with a potential sale in mind, so that your renovation can help increase both the quality of your life as well as your home’s sale value. Therefore, interior design consultations can be well worth your dollar if you are looking to alter the configuration of a large space and want to have maximum control over the end result before the engineering work commences.

Should you take up a renovation loan?

You should take up a home renovation loan if the benefit you enjoy from expanding the project outweighs the cost associated with borrowing the bank’s money. In general, you should expand your project’s budget by taking up a loan only if your home value can increase so much from the improvement to justify the additional interest costs you need to pay. These criteria can be complicated, however, by other factors like your emotional needs as well as your financial leverage.

| Benefit of Renovation Loan | Cost of Renovation Loan |

|---|---|

| Incremental appreciation in home value | Additional interest cost |

| Emotional desires to live in a better environment | Relative burden on monthly budget even if you ultimately break-even |

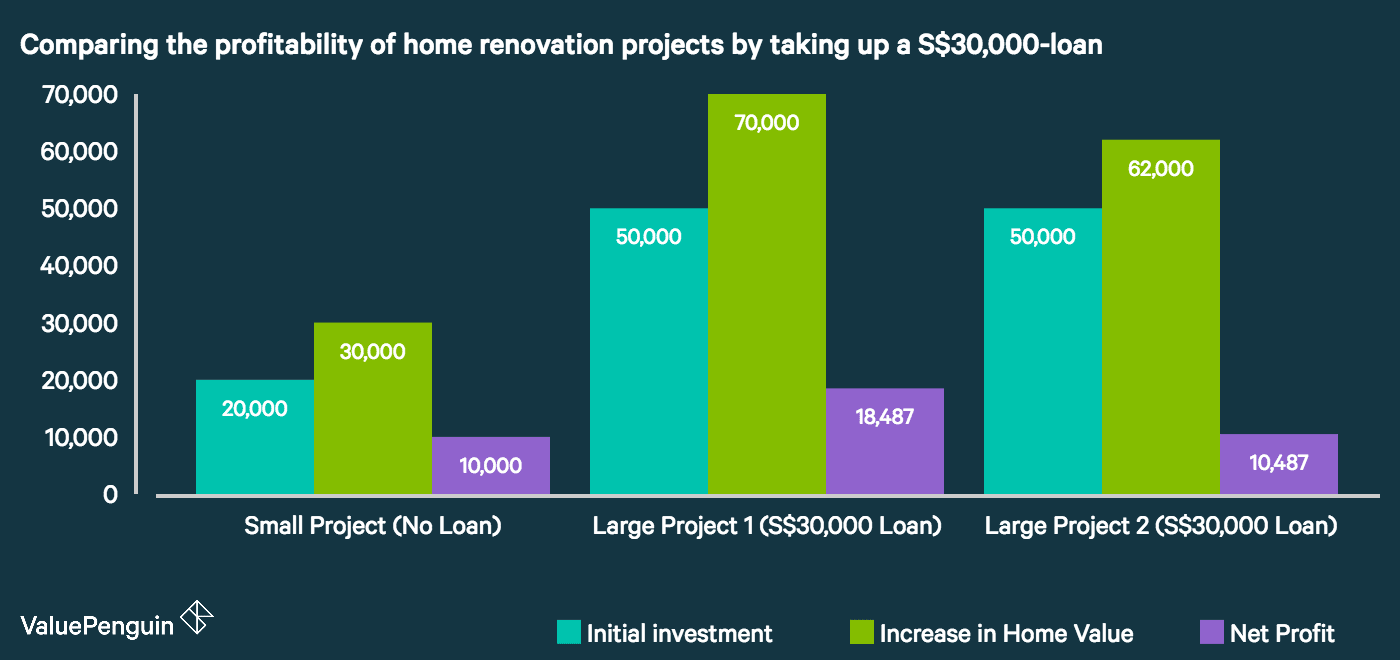

Let’s take a look at an example of how interest costs and project profitability can affect your decision to take out a home loan by assuming three different projects. Suppose there’s a renovation project you can do with S$20,000 of your own money, which can increase the value of your home by S$30,000. Such a project could generate a net benefit of S$10,000. Now, we could consider 2 bigger projects that cost S$50,000 in total. Since we only have S$20,000, it would require us to borrow S$30,000 of renovation loan from a bank like CIMB, which can cost S$1,513 in interest and fees over 3 years. Should we choose to do either of the bigger projects?

| (in SGD) | Small Project | Large Project 1 | Large Project 2 |

|---|---|---|---|

| Project Size | 20,000 | 50,000 | 50,000 |

| Your money + Loan | 20,000 + 0 | 20,000 + 30,000 | 20,000 + 30,000 |

| Est. increase in home val | 30,000 | 70,000 | 62,000 |

| Less: Initial investment | 20,000 | 50,000 | 50,000 |

| Incremental appreciation | 10,000 | 20,000 | 12,000 |

| Less: Interest cost | 0 | 1,513 | 1,513 |

| Net position | 10,000 | 18,487 | 10,487 |

| Note | – | Most preferred | Least preferred |

The answer to this question primarily depends on how much net benefit we gain by borrowing money to do a bigger renovation project. For example, project 1 increases the value of our home by S$70,000, which nets S$18,500 of benefit. Since this is a meaningful increase from S$10,000 of net benefit from the original small project, project 1 would be well worth the additional burden of getting a loan. In contrast, project 2 is nearly identical to the original one in terms of the net benefit we get. Since it generates no additional value compared to the original project, and can only decrease our monthly spending power, project 2 may not be worth pursuing.

Update Your Home Insurance Coverage

Following extensive upgrading and additions, you should make sure that the coverage on your home insurance policy matches the actual value of your property to avoid the penalty of under-insurance. If you do not already have a home insurance coverage, you should consider buying one to insure your new renovations. It’s a rather small sum of a few hundred dollars that can protect your large investment in your property from unforeseen mishaps and accidents.

Parting Thoughts

In addition to the financial concerns we noted above, home renovation can also have emotional values, namely the benefit of living in a better environment. Ultimately, it all comes down to costs and benefits, both financial and non-financial. We hope you’ll be able to use our resources to make the best financial decision for your individual needs.

The article 5 Things You Didn’t Know Before Embarking on a Home Renovation Project originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

Source: ValuePen